Aisin (TSE:7259) shares have recently drawn attention for their steady performance, especially as the stock delivered gains of 1% over the past day. Investors are now weighing up the company's valuation following this recent move.

While Aisin's 1% gain grabbed headlines this week, it's the bigger picture that counts. The company's 1-year total shareholder return stands at a modest 0.6%, reflecting a period of stable but subdued momentum despite pockets of optimism around earnings and sector developments. Investors are watching closely to see if growth appetite or risk perception will shift the narrative from here.

If you're keen to see what else is shifting in the auto space, there's a real opportunity to discover See the full list for free.

With shares moving sideways and modest growth in annual results, the crucial question is whether Aisin’s current valuation leaves room for upside or if future prospects are already reflected in the stock price.

Advertisement

Price-to-Earnings of 14.2x: Is it justified?

Aisin currently trades at a Price-to-Earnings (P/E) ratio of 14.2x, positioning it above the JP Auto Components industry average of 11.2x. With a last close of ¥2,551.5, this premium valuation raises questions about whether investors are paying up for future growth or strong fundamentals.

The P/E ratio is a widely used measure that compares a company’s share price to its per-share earnings. For automakers and parts suppliers like Aisin, it signals how much the market expects in terms of future earnings growth or quality. A higher multiple typically suggests confidence in the company's trajectory, but can also reflect market optimism that may not materialize.

Aisin’s P/E sits not only above the industry average but also right in line with its peer group average. Compared to its estimated fair P/E ratio of 15.7x, the current level could be seen as reasonable, though it suggests there is limited upside unless profits accelerate further.

However, slower revenue growth or a further discount to analyst price targets could put pressure on Aisin’s shares and challenge the current valuation narrative.

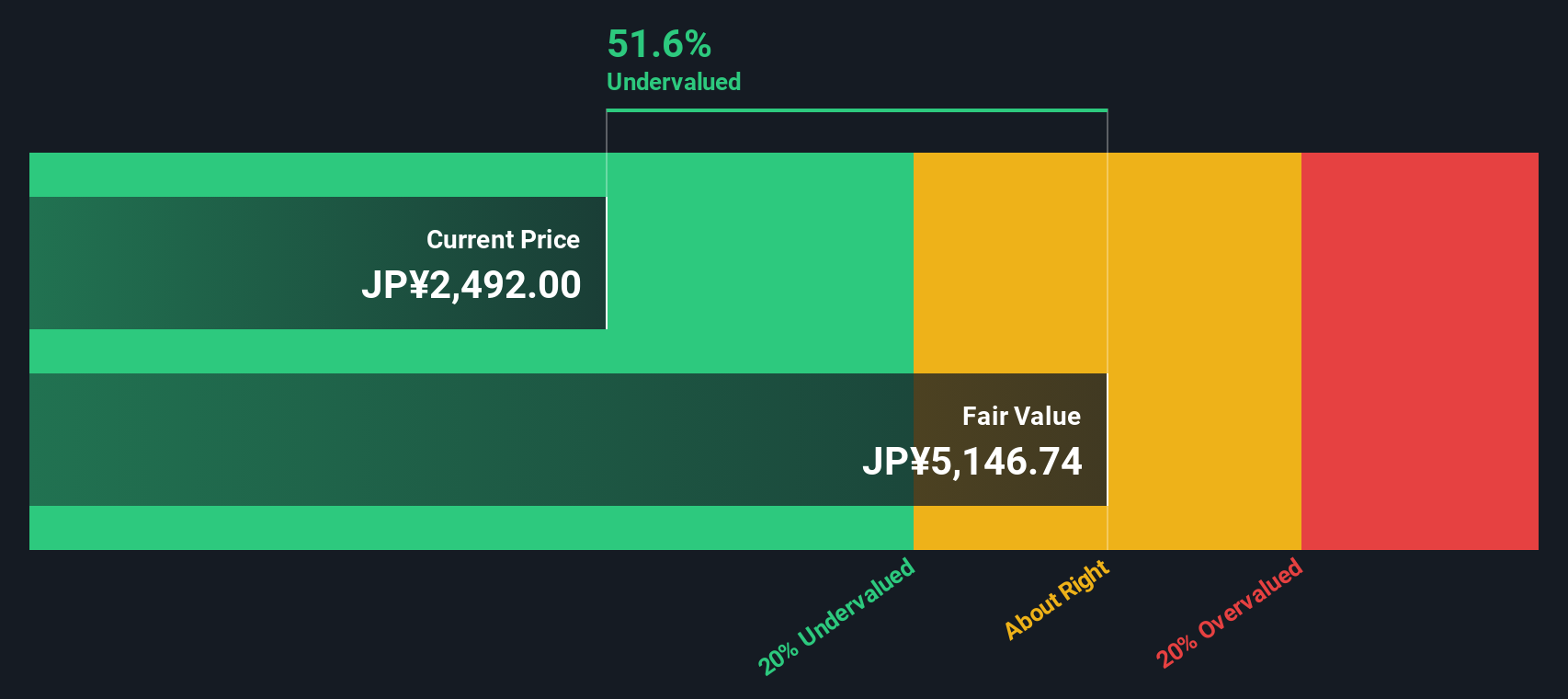

Looking at Aisin through a different lens, our DCF model suggests the shares are actually trading well below their intrinsic value. Based on this approach, Aisin is undervalued by nearly 50%, hinting at much greater upside than the P/E ratio alone may imply. So which narrative stands up: premium pricing or hidden value?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Aisin for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Aisin Narrative

If you see things differently or want to dig deeper into the data yourself, it only takes a couple of minutes to build your own perspective on Aisin, and Do it your way.

There's an entire world of opportunities waiting beyond Aisin. Use the Simply Wall Street Screener and get a real edge on the market’s next big themes.

Capture innovation in technology and healthcare by browsing these 31 healthcare AI stocks, which highlights companies reshaping patient care and diagnostics.

Uncover potential in the fast-growing digital assets space by scanning these 78 cryptocurrency and blockchain stocks, where blockchain businesses are building tomorrow’s finance giants.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks