Advertisement

3 European Stocks Estimated To Be Undervalued By Up To 37.1%

Simply Wall St

Reviewed by Simply Wall St

The European market has recently seen mixed performances, with the pan-European STOXX Europe 600 Index edging up by 0.56% amid hopes for increased government spending, although concerns over U.S. tariffs have tempered gains. As central banks navigate growth challenges and inflation risks, investors are on the lookout for stocks that may be undervalued in this uncertain environment. Identifying such stocks involves assessing their intrinsic value compared to current market prices, especially when broader economic conditions present both opportunities and challenges.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Absolent Air Care Group (OM:ABSO) | SEK261.00 | SEK510.37 | 48.9% |

| Biotage (OM:BIOT) | SEK98.45 | SEK191.35 | 48.5% |

| Romsdal Sparebank (OB:ROMSB) | NOK130.00 | NOK257.93 | 49.6% |

| TF Bank (OM:TFBANK) | SEK349.00 | SEK685.85 | 49.1% |

| Bonesupport Holding (OM:BONEX) | SEK300.60 | SEK584.32 | 48.6% |

| Vestas Wind Systems (CPSE:VWS) | DKK102.40 | DKK202.35 | 49.4% |

| F-Secure Oyj (HLSE:FSECURE) | €1.742 | €3.45 | 49.5% |

| Neosperience (BIT:NSP) | €0.538 | €1.06 | 49.2% |

| Fodelia Oyj (HLSE:FODELIA) | €7.14 | €13.91 | 48.7% |

| Dino Polska (WSE:DNP) | PLN457.20 | PLN887.95 | 48.5% |

Let's dive into some prime choices out of the screener.

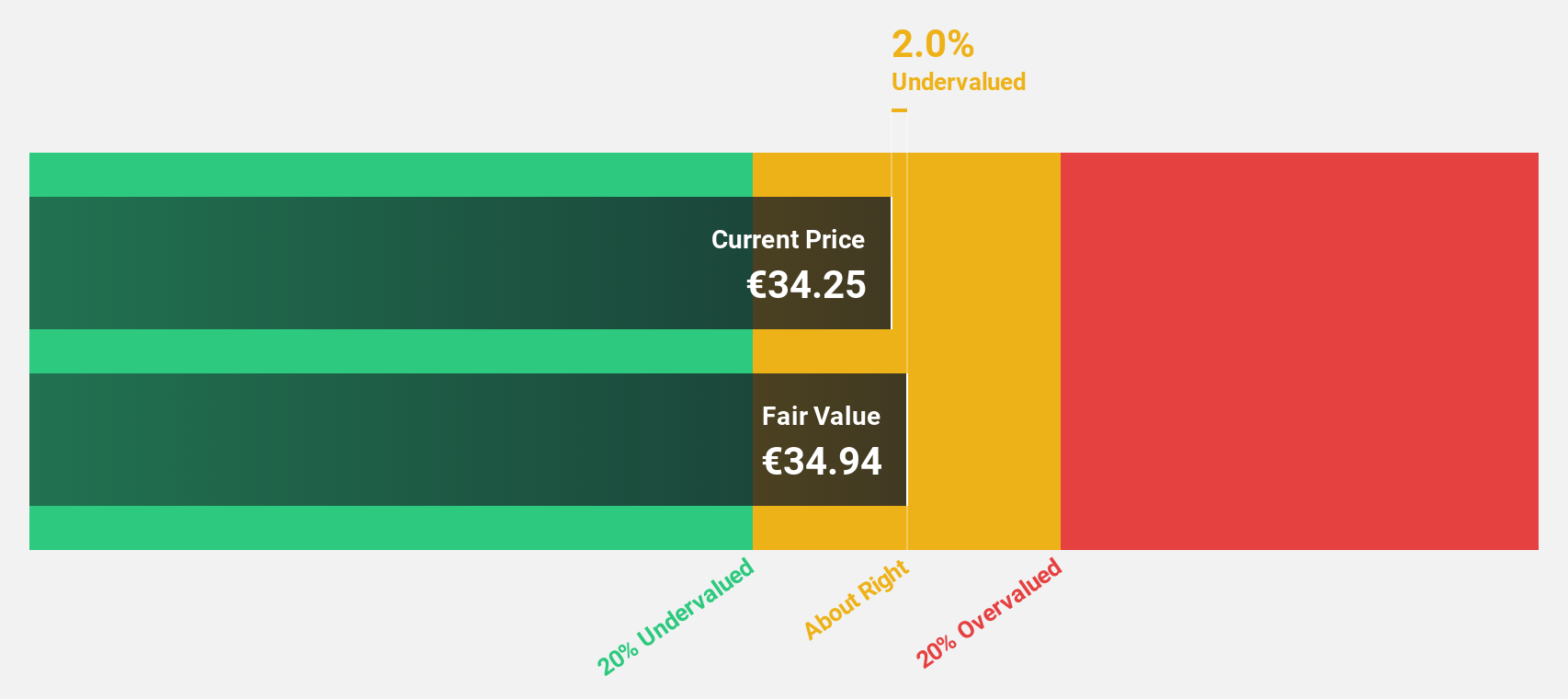

TXT e-solutions (BIT:TXT)

Overview: TXT e-solutions S.p.A. offers software and service solutions both in Italy and internationally, with a market cap of €420.57 million.

Operations: The company's revenue is derived from three main segments: Fintech (€191.70 million), Smart Solutions (€64 million), and Digital Advisory (€48.90 million).

Estimated Discount To Fair Value: 23.8%

TXT e-solutions appears undervalued based on cash flows, trading at €34.8, below its estimated fair value of €45.69. With earnings expected to grow significantly by 20.77% annually and revenue outpacing the Italian market at 12.6%, the company shows strong growth potential despite a lower forecasted return on equity of 17.6%. Recent strategic moves include pursuing M&A to enhance market reach and a partnership with Zen Technologies for advanced pilot training solutions, potentially boosting future cash flows.

- The analysis detailed in our TXT e-solutions growth report hints at robust future financial performance.

- Click here and access our complete balance sheet health report to understand the dynamics of TXT e-solutions.

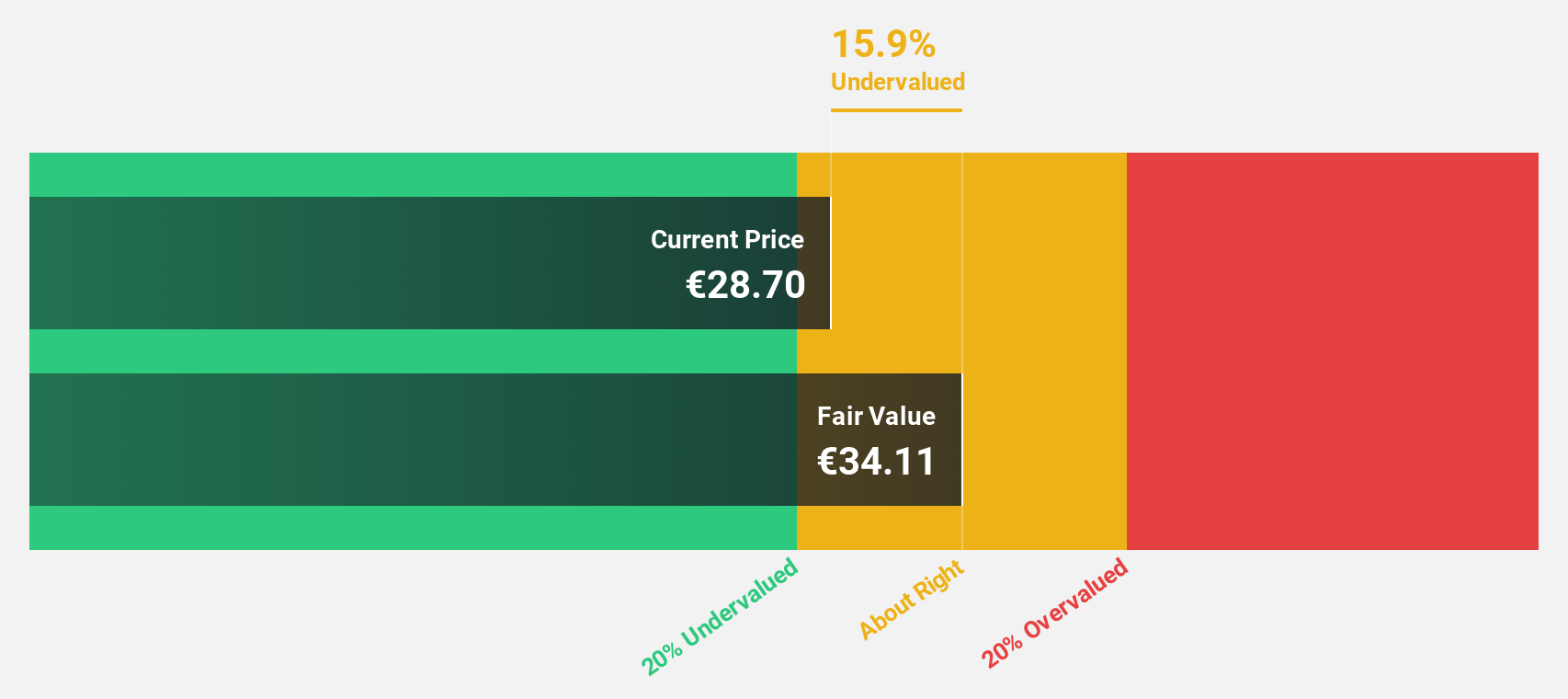

Revenio Group Oyj (HLSE:REG1V)

Overview: Revenio Group Oyj specializes in ophthalmological devices and software for diagnosing glaucoma, macular degeneration, and diabetic retinopathy, operating in Finland, Europe, North America, and internationally with a market cap of €679.28 million.

Operations: The company generates its revenue primarily from its Health Tech segment, which accounted for €103.82 million.

Estimated Discount To Fair Value: 37.1%

Revenio Group Oyj is trading at €25.54, significantly below its estimated fair value of €40.58, indicating it may be undervalued based on cash flows. Earnings are forecast to grow at 19.7% annually, outpacing the Finnish market's growth rate of 11.4%. However, revenue growth is slower than earnings at 12.3% per year but still surpasses the market average of 3.7%. Recent earnings show stable sales growth to €103.5 million despite a slight dip in net income to €18.5 million.

- Insights from our recent growth report point to a promising forecast for Revenio Group Oyj's business outlook.

- Unlock comprehensive insights into our analysis of Revenio Group Oyj stock in this financial health report.

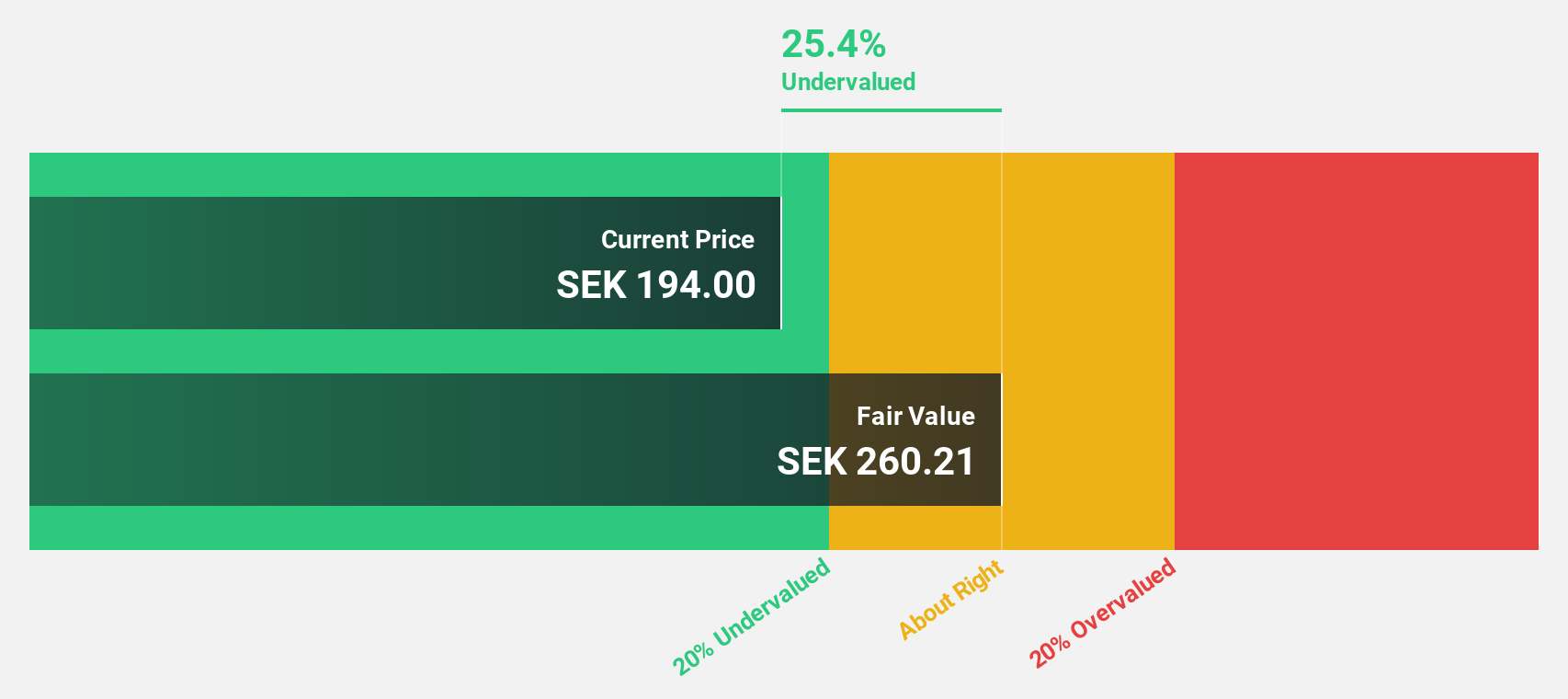

CellaVision (OM:CEVI)

Overview: CellaVision AB (publ) develops and sells instruments, software, and reagents for blood and body fluids analysis in Sweden and internationally, with a market cap of SEK4.08 billion.

Operations: The company's revenue primarily comes from Automated Microscopy Systems and Reagents in the field of Hematology, totaling SEK723.22 million.

Estimated Discount To Fair Value: 30.4%

CellaVision AB is trading at SEK 171, well below its estimated fair value of SEK 245.82, suggesting it is undervalued based on cash flows. Earnings are projected to grow at 19.8% annually, outstripping the Swedish market's growth rate of 9.1%. However, recent earnings show a decline in sales to SEK 186.69 million and net income to SEK 40.94 million for Q4 2024 compared to the previous year’s figures.

- The growth report we've compiled suggests that CellaVision's future prospects could be on the up.

- Click here to discover the nuances of CellaVision with our detailed financial health report.

Taking Advantage

- Gain an insight into the universe of 204 Undervalued European Stocks Based On Cash Flows by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Searching for a Fresh Perspective?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if TXT e-solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About BIT:TXT

TXT e-solutions

Provides software and service solutions in Italy and internationally.

Good value with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Rocket Lab USA Will Ignite a 30% Revenue Growth Journey

Fair Value US$31.72|41.9% undervalued

KI

Community Contributor

EasyJet weirdly unloved by investors in spite of relatively attractive metrics

Fair Value UK£6.95|31.9% undervalued

PI

Community Contributor

HEXPOL AB: Sustained Long Term Growth, Stable Margins, and Strategic M&A

Fair Value SEK 122.27|24.9% undervalued

MA

Community Contributor