Advertisement

LIXIL Corporation (TSE:5938) has announced that it will pay a dividend of ¥45.00 per share on the 2nd of December. Based on this payment, the dividend yield on the company's stock will be 5.1%, which is an attractive boost to shareholder returns.

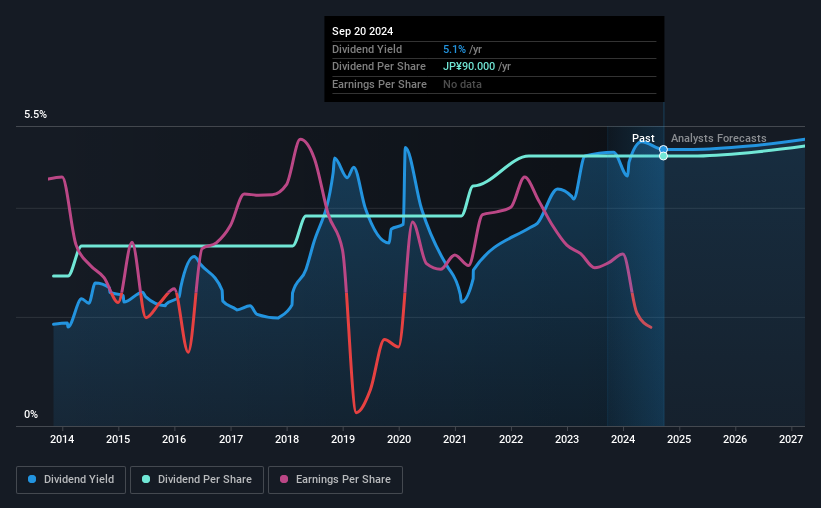

Check out our latest analysis for LIXIL

LIXIL's Distributions May Be Difficult To Sustain

A big dividend yield for a few years doesn't mean much if it can't be sustained. While LIXIL is not profitable, it is paying out less than 75% of its free cash flow, which means that there is plenty left over for reinvestment into the business. In general, cash flows are more important than the more traditional measures of profit so we feel pretty comfortable with the dividend at this level.

Looking forward, earnings per share is forecast to expand by 55.4% over the next year. While it is good to see income moving in the right direction, it still looks like the company won't achieve profitability. The healthy cash flows are definitely a good sign though, so we wouldn't panic just yet, especially with the earnings growing.

LIXIL Has A Solid Track Record

The company has an extended history of paying stable dividends. The annual payment during the last 10 years was ¥50.00 in 2014, and the most recent fiscal year payment was ¥90.00. This works out to be a compound annual growth rate (CAGR) of approximately 6.1% a year over that time. Companies like this can be very valuable over the long term, if the decent rate of growth can be maintained.

The Company Could Face Some Challenges Growing The Dividend

The company's investors will be pleased to have been receiving dividend income for some time. We are encouraged to see that LIXIL has grown earnings per share at 15% per year over the past five years. It's not great that the company is not turning a profit, but the decent growth in recent years is certainly a positive sign. All is not lost, but the future of the dividend definitely rests upon the company's ability to become profitable soon.

In Summary

Overall, we don't think this company makes a great dividend stock, even though the dividend wasn't cut this year. The company has been bring in plenty of cash to cover the dividend, but we don't necessarily think that makes it a great dividend stock. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For example, we've identified 2 warning signs for LIXIL (1 is concerning!) that you should be aware of before investing. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:5938

LIXIL

Through its subsidiaries, operates water technology and housing technology business in Japan and internationally.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor