Advertisement

Unearthing Undiscovered Gems With Promising Potential February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a landscape marked by tariff uncertainties and mixed economic signals, small-cap stocks have been particularly sensitive to these fluctuations, with indices like the S&P 600 reflecting broader market sentiment. Despite these challenges, opportunities arise for discerning investors who can identify companies with strong fundamentals and growth potential that may not yet be widely recognized.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Anpec Electronics | 3.15% | 3.67% | 9.94% | ★★★★★★ |

| Darya-Varia Laboratoria | NA | 1.44% | -11.65% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Prima Andalan Mandiri | 0.94% | 20.24% | 15.28% | ★★★★★★ |

| Yulie Sekuritas Indonesia | NA | 18.62% | 9.58% | ★★★★★★ |

| Central Finance | 1.21% | 11.98% | 16.10% | ★★★★★☆ |

| Vinacomin - Power Holding | 42.01% | -0.84% | 34.75% | ★★★★★☆ |

| Li Ming Development Construction | 236.64% | 31.54% | 34.00% | ★★★★☆☆ |

| Bhakti Multi Artha | 45.21% | 32.37% | -16.43% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

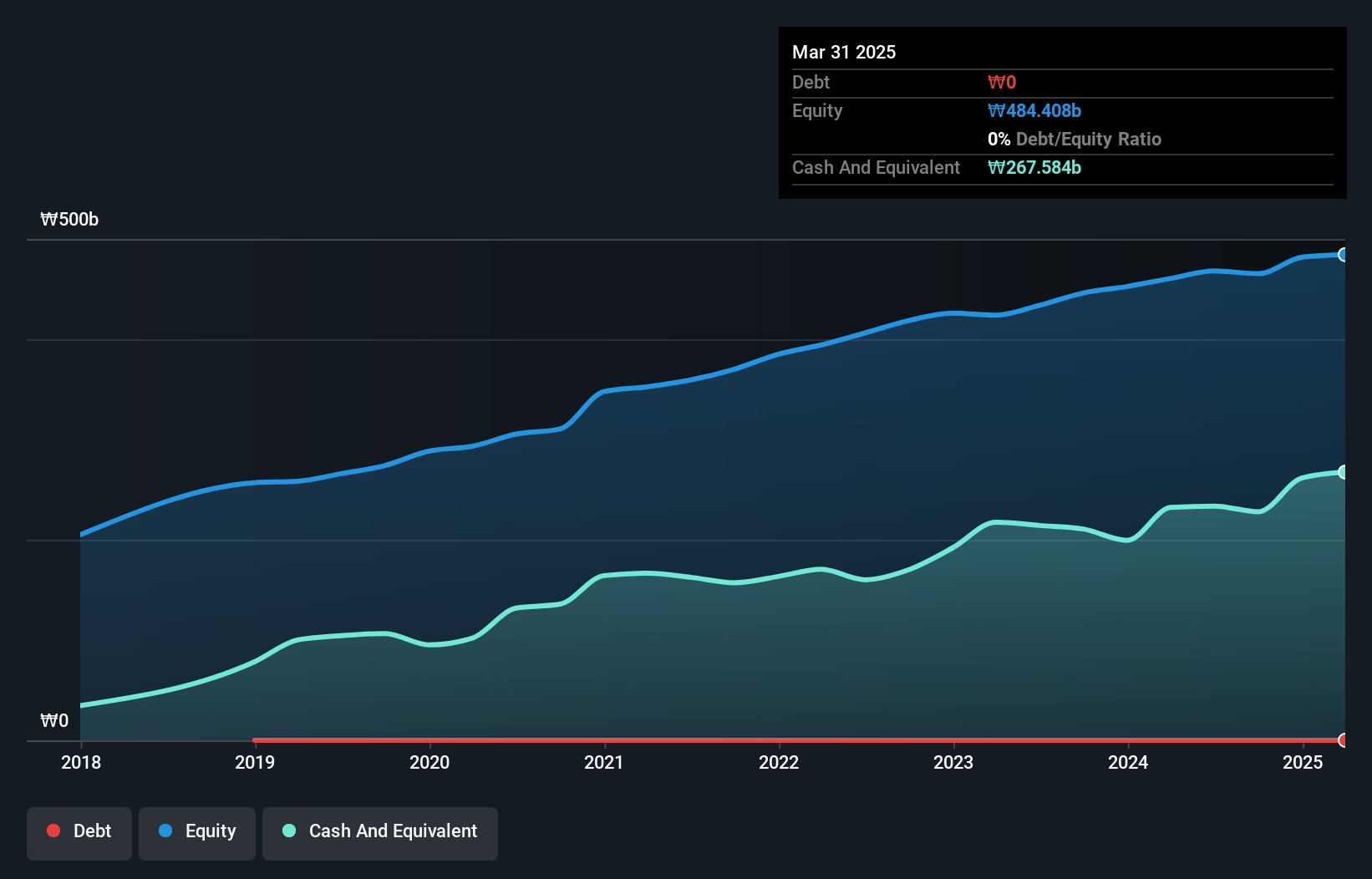

KCTech (KOSE:A281820)

Simply Wall St Value Rating: ★★★★★★

Overview: KCTech Co., Ltd. operates in South Korea, focusing on the manufacture and distribution of semiconductor systems, display systems, and electronic materials, with a market capitalization of approximately ₩680.09 billion.

Operations: KCTech generates revenue primarily from its semiconductor systems, display systems, and electronic materials segments. The company has a market capitalization of approximately ₩680.09 billion.

KCTech, a nimble player in the semiconductor space, showcases a debt-free status over the past five years and boasts high-quality earnings. The company has seen modest earnings growth of 0.4% last year, trailing behind the industry's 7.4%. However, its forecasted annual growth rate of nearly 31% suggests potential upside. Financially sound with positive free cash flow and recent capital expenditures around KRW 9 billion (US$8 million), KCTech also completed a share buyback program repurchasing about 1.28% of its shares for KRW 10 billion (US$8 million) last year, indicating confidence in its valuation and future prospects.

- Dive into the specifics of KCTech here with our thorough health report.

Assess KCTech's past performance with our detailed historical performance reports.

Lanzhou Lishang Guochao Industrial GroupLtd (SHSE:600738)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Lanzhou Lishang Guochao Industrial Group Co., Ltd operates department stores in China and internationally, with a market cap of CN¥3.62 billion.

Operations: The company generates its revenue primarily through the operation of department stores. Its financial performance is influenced by factors such as sales volume and cost management, with a focus on optimizing profit margins.

Lanzhou Lishang Guochao Industrial Group Ltd. showcases a dynamic profile with its earnings growth of 166% in the past year, outpacing the Multiline Retail industry's -5%. The company's net debt to equity ratio stands at a satisfactory 22.9%, reflecting prudent financial management as it decreased from 52.3% over five years. Its price-to-earnings ratio of 32x positions it attractively below the CN market average of 36x, suggesting potential value for investors. Despite a history of volatile share prices, its high-quality earnings and well-covered interest payments (10.9x EBIT) highlight robust operational performance amidst industry challenges.

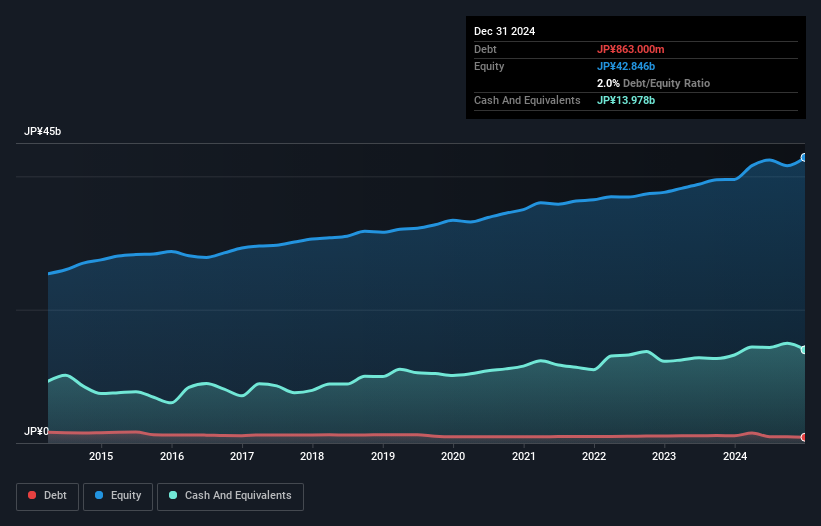

Nippon Hume (TSE:5262)

Simply Wall St Value Rating: ★★★★★★

Overview: Nippon Hume Corporation is engaged in the manufacturing and sale of pipes and concrete piles in Japan, with a market cap of ¥41.94 billion.

Operations: Nippon Hume generates revenue primarily from the manufacturing and sale of pipes and concrete piles. The company's financial performance is influenced by its gross profit margin, which has shown variability over recent periods.

Nippon Hume, a small player in the building industry, has been making waves with its remarkable earnings growth of 130% over the past year, outpacing the industry's 16%. The company is trading at 37% below its estimated fair value, presenting an intriguing opportunity. Its debt-to-equity ratio has improved from 2.8% to 2%, reflecting better financial health. Nippon Hume earns more interest than it pays and boasts high-quality earnings. With more cash than total debt and positive free cash flow, this firm seems well-positioned for future endeavors in a competitive market landscape.

- Click here to discover the nuances of Nippon Hume with our detailed analytical health report.

Evaluate Nippon Hume's historical performance by accessing our past performance report.

Seize The Opportunity

- Delve into our full catalog of 4695 Undiscovered Gems With Strong Fundamentals here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nippon Hume might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:5262

Flawless balance sheet with proven track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Apple: A Dying Star with an Overpriced Valuation

Fair Value US$177.34|19.1% overvalued

IN

Community Contributor

Avino a case for USD$20 per share within 5 years (assuming $3,500 gold, $100 silver and $4 copper).

Fair Value CA$26.79|86.0% undervalued

AG

Community Contributor

Riding the Defense Boom RENK Sees Revenue Climb at 15% CAGR by FY 2029

Fair Value €69.87|14.3% undervalued

CH

Community Contributor