Nissan Motor (TSE:7201) shares have seen shifts worth watching lately, especially as the stock wrapped up the past month with a 1% gain and an impressive 19% rise over the past 3 months. Investors are paying attention to how the stock holds up after a volatile stretch, with valuation and fundamentals serving as key guideposts.

Nissan Motor’s 1% rise over the past month comes after a bumpy start to the year, with momentum picking up recently despite a 21% year-to-date share price decline. Over the longer term, total shareholder return remains modest. This highlights both recovery potential and ongoing scrutiny of fundamentals.

If Nissan’s shifting momentum has you curious about other automakers, it’s a great opportunity to check out See the full list for free.

With recent momentum shifts and fundamentals under close watch, the key question is whether Nissan Motor is currently trading below its true value, or if the market has already factored in the company’s future prospects. Could this be a genuine buying window, or is everything priced in?

Advertisement

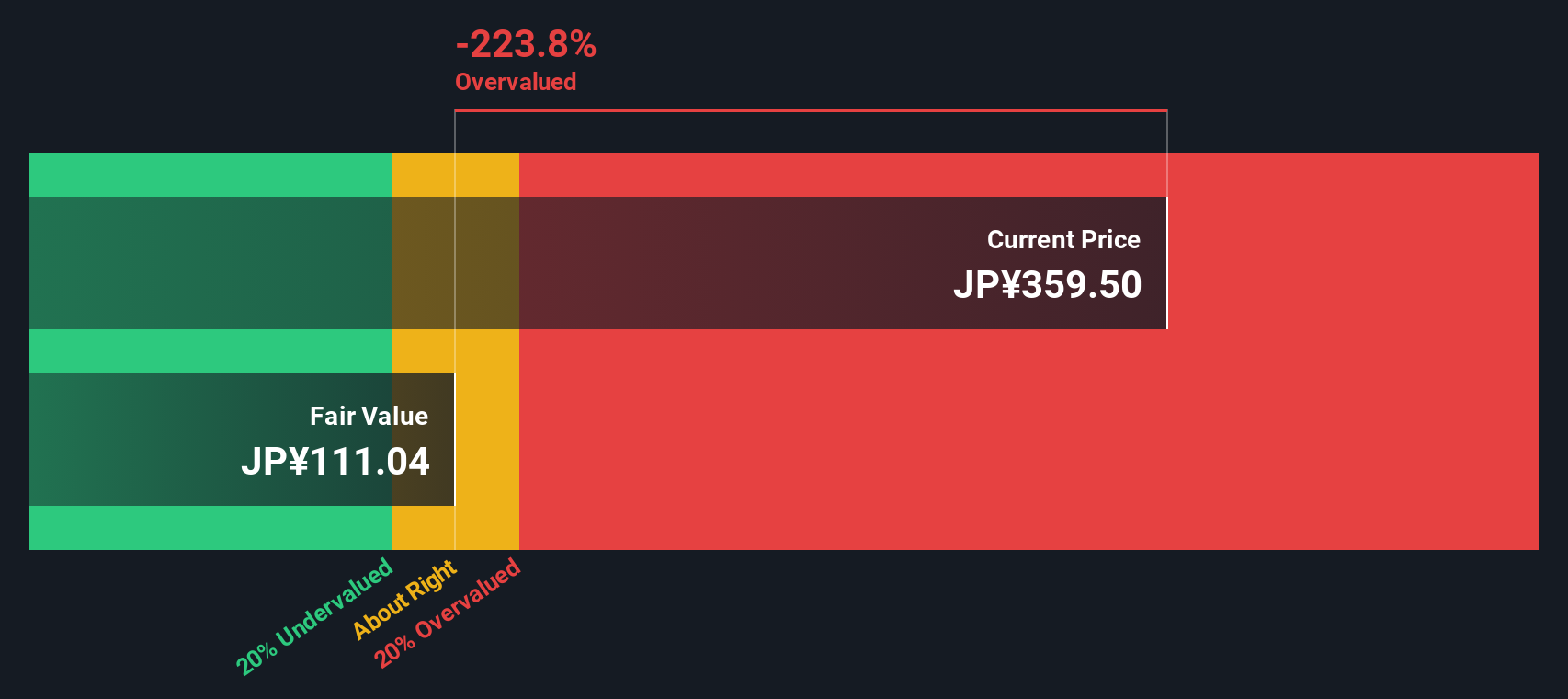

Most Popular Narrative: 12% Overvalued

The latest narrative puts Nissan Motor’s fair value below the current market price, highlighting a disconnect between analyst expectations and recent share performance. This context sets up debate about whether optimism is running too far ahead of fundamentals.

Aggressive cost reduction initiatives under the Re:Nissan plan, including plant consolidation, fixed and variable cost savings, engineering process improvements, and supply chain optimization, are designed to significantly improve operating earnings and net margins. Tangible benefits are expected from 2026 onward as restructuring milestones are completed. Deeper global partnerships and scaling via the Renault-Mitsubishi alliance, along with ongoing collaborations with other automakers such as Honda, are expected to yield further R&D and manufacturing efficiencies, shared platform utilization, and technology advancements. These changes support long-term margin expansion through enhanced economies of scale.

Curious how these bold turnaround strategies collide with razor-thin margin projections? The playbook behind this valuation combines risky profit growth with untested efficiency moves. Discover which forecasts and alliance bets underpin the narrative’s calculation—will expectations hit the mark or backfire?

However, mounting competition in China and continuing negative cash flow could quickly challenge the positive outlook for recovery and margin expansion for Nissan Motor.

While industry and peer comparisons suggest Nissan Motor is attractively valued on a sales basis, our DCF model tells a different story. According to this cash flow-based approach, Nissan’s stock price sits well above its estimated fair value. This may indicate possible overvaluation if longer-term growth does not materialize as forecast.

If you see the numbers differently or want to draw your own conclusions, you can build a unique narrative of your own in just a few minutes. Do it your way

A great starting point for your Nissan Motor research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Take control of your portfolio by seeking out tomorrow’s big opportunities. Don’t let the market move on without you. Use these tools to find smart investments now:

Capitalise on the transformative power of artificial intelligence by targeting growth potential in these 26 AI penny stocks, driving innovation across industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Nissan Motor might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.