- Italy

- /

- Food and Staples Retail

- /

- BIT:MARR

MARR S.p.A. (BIT:MARR) Released Earnings Last Week And Analysts Lifted Their Price Target To €20.30

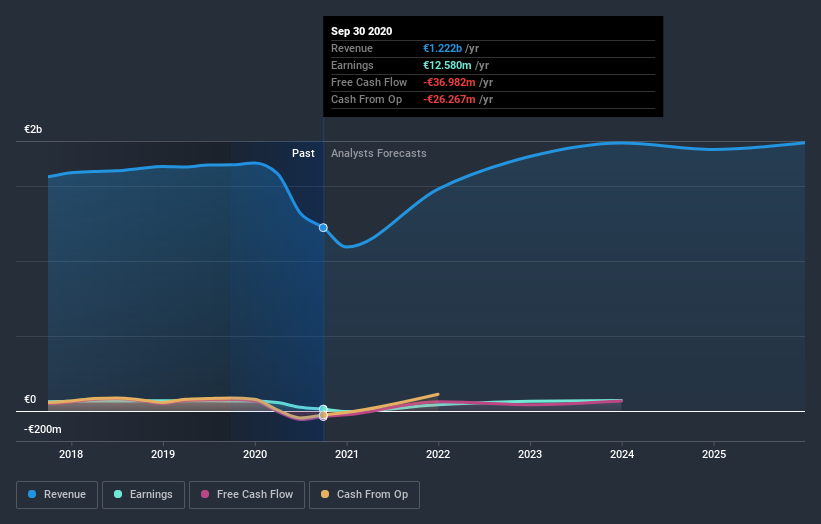

Shareholders might have noticed that MARR S.p.A. (BIT:MARR) filed its annual result this time last week. The early response was not positive, with shares down 8.6% to €18.10 in the past week. Revenues were €1.2b, and MARR came in a solid 12% ahead of expectations. This is an important time for investors, as they can track a company's performance in its report, look at what experts are forecasting for next year, and see if there has been any change to expectations for the business. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

Check out our latest analysis for MARR

Taking into account the latest results, the most recent consensus for MARR from four analysts is for revenues of €1.48b in 2021 which, if met, would be a huge 21% increase on its sales over the past 12 months. Statutory earnings per share are predicted to shoot up 227% to €0.62. Before this earnings report, the analysts had been forecasting revenues of €1.49b and earnings per share (EPS) of €0.73 in 2021. The analysts seem to have become more bearish following the latest results. While there were no changes to revenue forecasts, there was a substantial drop in EPS estimates.

Despite cutting their earnings forecasts,the analysts have lifted their price target 8.6% to €20.30, suggesting that these impacts are not expected to weigh on the stock's value in the long term. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values MARR at €23.00 per share, while the most bearish prices it at €15.80. These price targets show that analysts do have some differing views on the business, but the estimates do not vary enough to suggest to us that some are betting on wild success or utter failure.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's clear from the latest estimates that MARR's rate of growth is expected to accelerate meaningfully, with the forecast 21% annualised revenue growth to the end of 2021 noticeably faster than its historical growth of 0.2% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 3.7% annually. It seems obvious that, while the growth outlook is brighter than the recent past, the analysts also expect MARR to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for MARR. Fortunately, they also reconfirmed their revenue numbers, suggesting sales are tracking in line with expectations - and our data suggests that revenues are expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that in mind, we wouldn't be too quick to come to a conclusion on MARR. Long-term earnings power is much more important than next year's profits. At Simply Wall St, we have a full range of analyst estimates for MARR going out to 2025, and you can see them free on our platform here..

Plus, you should also learn about the 3 warning signs we've spotted with MARR (including 1 which is a bit concerning) .

If you decide to trade MARR, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About BIT:MARR

MARR

Engages in marketing and distribution of fresh, dried, and frozen food products for catering in Italy, the European Union, and internationally.

Good value with adequate balance sheet.

Similar Companies

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fiverr International will transform the freelance industry with AI-powered growth

Jackson Financial Stock: When Insurance Math Meets a Shifting Claims Landscape

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion