- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

UltraTech Cement's (NSE:ULTRACEMCO) Dividend Will Be Increased To ₹37.00

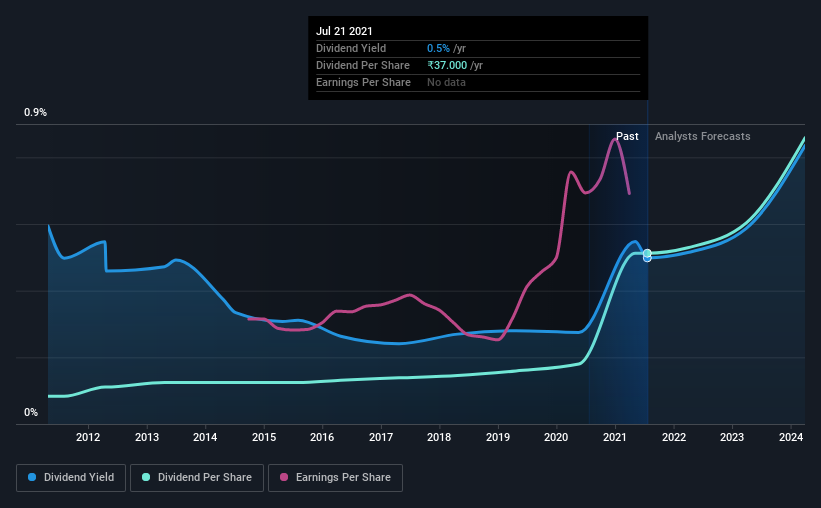

UltraTech Cement Limited (NSE:ULTRACEMCO) will increase its dividend on the 18th of October to ₹37.00. Even though the dividend went up, the yield is still quite low at only 0.5%.

View our latest analysis for UltraTech Cement

UltraTech Cement's Payment Has Solid Earnings Coverage

The dividend yield is a little bit low, but sustainability of the payments is also an important part of evaluating an income stock. However, UltraTech Cement's earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

The next year is set to see EPS grow by 21.3%. If the dividend continues along recent trends, we estimate the payout ratio will be 21%, which is in the range that makes us comfortable with the sustainability of the dividend.

UltraTech Cement Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2011, the dividend has gone from ₹6.00 to ₹37.00. This works out to be a compound annual growth rate (CAGR) of approximately 20% a year over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Looks Likely To Grow

Investors who have held shares in the company for the past few years will be happy with the dividend income they have received. UltraTech Cement has impressed us by growing EPS at 15% per year over the past five years. With a decent amount of growth and a low payout ratio, we think this bodes well for UltraTech Cement's prospects of growing its dividend payments in the future.

UltraTech Cement Looks Like A Great Dividend Stock

Overall, a dividend increase is always good, and we think that UltraTech Cement is a strong income stock thanks to its track record and growing earnings. The company is easily earning enough to cover its dividend payments and it is great to see that these earnings are being translated into cash flow. All of these factors considered, we think this has solid potential as a dividend stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For example, we've picked out 2 warning signs for UltraTech Cement that investors should know about before committing capital to this stock. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

If you decide to trade UltraTech Cement, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

If you're looking to trade UltraTech Cement, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:ULTRACEMCO

UltraTech Cement

Primarily engages in the manufacture and sale of clinker, cement, and related products in India.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Community Narratives