Advertisement

- India

- /

- Specialty Stores

- /

- NSEI:NYKAA

Investors Will Want FSN E-Commerce Ventures' (NSE:NYKAA) Growth In ROCE To Persist

What trends should we look for it we want to identify stocks that can multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. So on that note, FSN E-Commerce Ventures (NSE:NYKAA) looks quite promising in regards to its trends of return on capital.

Return On Capital Employed (ROCE): What Is It?

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. Analysts use this formula to calculate it for FSN E-Commerce Ventures:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

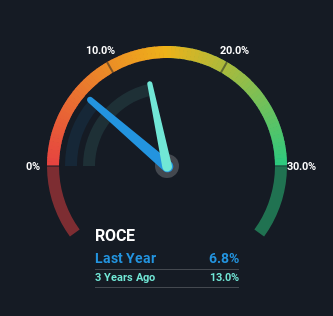

0.068 = ₹1.1b ÷ (₹31b - ₹15b) (Based on the trailing twelve months to December 2023).

Therefore, FSN E-Commerce Ventures has an ROCE of 6.8%. Ultimately, that's a low return and it under-performs the Specialty Retail industry average of 17%.

View our latest analysis for FSN E-Commerce Ventures

In the above chart we have measured FSN E-Commerce Ventures' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering FSN E-Commerce Ventures here for free.

So How Is FSN E-Commerce Ventures' ROCE Trending?

While in absolute terms it isn't a high ROCE, it's promising to see that it has been moving in the right direction. The numbers show that in the last four years, the returns generated on capital employed have grown considerably to 6.8%. The company is effectively making more money per dollar of capital used, and it's worth noting that the amount of capital has increased too, by 316%. So we're very much inspired by what we're seeing at FSN E-Commerce Ventures thanks to its ability to profitably reinvest capital.

In another part of our analysis, we noticed that the company's ratio of current liabilities to total assets decreased to 49%, which broadly means the business is relying less on its suppliers or short-term creditors to fund its operations. Therefore we can rest assured that the growth in ROCE is a result of the business' fundamental improvements, rather than a cooking class featuring this company's books. However, current liabilities are still at a pretty high level, so just be aware that this can bring with it some risks.

In Conclusion...

All in all, it's terrific to see that FSN E-Commerce Ventures is reaping the rewards from prior investments and is growing its capital base. And investors seem to expect more of this going forward, since the stock has rewarded shareholders with a 7.0% return over the last year. In light of that, we think it's worth looking further into this stock because if FSN E-Commerce Ventures can keep these trends up, it could have a bright future ahead.

While FSN E-Commerce Ventures looks impressive, no company is worth an infinite price. The intrinsic value infographic in our free research report helps visualize whether NYKAA is currently trading for a fair price.

While FSN E-Commerce Ventures isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NYKAA

FSN E-Commerce Ventures

Through its subsidiaries, provides a range of beauty, personal care, and fashion products for women, men, kids, and home in India and internationally.

Exceptional growth potential with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|18.2% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|12.1% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.4% undervalued

NO

Community Contributor