- Japan

- /

- Construction

- /

- TSE:1965

Undiscovered Gems To Watch This February 2025

Reviewed by Simply Wall St

As February 2025 unfolds, global markets are navigating a complex landscape marked by fluctuating corporate earnings, AI competition fears, and steady monetary policies from major central banks. Amidst these dynamics, small-cap stocks have shown resilience despite broader market volatility and tariff uncertainties. In this environment, identifying promising stocks often involves looking for companies with strong fundamentals and growth potential that can weather economic shifts and capitalize on emerging trends.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Morris State Bancshares | 10.20% | -0.28% | 6.97% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Parker Drilling | 46.05% | 0.86% | 52.25% | ★★★★★★ |

| Nofoth Food Products | NA | 14.41% | 31.88% | ★★★★★★ |

| Aesler Grup Internasional | NA | -17.61% | -40.21% | ★★★★★★ |

| Berger Paints Bangladesh | 3.72% | 10.32% | 7.30% | ★★★★★☆ |

| Keir International | 23.18% | 49.21% | -17.98% | ★★★★★☆ |

| BOSQAR d.d | 94.35% | 39.11% | 23.56% | ★★★★☆☆ |

| Britam Holdings | 8.55% | -2.40% | 35.94% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

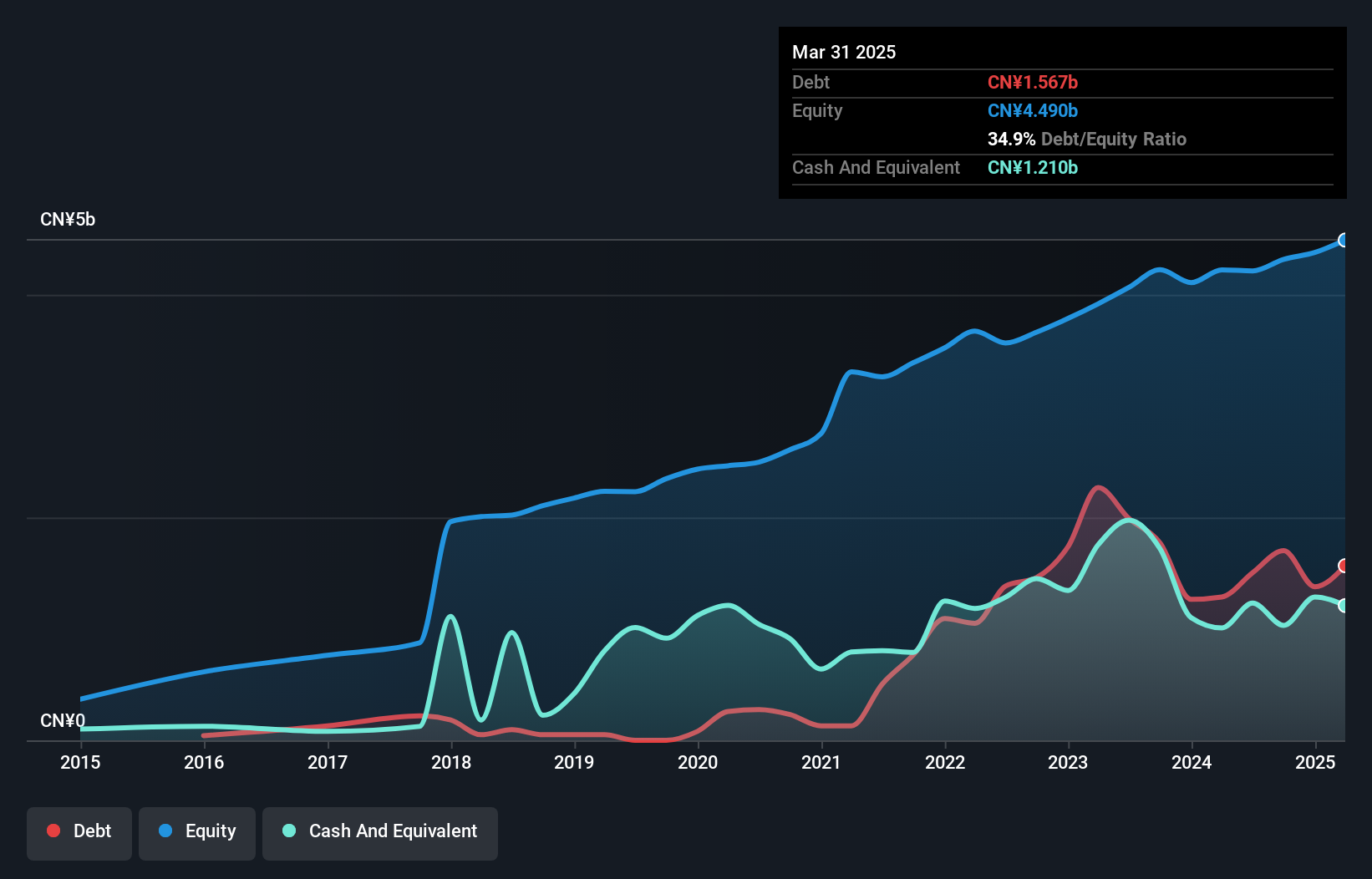

Aoshikang Technology (SZSE:002913)

Simply Wall St Value Rating: ★★★★★☆

Overview: Aoshikang Technology Co., Ltd. focuses on the research, development, production, and sale of printed circuit boards and has a market capitalization of CN¥7.74 billion.

Operations: Aoshikang derives its revenue primarily from the sale of printed circuit boards, amounting to CN¥4.41 billion.

Aoshikang Technology, a smaller player in the electronics sector, seems to offer value with its stock trading 57.4% below estimated fair value. Over the past year, earnings grew by 7.3%, outpacing the industry's 2.3% growth rate, indicating strong performance relative to peers. Despite an increase in debt-to-equity ratio from 0% to 39.4% over five years, interest payments are comfortably covered by EBIT at a multiple of 441x, reflecting robust financial health. The recent board changes and amendments to company bylaws could signal strategic shifts that may impact future growth prospects positively or negatively depending on execution.

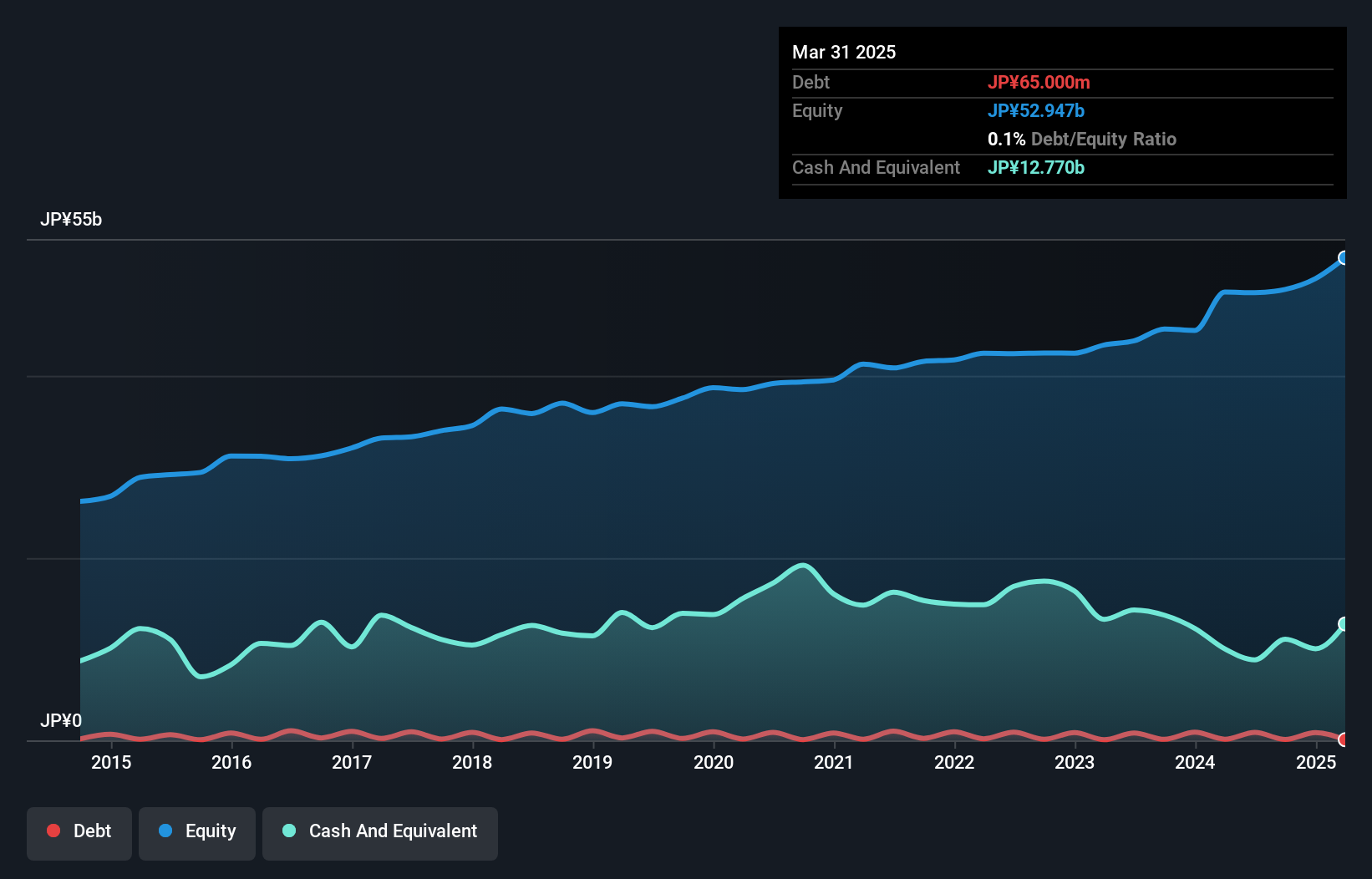

Techno Ryowa (TSE:1965)

Simply Wall St Value Rating: ★★★★★☆

Overview: Techno Ryowa Ltd. focuses on the design, construction, and maintenance of environmental control systems primarily in Japan with a market capitalization of ¥51.80 billion.

Operations: Techno Ryowa Ltd. generates revenue primarily from its Air Conditioning Sanitary Equipment Construction Business, which accounts for ¥48.01 billion, and General Building Equipment Work, contributing ¥25.11 billion. The Electrical Equipment Construction Business and Cooling and Heating Equipment Sales Segment add smaller portions of ¥2.62 billion and ¥1.20 billion respectively to the company's total revenue stream.

Techno Ryowa, a smaller player in its field, is showing promising signs with an impressive 77.5% earnings growth over the past year, outpacing the construction industry's 20.3%. Its debt to equity ratio has improved from 0.5 to 0.2 over five years, indicating better financial health. The company also boasts high-quality earnings and a favorable price-to-earnings ratio of 12.3x compared to the JP market's 13.4x, making it an attractive option for value seekers. However, free cash flow remains negative at -US$738 million as of September last year, which could be an area of concern moving forward.

- Click to explore a detailed breakdown of our findings in Techno Ryowa's health report.

Evaluate Techno Ryowa's historical performance by accessing our past performance report.

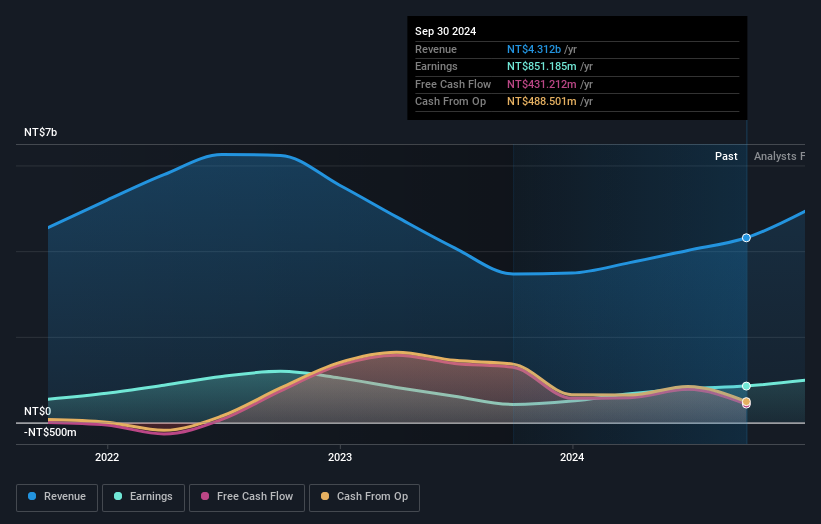

Flytech Technology (TWSE:6206)

Simply Wall St Value Rating: ★★★★★★

Overview: Flytech Technology Co., Ltd. designs, manufactures, trades in, and sells computers and peripheral equipment across various international markets, with a market cap of NT$13.69 billion.

Operations: Flytech Technology generates revenue primarily from the design, manufacturing, and sale of computers and peripheral equipment across multiple international markets. The company's financial performance is reflected in its market capitalization of NT$13.69 billion.

Flytech Technology, a nimble player in the tech space, has shown impressive financial strides recently. With earnings growth of 101% over the past year, it outpaces its industry peers significantly. The company boasts a debt-free status, which enhances its financial stability and flexibility. Its price-to-earnings ratio of 17.6x suggests it is attractively valued compared to the broader TW market at 20.4x. Recent earnings reports reveal strong performance with third-quarter sales hitting TWD 1,097 million and net income at TWD 190 million, reflecting solid operational efficiency and profitability improvements over last year’s figures.

- Navigate through the intricacies of Flytech Technology with our comprehensive health report here.

Understand Flytech Technology's track record by examining our Past report.

Key Takeaways

- Reveal the 4688 hidden gems among our Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Techno Ryowa might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1965

Techno Ryowa

Engages in the design, construction, and maintenance of environmental control systems primarily in Japan.

Solid track record with excellent balance sheet.

Market Insights

Community Narratives