Advertisement

Earnings Beat: Tata Elxsi Limited Just Beat Analyst Forecasts, And Analysts Have Been Updating Their Models

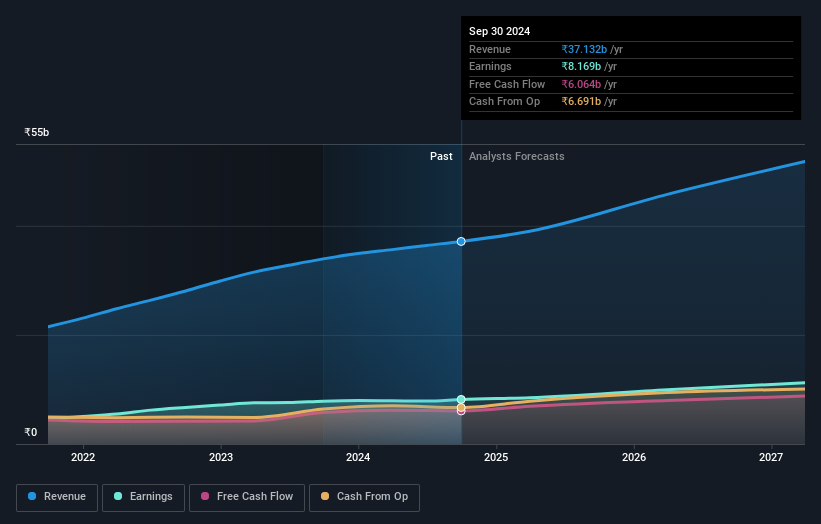

Last week saw the newest quarterly earnings release from Tata Elxsi Limited (NSE:TATAELXSI), an important milestone in the company's journey to build a stronger business. It looks like a credible result overall - although revenues of ₹9.6b were in line with what the analysts predicted, Tata Elxsi surprised by delivering a statutory profit of ₹36.83 per share, a notable 10% above expectations. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

Check out our latest analysis for Tata Elxsi

Taking into account the latest results, the consensus forecast from Tata Elxsi's 15 analysts is for revenues of ₹39.0b in 2025. This reflects a satisfactory 5.0% improvement in revenue compared to the last 12 months. Per-share earnings are expected to increase 3.8% to ₹136. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹39.0b and earnings per share (EPS) of ₹135 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

It will come as no surprise then, to learn that the consensus price target is largely unchanged at ₹6,845. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Tata Elxsi, with the most bullish analyst valuing it at ₹8,961 and the most bearish at ₹5,509 per share. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We would highlight that Tata Elxsi's revenue growth is expected to slow, with the forecast 10% annualised growth rate until the end of 2025 being well below the historical 20% p.a. growth over the last five years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 15% per year. Factoring in the forecast slowdown in growth, it seems obvious that Tata Elxsi is also expected to grow slower than other industry participants.

The Bottom Line

The most obvious conclusion is that there's been no major change in the business' prospects in recent times, with the analysts holding their earnings forecasts steady, in line with previous estimates. On the plus side, there were no major changes to revenue estimates; although forecasts imply they will perform worse than the wider industry. The consensus price target held steady at ₹6,845, with the latest estimates not enough to have an impact on their price targets.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Tata Elxsi going out to 2027, and you can see them free on our platform here..

You still need to take note of risks, for example - Tata Elxsi has 1 warning sign we think you should be aware of.

Valuation is complex, but we're here to simplify it.

Discover if Tata Elxsi might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TATAELXSI

Tata Elxsi

Engages in the provision of product design and engineering, and systems integration and support services in India, the United States, Europe, and internationally.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor