- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

UltraTech Cement Limited's (NSE:ULTRACEMCO) Stock Has Fared Decently: Is the Market Following Strong Financials?

Most readers would already know that UltraTech Cement's (NSE:ULTRACEMCO) stock increased by 3.3% over the past week. Since the market usually pay for a company’s long-term financial health, we decided to study the company’s fundamentals to see if they could be influencing the market. In this article, we decided to focus on UltraTech Cement's ROE.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it received from its shareholders. In short, ROE shows the profit each dollar generates with respect to its shareholder investments.

See our latest analysis for UltraTech Cement

How Is ROE Calculated?

The formula for ROE is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for UltraTech Cement is:

10% = ₹66b ÷ ₹628b (Based on the trailing twelve months to September 2024).

The 'return' refers to a company's earnings over the last year. So, this means that for every ₹1 of its shareholder's investments, the company generates a profit of ₹0.10.

Why Is ROE Important For Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

UltraTech Cement's Earnings Growth And 10% ROE

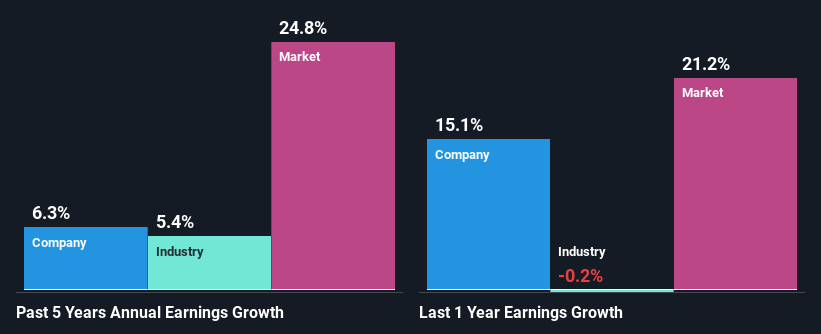

On the face of it, UltraTech Cement's ROE is not much to talk about. However, the fact that the company's ROE is higher than the average industry ROE of 6.5%, is definitely interesting. Consequently, this likely laid the ground for the decent growth of 6.3% seen over the past five years by UltraTech Cement. Bear in mind, the company does have a moderately low ROE. It is just that the industry ROE is lower. So there might well be other reasons for the earnings to grow. For example, it is possible that the broader industry is going through a high growth phase, or that the company has a low payout ratio.

Next, on comparing UltraTech Cement's net income growth with the industry, we found that the company's reported growth is similar to the industry average growth rate of 5.4% over the last few years.

Earnings growth is an important metric to consider when valuing a stock. It’s important for an investor to know whether the market has priced in the company's expected earnings growth (or decline). This then helps them determine if the stock is placed for a bright or bleak future. Is UltraTech Cement fairly valued compared to other companies? These 3 valuation measures might help you decide.

Is UltraTech Cement Making Efficient Use Of Its Profits?

In UltraTech Cement's case, its respectable earnings growth can probably be explained by its low three-year median payout ratio of 22% (or a retention ratio of 78%), which suggests that the company is investing most of its profits to grow its business.

Besides, UltraTech Cement has been paying dividends for at least ten years or more. This shows that the company is committed to sharing profits with its shareholders. Based on the latest analysts' estimates, we found that the company's future payout ratio over the next three years is expected to hold steady at 22%. Still, forecasts suggest that UltraTech Cement's future ROE will rise to 14% even though the the company's payout ratio is not expected to change by much.

Conclusion

In total, we are pretty happy with UltraTech Cement's performance. In particular, it's great to see that the company has seen significant growth in its earnings backed by a respectable ROE and a high reinvestment rate. That being so, the latest analyst forecasts show that the company will continue to see an expansion in its earnings. To know more about the company's future earnings growth forecasts take a look at this free report on analyst forecasts for the company to find out more.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ULTRACEMCO

UltraTech Cement

Primarily engages in the manufacture and sale of clinker, cement, and related products in India.

Solid track record with excellent balance sheet and pays a dividend.