Should You Buy The Oita Bank, Ltd. (TSE:8392) For Its Upcoming Dividend?

Readers hoping to buy The Oita Bank, Ltd. (TSE:8392) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. The ex-dividend date generally occurs two days before the record date, which is the day on which shareholders need to be on the company's books in order to receive a dividend. The ex-dividend date is important because any transaction on a stock needs to have been settled before the record date in order to be eligible for a dividend. Thus, you can purchase Oita Bank's shares before the 28th of March in order to receive the dividend, which the company will pay on the 23rd of June.

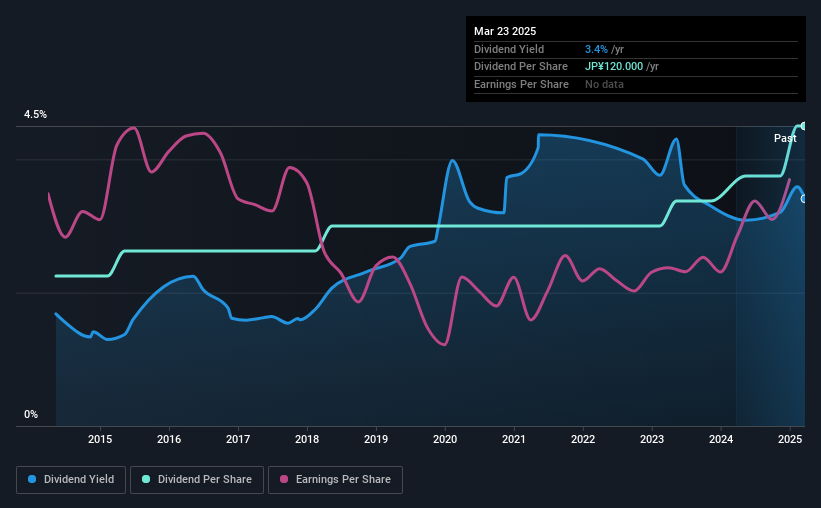

The company's next dividend payment will be JP¥60.00 per share, on the back of last year when the company paid a total of JP¥120 to shareholders. Based on the last year's worth of payments, Oita Bank has a trailing yield of 3.4% on the current stock price of JP¥3520.00. Dividends are an important source of income to many shareholders, but the health of the business is crucial to maintaining those dividends. So we need to check whether the dividend payments are covered, and if earnings are growing.

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Oita Bank paid out just 19% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances.

Generally speaking, the lower a company's payout ratios, the more resilient its dividend usually is.

Check out our latest analysis for Oita Bank

Click here to see how much of its profit Oita Bank paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies with consistently growing earnings per share generally make the best dividend stocks, as they usually find it easier to grow dividends per share. If earnings fall far enough, the company could be forced to cut its dividend. This is why it's a relief to see Oita Bank earnings per share are up 8.4% per annum over the last five years.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. Oita Bank has delivered 7.2% dividend growth per year on average over the past 10 years. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

Final Takeaway

Has Oita Bank got what it takes to maintain its dividend payments? Oita Bank has seen its earnings per share grow slowly in recent years, and the company reinvests more than half of its profits in the business, which generally bodes well for its future prospects. In summary, Oita Bank appears to have some promise as a dividend stock, and we'd suggest taking a closer look at it.

Want to learn more about Oita Bank's dividend performance? Check out this visualisation of its historical revenue and earnings growth.

A common investing mistake is buying the first interesting stock you see. Here you can find a full list of high-yield dividend stocks.

If you're looking to trade Oita Bank, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSE:8392

Oita Bank

Provides various banking products and services to individual and corporate clients primarily in Japan.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives