Advertisement

We Think Marksans Pharma (NSE:MARKSANS) Can Manage Its Debt With Ease

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Marksans Pharma Limited (NSE:MARKSANS) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Marksans Pharma

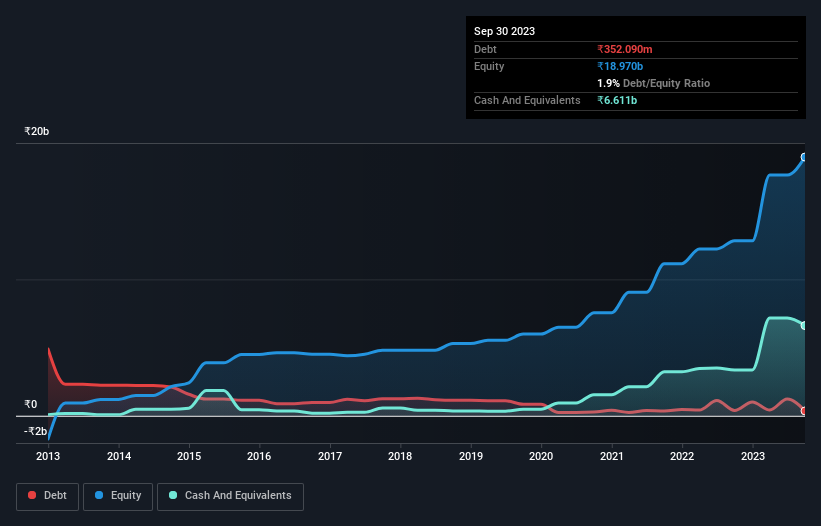

What Is Marksans Pharma's Net Debt?

As you can see below, Marksans Pharma had ₹352.1m of debt at September 2023, down from ₹390.9m a year prior. However, it does have ₹6.61b in cash offsetting this, leading to net cash of ₹6.26b.

How Strong Is Marksans Pharma's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Marksans Pharma had liabilities of ₹3.33b due within 12 months and liabilities of ₹838.2m due beyond that. On the other hand, it had cash of ₹6.61b and ₹4.51b worth of receivables due within a year. So it can boast ₹6.95b more liquid assets than total liabilities.

This short term liquidity is a sign that Marksans Pharma could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Marksans Pharma has more cash than debt is arguably a good indication that it can manage its debt safely.

In addition to that, we're happy to report that Marksans Pharma has boosted its EBIT by 57%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since Marksans Pharma will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. While Marksans Pharma has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Looking at the most recent three years, Marksans Pharma recorded free cash flow of 31% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Summing Up

While we empathize with investors who find debt concerning, you should keep in mind that Marksans Pharma has net cash of ₹6.26b, as well as more liquid assets than liabilities. And it impressed us with its EBIT growth of 57% over the last year. So we don't think Marksans Pharma's use of debt is risky. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. For example, we've discovered 2 warning signs for Marksans Pharma that you should be aware of before investing here.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MARKSANS

Marksans Pharma

Engages in the research, manufacturing, marketing, and sale of pharmaceutical formulations in the United States, North America, Europe, the United Kingdom, Australia, New Zealand, and internationally.

Very undervalued with excellent balance sheet.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|27.4% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|25.8% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|2.7% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.0% undervalued

RO

Community Contributor