Advertisement

- Japan

- /

- Construction

- /

- TSE:1860

Toda Corporation (TSE:1860): Evaluating Valuation as NFT Tourism Partnership Signals Tech Innovation

Simply Wall St

Reviewed by Kshitija Bhandaru

Toda (TSE:1860) recently partnered with JTB and Fujitsu in a pilot program aimed at using NFTs to support tourism and regional digital transformation in Fukui Prefecture. This move is in line with Japan’s national focus on Web3-driven revitalization.

See our latest analysis for Toda.

Toda’s latest NFT partnership seems to have caught the market’s interest, with the share price climbing 8% over the last three months and boosting its one-year total shareholder return to a solid 12.5%. While recent momentum has been positive, the longer-term track record, with total returns of 55% over three years and nearly 78% over five, shows how well the stock has rewarded patient holders.

If Toda’s tech-forward moves have made you curious, now’s a great time to broaden your search and discover fast growing stocks with high insider ownership

With shares up and innovative projects underway, the key question for investors is whether Toda remains undervalued amidst this momentum, or if the recent gains indicate the market is already pricing in much of its future growth potential.

Price-to-Earnings of 12.4x: Is it justified?

Toda trades on a price-to-earnings (P/E) ratio of 12.4x, just above the Japanese Construction industry average of 12.3x. At the recent close of ¥1,034, the stock is not cheap relative to peers, suggesting the market is pricing in cautious optimism.

The price-to-earnings ratio reflects how much investors are willing to pay for each yen of current earnings. For construction companies like Toda, the P/E can signal expectations for profitability, growth, and sector stability. When the ratio stands just above the industry average, it indicates the stock may be carrying a mild premium, potentially linked to its recent digital initiatives and returns.

However, compared to its estimated fair price-to-earnings of 12.3x, Toda looks only slightly expensive. This level suggests room for sentiment to shift if results either beat or lag current expectations. The market’s implied “fair” valuation could act as a magnet for future moves.

Explore the SWS fair ratio for Toda

Result: Price-to-Earnings of 12.4x (ABOUT RIGHT)

However, flat annual net income growth and a valuation close to analyst targets could limit further upside if operational improvements do not materialize soon.

Find out about the key risks to this Toda narrative.

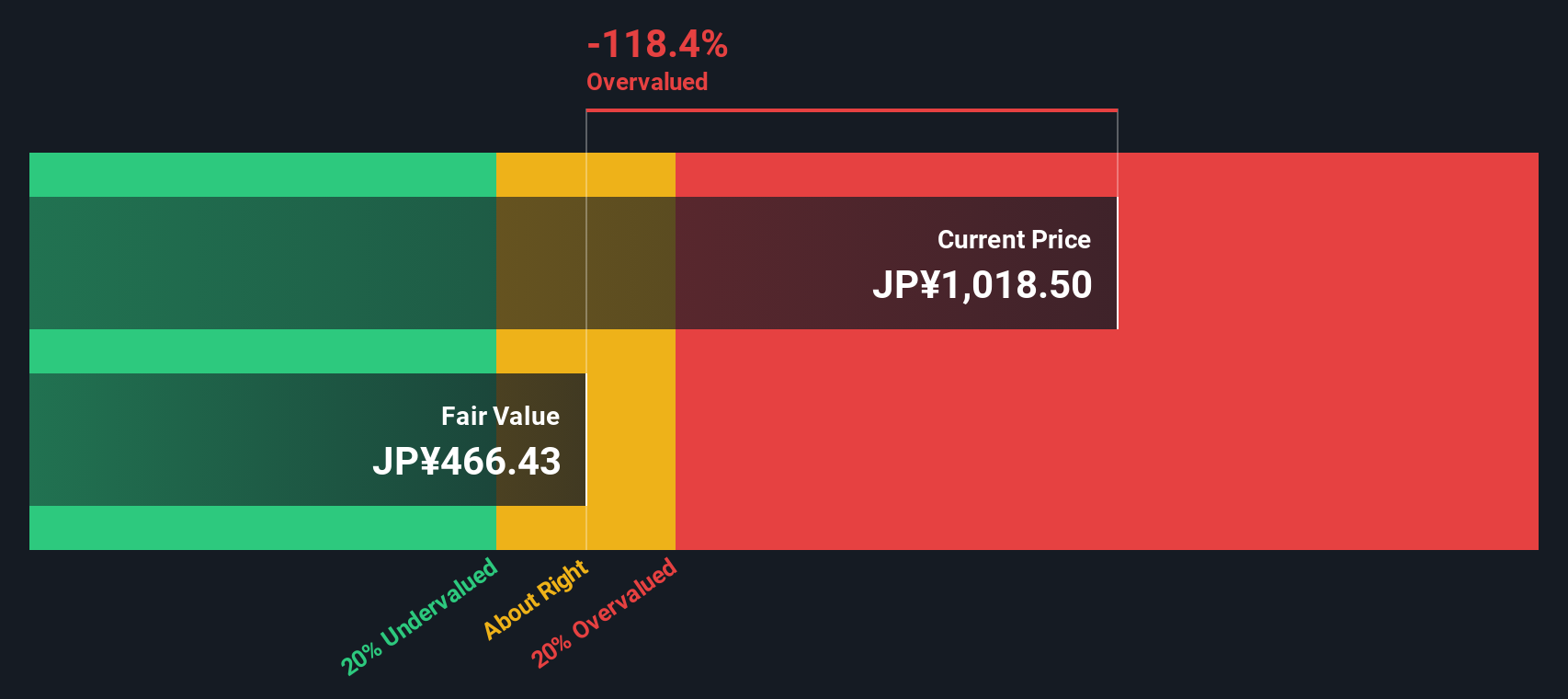

Another View: Discounted Cash Flow Model

Looking from a different perspective, our DCF model suggests Toda’s shares may be trading above their estimated fair value. The current price of ¥1,034 is significantly higher than the DCF-derived value of ¥468. This method uses future cash flow projections instead of earnings multiples, which challenges the optimism seen in market ratios.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Toda for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Toda Narrative

If you want a different perspective, why not take a hands-on approach and build your own view right from the numbers in just a few minutes. Do it your way

A great starting point for your Toda research is our analysis highlighting 2 key rewards and 3 important warning signs that could impact your investment decision.

Looking for More Smart Investment Opportunities?

There’s a world of potential waiting beyond Toda. Make your next portfolio move with confidence as these hand-picked stock ideas could put you ahead of the crowd.

- Capture growth by targeting these 25 AI penny stocks set to benefit from artificial intelligence breakthroughs across industries.

- Boost your passive income by choosing these 19 dividend stocks with yields > 3% offering robust yields and a track record of stable payouts.

- Ride the innovation wave by finding these 26 quantum computing stocks at the forefront of quantum computing advancements and disruption.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Toda might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:1860

Toda

Primarily engages in the construction and civil engineering businesses in Japan and internationally.

Proven track record average dividend payer.

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|13.6% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$89.00|23.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|37.6% undervalued

TR

Community Contributor