David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We can see that LTIMindtree Limited (NSE:LTIM) does use debt in its business. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for LTIMindtree

What Is LTIMindtree's Net Debt?

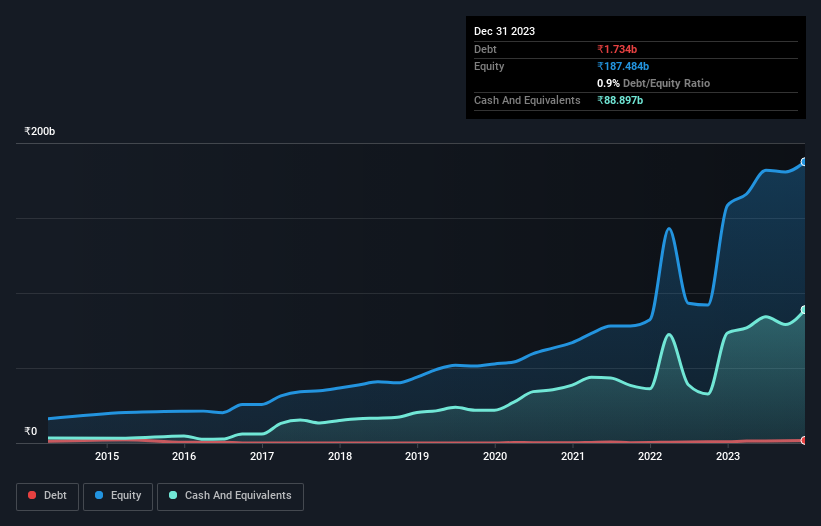

As you can see below, at the end of December 2023, LTIMindtree had ₹1.73b of debt, up from ₹810.0m a year ago. Click the image for more detail. But it also has ₹88.9b in cash to offset that, meaning it has ₹87.2b net cash.

How Healthy Is LTIMindtree's Balance Sheet?

We can see from the most recent balance sheet that LTIMindtree had liabilities of ₹54.0b falling due within a year, and liabilities of ₹13.4b due beyond that. Offsetting this, it had ₹88.9b in cash and ₹71.9b in receivables that were due within 12 months. So it actually has ₹93.4b more liquid assets than total liabilities.

This surplus suggests that LTIMindtree has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Simply put, the fact that LTIMindtree has more cash than debt is arguably a good indication that it can manage its debt safely.

On top of that, LTIMindtree grew its EBIT by 72% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if LTIMindtree can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. LTIMindtree may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the most recent three years, LTIMindtree recorded free cash flow worth 63% of its EBIT, which is around normal, given free cash flow excludes interest and tax. This cold hard cash means it can reduce its debt when it wants to.

Summing Up

While it is always sensible to investigate a company's debt, in this case LTIMindtree has ₹87.2b in net cash and a decent-looking balance sheet. And we liked the look of last year's 72% year-on-year EBIT growth. So we don't think LTIMindtree's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately, every company can contain risks that exist outside of the balance sheet. For instance, we've identified 2 warning signs for LTIMindtree that you should be aware of.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:LTIM

LTIMindtree

A technology consulting and digital solutions company, provides information technology services and solutions in India, North America, Europe, and internationally.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Community Narratives