Advertisement

Is Persistent Systems Limited (NSE:PERSISTENT) Popular Amongst Insiders?

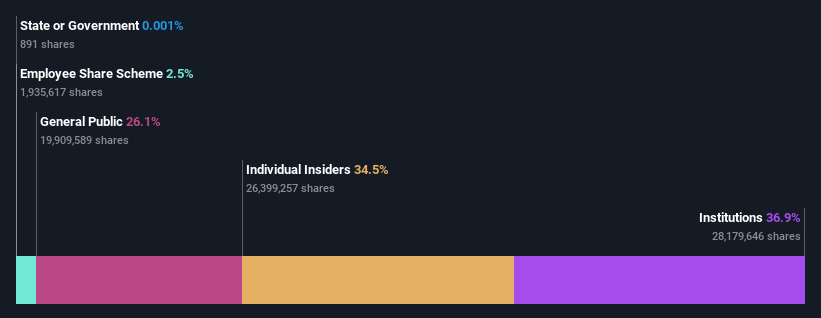

A look at the shareholders of Persistent Systems Limited (NSE:PERSISTENT) can tell us which group is most powerful. Institutions often own shares in more established companies, while it's not unusual to see insiders own a fair bit of smaller companies. I quite like to see at least a little bit of insider ownership. As Charlie Munger said 'Show me the incentive and I will show you the outcome.

With a market capitalization of ₹250b, Persistent Systems is rather large. We'd expect to see institutional investors on the register. Companies of this size are usually well known to retail investors, too. In the chart below, we can see that institutional investors have bought into the company. We can zoom in on the different ownership groups, to learn more about Persistent Systems.

View our latest analysis for Persistent Systems

What Does The Institutional Ownership Tell Us About Persistent Systems?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

As you can see, institutional investors have a fair amount of stake in Persistent Systems. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see Persistent Systems' historic earnings and revenue below, but keep in mind there's always more to the story.

We note that hedge funds don't have a meaningful investment in Persistent Systems. Because actions speak louder than words, we consider it a good sign when insiders own a significant stake in a company. In Persistent Systems' case, its Top Key Executive, Anand Deshpande, is the largest shareholder, holding 15% of shares outstanding. In comparison, the second and third largest shareholders hold about 15% and 5.0% of the stock.

We also observed that the top 9 shareholders account for more than half of the share register, with a few smaller shareholders to balance the interests of the larger ones to a certain extent.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of Persistent Systems

The definition of an insider can differ slightly between different countries, but members of the board of directors always count. Company management run the business, but the CEO will answer to the board, even if he or she is a member of it.

Most consider insider ownership a positive because it can indicate the board is well aligned with other shareholders. However, on some occasions too much power is concentrated within this group.

Our most recent data indicates that insiders own a reasonable proportion of Persistent Systems Limited. Insiders own ₹86b worth of shares in the ₹250b company. That's quite meaningful. Most would be pleased to see the board is investing alongside them. You may wish to access this free chart showing recent trading by insiders.

General Public Ownership

With a 26% ownership, the general public, mostly comprising of individual investors, have some degree of sway over Persistent Systems. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Persistent Systems , and understanding them should be part of your investment process.

But ultimately it is the future, not the past, that will determine how well the owners of this business will do. Therefore we think it advisable to take a look at this free report showing whether analysts are predicting a brighter future.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:PERSISTENT

Persistent Systems

Provides software products, services, and technology solutions in India, North America, and internationally.

Outstanding track record with flawless balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

72 followersusers have followed this narrative

5 commentsusers have commented on this narrative

34 likesusers have liked this narrative

WO

woodworthfund on Bumble ·

Swiped Left by Wall Street: The BMBL Rebound Trade

Fair Value:US$960.1% undervalued

22 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

WE

WealthAP on Duolingo ·

Duolingo (DUOL): Why A 20% Drop Might Be The Entry Point We've Been Waiting For

Fair Value:US$268.6441.8% undervalued

43 followersusers have followed this narrative

5 commentsusers have commented on this narrative

9 likesusers have liked this narrative

AN

andre_santos on Ferrari ·

Ferrari's Intrinsic and Historical Valuation

Fair Value:€243.5626.4% overvalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

Recently Updated Narratives

AN

andre_santos on Adobe ·

Adobe - A Fundamental and Historical Valuation

Fair Value:US$356.9814.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

LE

LeStockPicker on Novo Nordisk ·

Probably the best stock I've seen all year.

Fair Value:DKK 90058.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

DE

Deep_Insights on Hims & Hers Health ·

Hims & Hers Health aims for three dimensional revenue expansion

Fair Value:US$173.0281.9% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

WE

WealthAP on PayPal Holdings ·

The "Sleeping Giant" Stumbles, Then Wakes Up

Fair Value:US$8229.7% undervalued

72 followersusers have followed this narrative

5 commentsusers have commented on this narrative

34 likesusers have liked this narrative

AG

Agricola on Excellon Resources ·

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Fair Value:CA$31.898.3% undervalued

72 followersusers have followed this narrative

15 commentsusers have commented on this narrative

23 likesusers have liked this narrative

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25464.9% overvalued

75 followersusers have followed this narrative

1 commentusers have commented on this narrative

18 likesusers have liked this narrative

Trending Discussion

WA

Wane_Investment_House on Airtel Africa ·

Airtel Africa Plc – Recalibrated Valuation Highlights Compelling Relative Value Equity analysts highlight that Airtel’s stock remains undervalued relative to regional peers, presenting an attractive entry point for investors seeking exposure to a resilient, data-driven telecom business. Strategic Insights • Revenue Mix Transformation: The transition from voice to data highlights Airtel’s alignment with global telecom trends and positions the company to capture higher-margin opportunities in mobile data and digital services. • Operational Levers: Subscriber growth, tariff adjustments, and disciplined cost management provide a solid foundation for near-term growth. • Valuation Drivers: Adjustments to the equity risk premium (13.8% vs. 14.3%) and lower yields on Nigeria’s 10-year Eurobond (7.7% vs. 10.4%) have slightly tempered valuation, but the fundamentals remain strong. Analyst Commentary • Near-term Upside: The revised target price suggests significant potential gains, particularly given Airtel’s operational resilience and structural growth in data usage. • Investment Considerations: Investors seeking exposure to defensive growth in telecom should view Airtel as a long-term opportunity, with upside supported by undervaluation relative to regional peers. • Risk Factors: Currency appreciation (Naira strength), potential regulatory changes, and macroeconomic volatility remain key considerations for risk-adjusted returns. Conclusion Airtel Africa Plc combines robust operational performance, a favorable shift to data revenue, and strategic macro positioning with an undervalued stock price relative to peers. Despite muted market response in 2025, the recalibrated target price and potential upside of 72% underscore Airtel’s attractiveness for long-term investors seeking resilient, growth-oriented exposure in the African telecom sector.

0

|0