Advertisement

Shareholders Will Probably Hold Off On Increasing UniCredit S.p.A.'s (BIT:UCG) CEO Compensation For The Time Being

Key Insights

- UniCredit to hold its Annual General Meeting on 27th of October

- Salary of €2.00m is part of CEO Andrea Orcel's total remuneration

- Total compensation is 46% above industry average

- UniCredit's EPS grew by 102% over the past three years while total shareholder return over the past three years was 260%

Performance at UniCredit S.p.A. (BIT:UCG) has been reasonably good and CEO Andrea Orcel has done a decent job of steering the company in the right direction. As shareholders go into the upcoming AGM on 27th of October, CEO compensation will probably not be their focus, but rather the steps management will take to continue the growth momentum. However, some shareholders may still want to keep CEO compensation within reason.

Check out our latest analysis for UniCredit

Comparing UniCredit S.p.A.'s CEO Compensation With The Industry

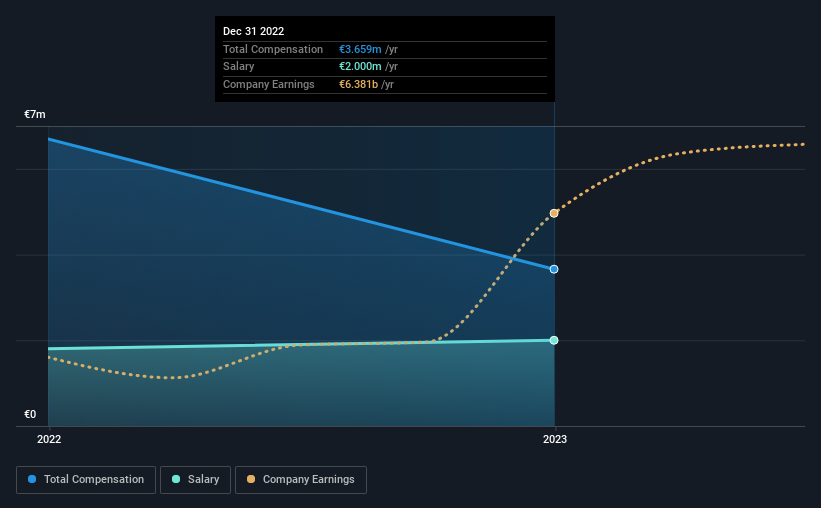

According to our data, UniCredit S.p.A. has a market capitalization of €39b, and paid its CEO total annual compensation worth €3.7m over the year to December 2022. That's a notable decrease of 45% on last year. In particular, the salary of €2.00m, makes up a fairly large portion of the total compensation being paid to the CEO.

On comparing similar companies in the Italian Banks industry with market capitalizations above €7.6b, we found that the median total CEO compensation was €2.5m. This suggests that Andrea Orcel is paid more than the median for the industry.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | €2.0m | €1.8m | 55% |

| Other | €1.7m | €4.9m | 45% |

| Total Compensation | €3.7m | €6.7m | 100% |

On an industry level, around 42% of total compensation represents salary and 58% is other remuneration. UniCredit is paying a higher share of its remuneration through a salary in comparison to the overall industry. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

UniCredit S.p.A.'s Growth

Over the past three years, UniCredit S.p.A. has seen its earnings per share (EPS) grow by 102% per year. Its revenue is up 48% over the last year.

This demonstrates that the company has been improving recently and is good news for the shareholders. Most shareholders would be pleased to see strong revenue growth combined with EPS growth. This combo suggests a fast growing business. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has UniCredit S.p.A. Been A Good Investment?

Boasting a total shareholder return of 260% over three years, UniCredit S.p.A. has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. However, if the board proposes to increase the compensation, some shareholders might have questions given that the CEO is already being paid higher than the industry.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. We did our research and identified 2 warning signs (and 1 which is a bit concerning) in UniCredit we think you should know about.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About BIT:UCG

UniCredit

Provides commercial banking services in Italy, Germany, Central Europe, and Eastern Europe.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor