Advertisement

- India

- /

- Electric Utilities

- /

- NSEI:TORNTPOWER

Torrent Power Limited Just Missed Earnings - But Analysts Have Updated Their Models

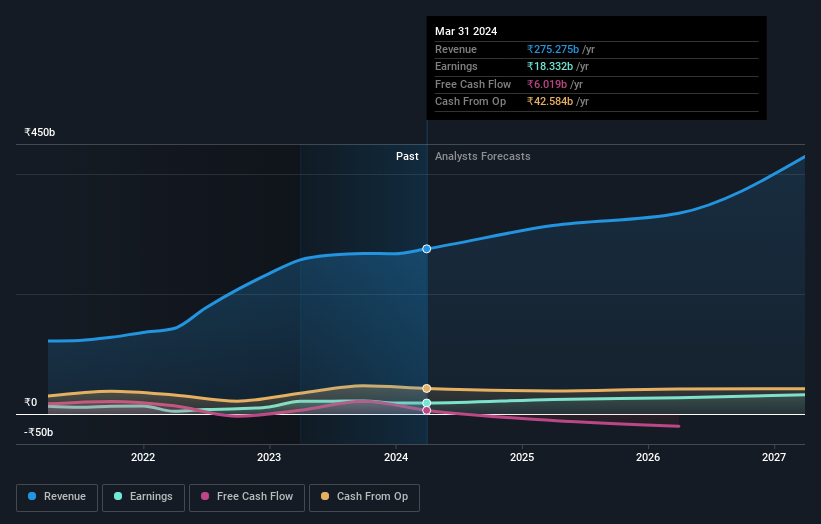

As you might know, Torrent Power Limited (NSE:TORNTPOWER) last week released its latest annual, and things did not turn out so great for shareholders. Torrent Power missed analyst forecasts, with revenues of ₹275b and statutory earnings per share (EPS) of ₹38.14, falling short by 2.2% and 8.7% respectively. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Torrent Power after the latest results.

Check out our latest analysis for Torrent Power

Taking into account the latest results, the current consensus from Torrent Power's nine analysts is for revenues of ₹314.1b in 2025. This would reflect a decent 14% increase on its revenue over the past 12 months. Per-share earnings are expected to leap 33% to ₹50.56. Before this earnings report, the analysts had been forecasting revenues of ₹298.5b and earnings per share (EPS) of ₹52.37 in 2025. So it's pretty clear consensus is mixed on Torrent Power after the latest results; whilethe analysts lifted revenue numbers, they also administered a minor downgrade to per-share earnings expectations.

Curiously, the consensus price target rose 12% to ₹1,119. We can only conclude that the forecast revenue growth is expected to offset the impact of the expected fall in earnings. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Torrent Power analyst has a price target of ₹1,560 per share, while the most pessimistic values it at ₹750. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's pretty clear that there is an expectation that Torrent Power's revenue growth will slow down substantially, with revenues to the end of 2025 expected to display 14% growth on an annualised basis. This is compared to a historical growth rate of 19% over the past five years. Juxtapose this against the other companies in the industry with analyst coverage, which are forecast to grow their revenues (in aggregate) 11% per year. Even after the forecast slowdown in growth, it seems obvious that Torrent Power is also expected to grow faster than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Torrent Power. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. At Simply Wall St, we have a full range of analyst estimates for Torrent Power going out to 2027, and you can see them free on our platform here..

Plus, you should also learn about the 2 warning signs we've spotted with Torrent Power .

Valuation is complex, but we're here to simplify it.

Discover if Torrent Power might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TORNTPOWER

Torrent Power

Engages in the generation, transmission, and distribution of electricity in India.

Solid track record with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor