Advertisement

Has Dev Information Technology Limited's (NSE:DEVIT) Impressive Stock Performance Got Anything to Do With Its Fundamentals?

Dev Information Technology's (NSE:DEVIT) stock is up by a considerable 9.3% over the past month. Given that stock prices are usually aligned with a company's financial performance in the long-term, we decided to study its financial indicators more closely to see if they had a hand to play in the recent price move. Particularly, we will be paying attention to Dev Information Technology's ROE today.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

Check out our latest analysis for Dev Information Technology

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Dev Information Technology is:

6.8% = ₹24m ÷ ₹344m (Based on the trailing twelve months to September 2020).

The 'return' is the profit over the last twelve months. One way to conceptualize this is that for each ₹1 of shareholders' capital it has, the company made ₹0.07 in profit.

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

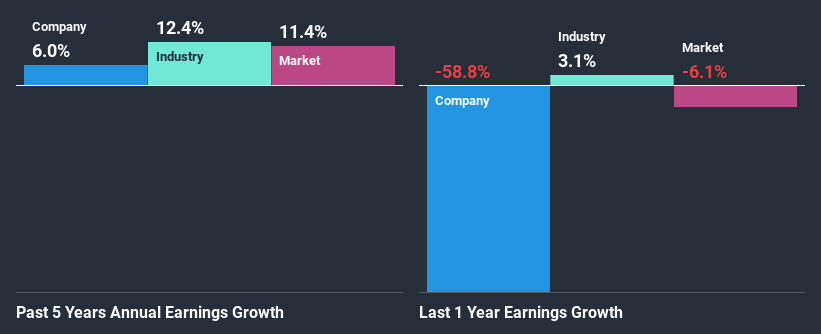

A Side By Side comparison of Dev Information Technology's Earnings Growth And 6.8% ROE

It is hard to argue that Dev Information Technology's ROE is much good in and of itself. Even compared to the average industry ROE of 9.6%, the company's ROE is quite dismal. Although, we can see that Dev Information Technology saw a modest net income growth of 6.0% over the past five years. We believe that there might be other aspects that are positively influencing the company's earnings growth. Such as - high earnings retention or an efficient management in place.

As a next step, we compared Dev Information Technology's net income growth with the industry and were disappointed to see that the company's growth is lower than the industry average growth of 12% in the same period.

Earnings growth is a huge factor in stock valuation. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. Doing so will help them establish if the stock's future looks promising or ominous. If you're wondering about Dev Information Technology's's valuation, check out this gauge of its price-to-earnings ratio, as compared to its industry.

Is Dev Information Technology Efficiently Re-investing Its Profits?

Dev Information Technology has a low three-year median payout ratio of 7.2%, meaning that the company retains the remaining 93% of its profits. This suggests that the management is reinvesting most of the profits to grow the business.

Besides, Dev Information Technology has been paying dividends over a period of three years. This shows that the company is committed to sharing profits with its shareholders.

Summary

Overall, we feel that Dev Information Technology certainly does have some positive factors to consider. That is, a decent growth in earnings backed by a high rate of reinvestment. However, we do feel that that earnings growth could have been higher if the business were to improve on the low ROE rate. Especially given how the company is reinvesting a huge chunk of its profits. While we won't completely dismiss the company, what we would do, is try to ascertain how risky the business is to make a more informed decision around the company. You can see the 3 risks we have identified for Dev Information Technology by visiting our risks dashboard for free on our platform here.

If you’re looking to trade Dev Information Technology, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:DEVIT

Dev Information Technology

Provides information technology enabled services in India, Europe, and internationally.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

ST

stuart_roberts on Upside Gold ·

An Undervalued 3.3Moz Gold Project in Canada

Fair Value:CA$5.0768.0% undervalued

278 followersusers have followed this narrative

1 commentusers have commented on this narrative

40 likesusers have liked this narrative

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8591.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

19 likesusers have liked this narrative

TO

Tokyo on Anheuser-Busch InBev ·

EU#8 - Anheuser-Busch InBev: Courage, Capital, and the Discipline to Build an Empire

Fair Value:€89.4521.3% undervalued

4 followersusers have followed this narrative

3 commentsusers have commented on this narrative

2 likesusers have liked this narrative

OS

oscargarcia on Amazon.com ·

The capitalist colossus that makes your parcels magically appear, powers half the internet, and knows your shopping habits.

Fair Value:US$2802.3% undervalued

59 followersusers have followed this narrative

1 commentusers have commented on this narrative

2 likesusers have liked this narrative

Recently Updated Narratives

CH

Chimichanga696 on Bajaj Auto ·

Bajaj Auto has seen a correction in its stock price after a strong rally, making it an attractive opportunity for investors.

Fair Value:₹15k31.2% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RO

RockeTeller on Barton Gold Holdings ·

Aussie’s Barton Gold, No Debt Miner with 1 Mill That Changes Everything

Fair Value:AU$22.4495.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MR

MRT23 on Ategrity Specialty Insurance Company Holdings ·

ASIC is a technology-differentiated E&S insurer compounding book value with a structurally improving combined ratio

Fair Value:US$3035.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KI

Kingman1152 on NVIDIA ·

NVIDIA will see a profit margin surge of 55% in the next 5 years

Fair Value:US$305.235.6% undervalued

69 followersusers have followed this narrative

2 commentsusers have commented on this narrative

24 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$561.9326.8% undervalued

1396 followersusers have followed this narrative

2 commentsusers have commented on this narrative

12 likesusers have liked this narrative

TR

tripledub on Meta Platforms ·

The $135 Billion Bet That Should Make Every Shareholder Nervous

Fair Value:US$74018.2% undervalued

31 followersusers have followed this narrative

3 commentsusers have commented on this narrative

32 likesusers have liked this narrative