Advertisement

Pattern S.p.A.'s (BIT:PTR) P/E Is Still On The Mark Following 26% Share Price Bounce

Those holding Pattern S.p.A. (BIT:PTR) shares would be relieved that the share price has rebounded 26% in the last thirty days, but it needs to keep going to repair the recent damage it has caused to investor portfolios. Looking further back, the 11% rise over the last twelve months isn't too bad notwithstanding the strength over the last 30 days.

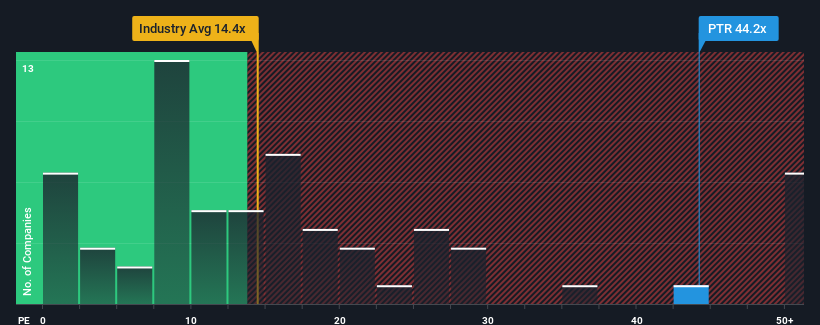

Following the firm bounce in price, Pattern's price-to-earnings (or "P/E") ratio of 44.2x might make it look like a strong sell right now compared to the market in Italy, where around half of the companies have P/E ratios below 14x and even P/E's below 8x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so lofty.

Pattern could be doing better as its earnings have been going backwards lately while most other companies have been seeing positive earnings growth. It might be that many expect the dour earnings performance to recover substantially, which has kept the P/E from collapsing. If not, then existing shareholders may be extremely nervous about the viability of the share price.

Check out our latest analysis for Pattern

What Are Growth Metrics Telling Us About The High P/E?

There's an inherent assumption that a company should far outperform the market for P/E ratios like Pattern's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 37% decrease to the company's bottom line. This means it has also seen a slide in earnings over the longer-term as EPS is down 37% in total over the last three years. Therefore, it's fair to say the earnings growth recently has been undesirable for the company.

Looking ahead now, EPS is anticipated to climb by 28% per year during the coming three years according to the two analysts following the company. That's shaping up to be materially higher than the 15% each year growth forecast for the broader market.

In light of this, it's understandable that Pattern's P/E sits above the majority of other companies. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Pattern's P/E?

The strong share price surge has got Pattern's P/E rushing to great heights as well. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

As we suspected, our examination of Pattern's analyst forecasts revealed that its superior earnings outlook is contributing to its high P/E. Right now shareholders are comfortable with the P/E as they are quite confident future earnings aren't under threat. Unless these conditions change, they will continue to provide strong support to the share price.

Before you take the next step, you should know about the 3 warning signs for Pattern (1 is concerning!) that we have uncovered.

If you're unsure about the strength of Pattern's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:PTR

Pattern

Engages in engineering, prototyping, and production of luxury goods in Italy, rest of the European Union, and internationally.

Good value with moderate growth potential.

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Cue Biopharma ·

Cue Biopharma (NASDAQ: CUE): The Scientist Behind Xolair Just Gave Cue a Next-Generation Shot at the Same Multi-Billion-Dollar Market

Fair Value:US$7056.5% undervalued

25 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$317.225.0% undervalued

28 followersusers have followed this narrative

7 commentsusers have commented on this narrative

9 likesusers have liked this narrative

NI

niteco on Broadcom ·

A Capital Allocation Favorite with Structural Importance

Fair Value:US$651.0539.8% undervalued

26 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

TO

Tokyo on Okta ·

Good foundation, but now it's all about the next steps

Fair Value:US$15120.6% undervalued

83 followersusers have followed this narrative

7 commentsusers have commented on this narrative

11 likesusers have liked this narrative

Recently Updated Narratives

TE

Terence on Zenith Bank ·

Zenith Bank's Revenue To Surge by 18% in the Coming Years

Fair Value:₦93.5936.4% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥4.05k29.1% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

RO

RockeTeller on 1911 Gold ·

1911 Gold, This Junior Gold Stock Has a 105% IRR and a 2027 Production Target

Fair Value:CA$12.7295.1% undervalued

87 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7447.8% undervalued

58 followersusers have followed this narrative

0 commentsusers have commented on this narrative

15 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9723.4% undervalued

57 followersusers have followed this narrative

0 commentsusers have commented on this narrative

14 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1932.6% undervalued

48 followersusers have followed this narrative

0 commentsusers have commented on this narrative

19 likesusers have liked this narrative

Trending Discussion

SI

Simply Wall St User on Access Holdings ·

It's wonderful. It has greatly helped me take informed decisions.

1

|0