Little Excitement Around Mangalam Drugs & Organics Limited's (NSE:MANGALAM) Revenues As Shares Take 25% Pounding

Mangalam Drugs & Organics Limited (NSE:MANGALAM) shares have had a horrible month, losing 25% after a relatively good period beforehand. Longer-term shareholders would now have taken a real hit with the stock declining 4.8% in the last year.

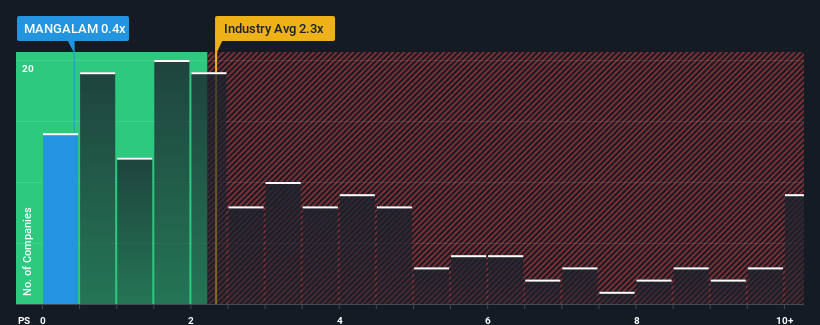

Since its price has dipped substantially, Mangalam Drugs & Organics may be sending buy signals at present with its price-to-sales (or "P/S") ratio of 0.4x, considering almost half of all companies in the Pharmaceuticals industry in India have P/S ratios greater than 2.3x and even P/S higher than 5x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's limited.

See our latest analysis for Mangalam Drugs & Organics

What Does Mangalam Drugs & Organics' P/S Mean For Shareholders?

As an illustration, revenue has deteriorated at Mangalam Drugs & Organics over the last year, which is not ideal at all. Perhaps the market believes the recent revenue performance isn't good enough to keep up the industry, causing the P/S ratio to suffer. However, if this doesn't eventuate then existing shareholders may be feeling optimistic about the future direction of the share price.

Want the full picture on earnings, revenue and cash flow for the company? Then our free report on Mangalam Drugs & Organics will help you shine a light on its historical performance.Is There Any Revenue Growth Forecasted For Mangalam Drugs & Organics?

The only time you'd be truly comfortable seeing a P/S as low as Mangalam Drugs & Organics' is when the company's growth is on track to lag the industry.

Taking a look back first, the company's revenue growth last year wasn't something to get excited about as it posted a disappointing decline of 13%. The last three years don't look nice either as the company has shrunk revenue by 4.8% in aggregate. So unfortunately, we have to acknowledge that the company has not done a great job of growing revenue over that time.

Comparing that to the industry, which is predicted to deliver 12% growth in the next 12 months, the company's downward momentum based on recent medium-term revenue results is a sobering picture.

In light of this, it's understandable that Mangalam Drugs & Organics' P/S would sit below the majority of other companies. Nonetheless, there's no guarantee the P/S has reached a floor yet with revenue going in reverse. There's potential for the P/S to fall to even lower levels if the company doesn't improve its top-line growth.

The Key Takeaway

Mangalam Drugs & Organics' recently weak share price has pulled its P/S back below other Pharmaceuticals companies. It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

As we suspected, our examination of Mangalam Drugs & Organics revealed its shrinking revenue over the medium-term is contributing to its low P/S, given the industry is set to grow. Right now shareholders are accepting the low P/S as they concede future revenue probably won't provide any pleasant surprises either. Unless the recent medium-term conditions improve, they will continue to form a barrier for the share price around these levels.

Having said that, be aware Mangalam Drugs & Organics is showing 3 warning signs in our investment analysis, and 1 of those makes us a bit uncomfortable.

If strong companies turning a profit tickle your fancy, then you'll want to check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:MANGALAM

Mangalam Drugs & Organics

Together with its subsidiary, manufactures and sells active pharmaceutical ingredients (APIs) and intermediates in India.

Acceptable track record with mediocre balance sheet.

Market Insights

Community Narratives