- Italy

- /

- Consumer Finance

- /

- BIT:MOL

Moltiply Group (BIT:MOL) rallies 4.8% this week, taking five-year gains to 103%

When we invest, we're generally looking for stocks that outperform the market average. And the truth is, you can make significant gains if you buy good quality businesses at the right price. To wit, the Moltiply Group share price has climbed 97% in five years, easily topping the market return of 9.5% (ignoring dividends). On the other hand, the more recent gains haven't been so impressive, with shareholders gaining just 23%, including dividends.

The past week has proven to be lucrative for Moltiply Group investors, so let's see if fundamentals drove the company's five-year performance.

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. One way to examine how market sentiment has changed over time is to look at the interaction between a company's share price and its earnings per share (EPS).

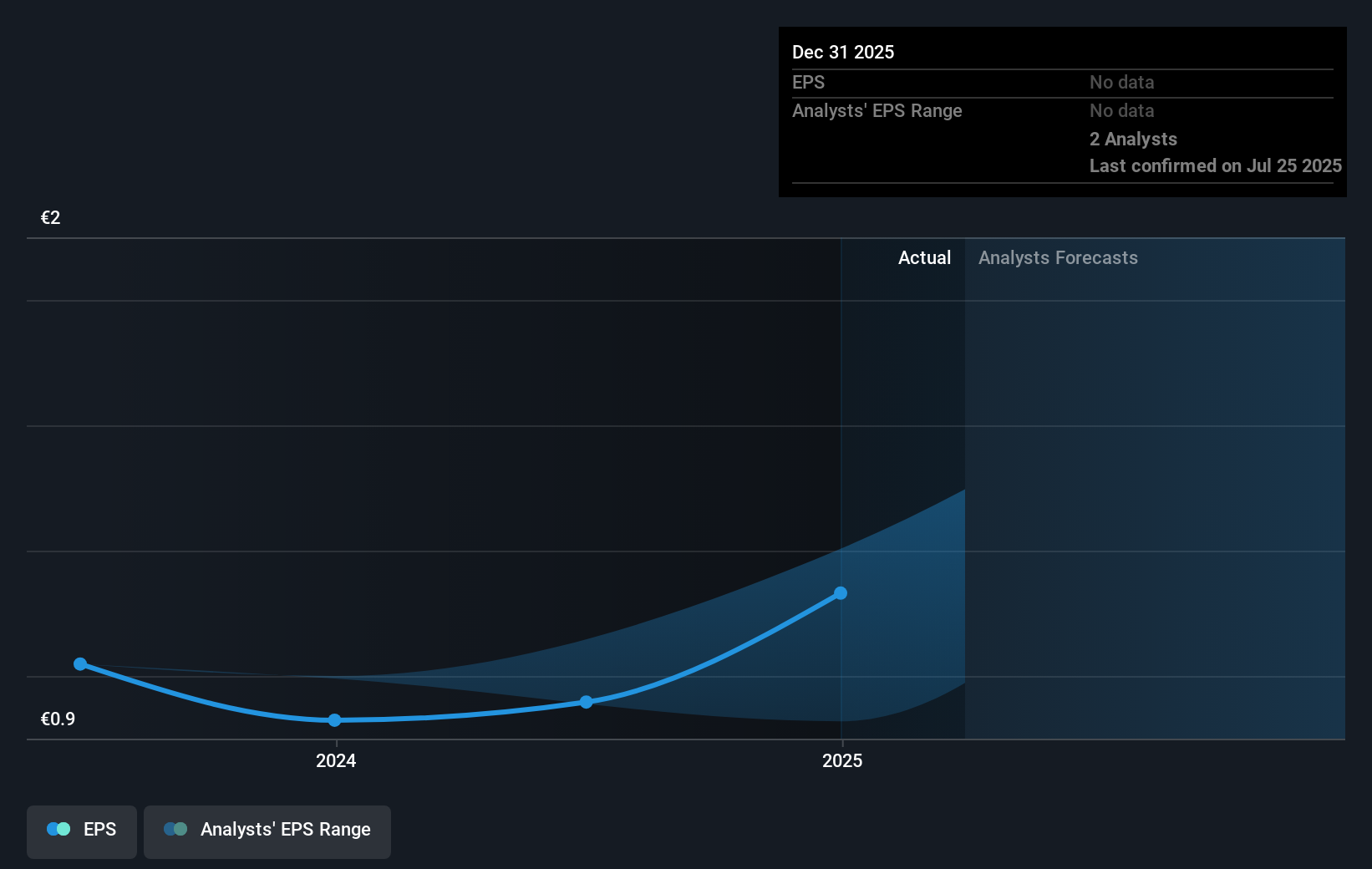

During the last half decade, Moltiply Group became profitable. That would generally be considered a positive, so we'd hope to see the share price to rise.

The company's earnings per share (over time) is depicted in the image below (click to see the exact numbers).

We know that Moltiply Group has improved its bottom line lately, but is it going to grow revenue? If you're interested, you could check this free report showing consensus revenue forecasts.

What About Dividends?

It is important to consider the total shareholder return, as well as the share price return, for any given stock. Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Moltiply Group the TSR over the last 5 years was 103%, which is better than the share price return mentioned above. This is largely a result of its dividend payments!

A Different Perspective

Moltiply Group shareholders are up 23% for the year (even including dividends). But that return falls short of the market. The silver lining is that the gain was actually better than the average annual return of 15% per year over five year. This suggests the company might be improving over time. It's always interesting to track share price performance over the longer term. But to understand Moltiply Group better, we need to consider many other factors. Case in point: We've spotted 1 warning sign for Moltiply Group you should be aware of.

Of course Moltiply Group may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Italian exchanges.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:MOL

Moltiply Group

A holding company that operates in the financial services industry.

High growth potential with proven track record.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)