Advertisement

- Japan

- /

- Construction

- /

- TSE:1979

Taikisha (TSE:1979): Assessing Valuation Following Completion of Share Buyback Program

Simply Wall St

Reviewed by Kshitija Bhandaru

Taikisha (TSE:1979) has concluded its share buyback program, purchasing 1.91% of its shares between July and September and reaching a total of 2.75% since May. This move reflects a focus on shareholder value.

See our latest analysis for Taikisha.

The completion of Taikisha’s buyback program comes at a time when the company’s momentum is building. Its share price has gained 17.1% year-to-date, and the one-year total shareholder return stands at an impressive 20.8%. Such steady gains, alongside a robust pace over the past three and five years, suggest continued optimism around long-term prospects and the impact of shareholder-friendly initiatives.

If Taikisha’s recent moves have sparked your curiosity about other companies with positive momentum, it might be a great moment to discover fast growing stocks with high insider ownership

With these strong results and shareholder-friendly actions, the key question for investors is whether Taikisha’s shares remain undervalued or if the recent gains already reflect all the good news. Is this a buying opportunity, or is future growth already priced in?

Price-to-Earnings of 16x: Is it justified?

At a price-to-earnings (P/E) ratio of 16x and a last close price of ¥2,881, Taikisha is trading above the construction industry average and above its own estimated fair P/E ratio.

The P/E ratio measures how much investors are willing to pay for each ¥1 of company earnings. In the context of Taikisha, this reflects market expectations for profits and growth. When compared to similar companies, Taikisha's P/E indicates investors may be pricing in stronger results than average, possibly due to its consistent profitability and recent shareholder initiatives.

However, the construction industry’s average P/E ratio is just 12.3x. This makes Taikisha look expensive by comparison. Furthermore, the estimated fair P/E ratio of 13.2x sets a level the broader market could benchmark against, suggesting the current multiple could be overreaching.

Explore the SWS fair ratio for Taikisha

Result: Price-to-Earnings of 16x (OVERVALUED)

However, slower revenue growth and Taikisha’s premium valuation could limit future returns if the market or industry conditions become less favorable.

Find out about the key risks to this Taikisha narrative.

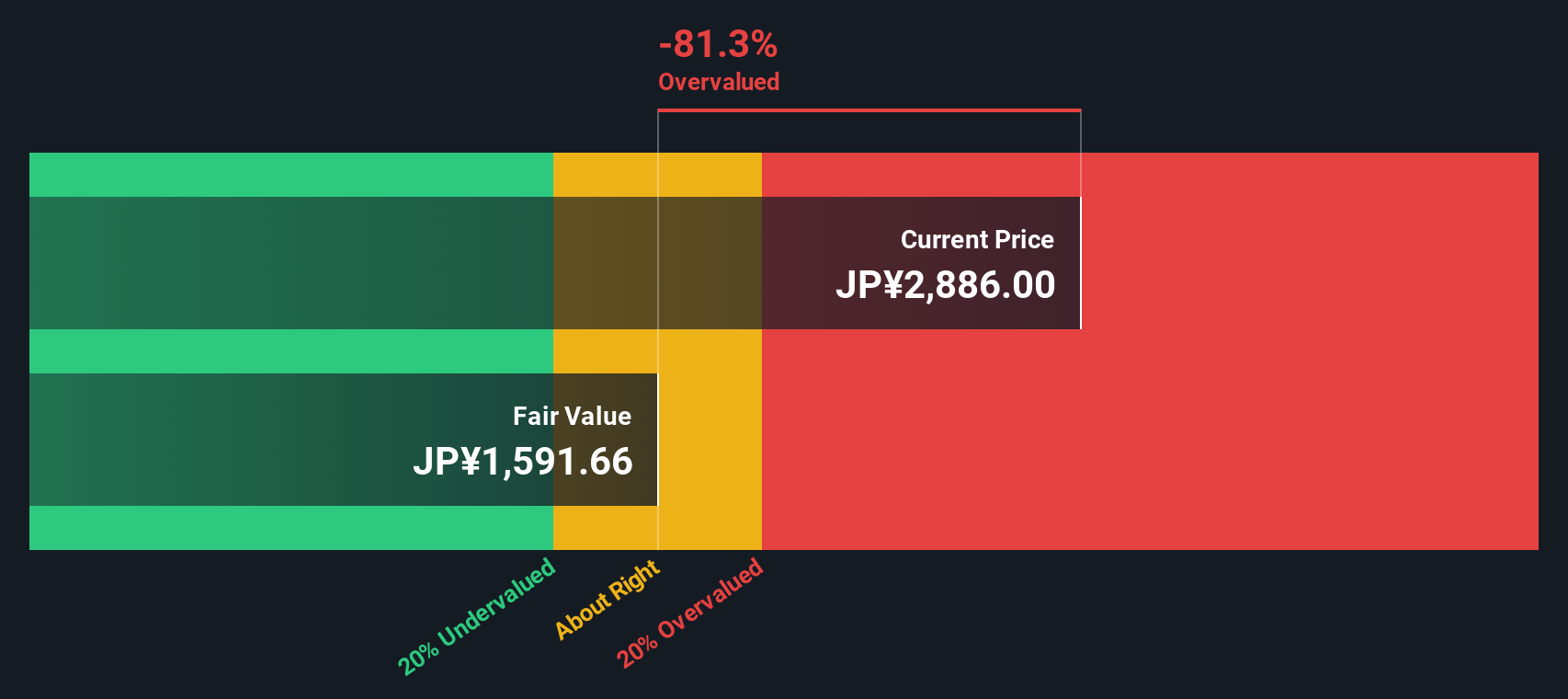

Another View: DCF Model Shows Even More Downside

While the price-to-earnings approach suggests Taikisha is expensively valued, the SWS DCF model presents an even starker picture. This analysis estimates that Taikisha's fair value is significantly below the current price, indicating the shares could be even more overvalued than multiples suggest. How does this shape your perspective on the risk?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Taikisha for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Taikisha Narrative

If you see things differently or want to look deeper into the numbers, you can build your own story from the data in just a few minutes with Do it your way.

A great starting point for your Taikisha research is our analysis highlighting 1 key reward and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Don't wait for the next hot stock to pass you by. Unlock opportunities by spotting trends and companies that could elevate your portfolio.

- Boost your income by tapping into steady cash flow. Start with these 19 dividend stocks with yields > 3% that offer reliable yields above 3%.

- Catch the wave of powerful tech disruption by uncovering leaders in artificial intelligence through these 25 AI penny stocks.

- Grow your wealth faster by targeting value-packed businesses with long-term upside using these 894 undervalued stocks based on cash flows based on strong cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Taikisha might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1979

Taikisha

Engages in the environmental systems and painting systems businesses in Japan.

Adequate balance sheet average dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor