Advertisement

Increases to CEO Compensation Might Be Put On Hold For Now at Morepen Laboratories Limited (NSE:MOREPENLAB)

Key Insights

- Morepen Laboratories to hold its Annual General Meeting on 28th of September

- Salary of ₹43.8m is part of CEO Sushil Suri's total remuneration

- Total compensation is 173% above industry average

- Morepen Laboratories' EPS declined by 2.7% over the past three years while total shareholder return over the past three years was 63%

The share price of Morepen Laboratories Limited (NSE:MOREPENLAB) has increased significantly over the past few years. However, the earnings growth has not kept up with the share price momentum, suggesting that some other factors may be driving the price direction. The upcoming AGM on 28th of September may be an opportunity for shareholders to bring up any concerns they may have for the board’s attention. They will be able to influence managerial decisions through the exercise of their voting power on resolutions, such as CEO remuneration and other matters, which may influence future company prospects. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

See our latest analysis for Morepen Laboratories

Comparing Morepen Laboratories Limited's CEO Compensation With The Industry

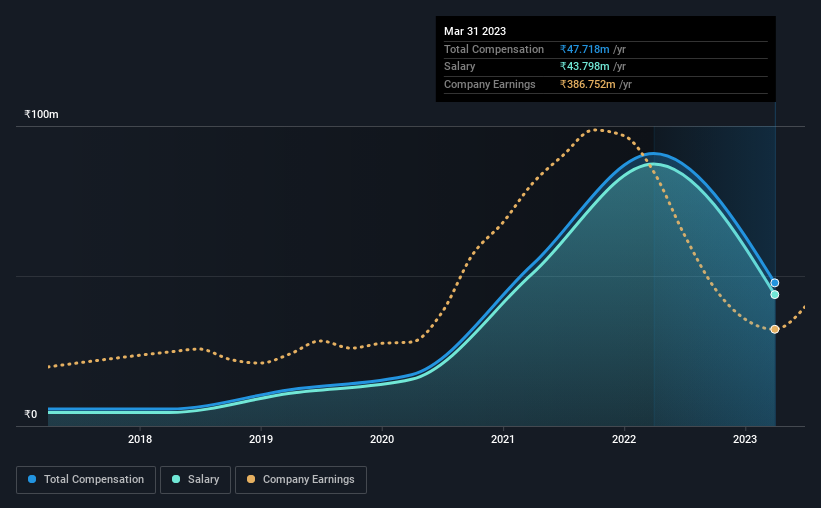

According to our data, Morepen Laboratories Limited has a market capitalization of ₹19b, and paid its CEO total annual compensation worth ₹48m over the year to March 2023. Notably, that's a decrease of 47% over the year before. In particular, the salary of ₹43.8m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Indian Pharmaceuticals industry with market capitalizations ranging between ₹8.3b and ₹33b had a median total CEO compensation of ₹17m. Hence, we can conclude that Sushil Suri is remunerated higher than the industry median. Furthermore, Sushil Suri directly owns ₹245m worth of shares in the company, implying that they are deeply invested in the company's success.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | ₹44m | ₹87m | 92% |

| Other | ₹3.9m | ₹3.5m | 8% |

| Total Compensation | ₹48m | ₹91m | 100% |

Talking in terms of the industry, salary represented approximately 96% of total compensation out of all the companies we analyzed, while other remuneration made up 4% of the pie. Morepen Laboratories is largely mirroring the industry average when it comes to the share a salary enjoys in overall compensation. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Morepen Laboratories Limited's Growth

Over the last three years, Morepen Laboratories Limited has shrunk its earnings per share by 2.7% per year. Its revenue is up 3.5% over the last year.

A lack of EPS improvement is not good to see. And the modest revenue growth over 12 months isn't much comfort against the reduced EPS. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Morepen Laboratories Limited Been A Good Investment?

We think that the total shareholder return of 63%, over three years, would leave most Morepen Laboratories Limited shareholders smiling. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean returns may be hard to keep up. In the upcoming AGM, shareholders will get the opportunity to discuss any concerns with the board, including those related to CEO remuneration and assess if the board's plan will likely improve performance in the future.

While CEO pay is an important factor to be aware of, there are other areas that investors should be mindful of as well. That's why we did some digging and identified 1 warning sign for Morepen Laboratories that you should be aware of before investing.

Switching gears from Morepen Laboratories, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MOREPENLAB

Morepen Laboratories

Develops, manufactures, markets, and sells active pharmaceutical ingredients (APIs), formulations, and home health products in India, the United States, and internationally.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|29.6% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|49.1% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|35.4% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|54.5% undervalued

AX

Community Contributor