Advertisement

- India

- /

- Basic Materials

- /

- NSEI:ULTRACEMCO

Should You Buy UltraTech Cement Limited (NSE:ULTRACEMCO) For Its Upcoming Dividend?

Readers hoping to buy UltraTech Cement Limited (NSE:ULTRACEMCO) for its dividend will need to make their move shortly, as the stock is about to trade ex-dividend. You will need to purchase shares before the 29th of July to receive the dividend, which will be paid on the 11th of September.

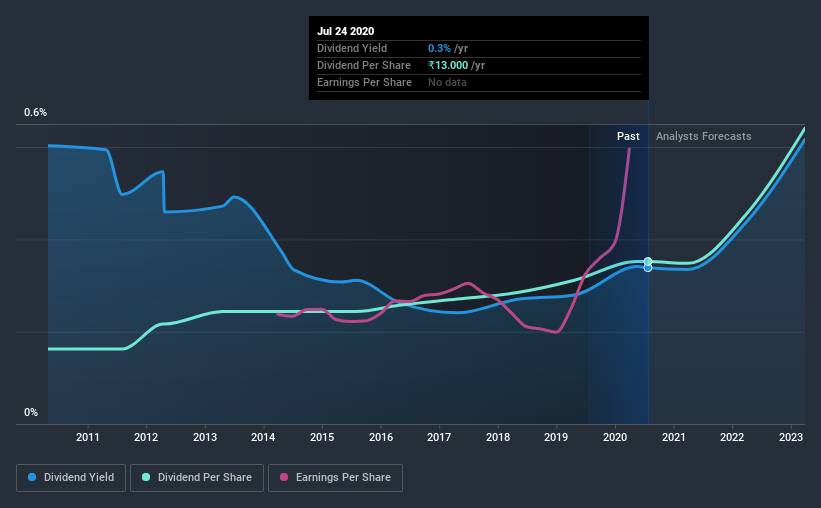

UltraTech Cement's next dividend payment will be ₹13.00 per share, and in the last 12 months, the company paid a total of ₹13.00 per share. Based on the last year's worth of payments, UltraTech Cement stock has a trailing yield of around 0.3% on the current share price of ₹3837.9. Dividends are a major contributor to investment returns for long term holders, but only if the dividend continues to be paid. So we need to investigate whether UltraTech Cement can afford its dividend, and if the dividend could grow.

Check out our latest analysis for UltraTech Cement

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. UltraTech Cement paid out just 6.4% of its profit last year, which we think is conservatively low and leaves plenty of margin for unexpected circumstances. That said, even highly profitable companies sometimes might not generate enough cash to pay the dividend, which is why we should always check if the dividend is covered by cash flow. Luckily it paid out just 4.4% of its free cash flow last year.

It's positive to see that UltraTech Cement's dividend is covered by both profits and cash flow, since this is generally a sign that the dividend is sustainable, and a lower payout ratio usually suggests a greater margin of safety before the dividend gets cut.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. If earnings fall far enough, the company could be forced to cut its dividend. That's why it's comforting to see UltraTech Cement's earnings have been skyrocketing, up 21% per annum for the past five years. UltraTech Cement looks like a real growth company, with earnings per share growing at a cracking pace and the company reinvesting most of its profits in the business.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the past 10 years, UltraTech Cement has increased its dividend at approximately 8.0% a year on average. We're glad to see dividends rising alongside earnings over a number of years, which may be a sign the company intends to share the growth with shareholders.

To Sum It Up

Has UltraTech Cement got what it takes to maintain its dividend payments? We love that UltraTech Cement is growing earnings per share while simultaneously paying out a low percentage of both its earnings and cash flow. These characteristics suggest the company is reinvesting in growing its business, while the conservative payout ratio also implies a reduced risk of the dividend being cut in the future. There's a lot to like about UltraTech Cement, and we would prioritise taking a closer look at it.

While it's tempting to invest in UltraTech Cement for the dividends alone, you should always be mindful of the risks involved. To that end, you should learn about the 3 warning signs we've spotted with UltraTech Cement (including 1 which makes us a bit uncomfortable).

If you're in the market for dividend stocks, we recommend checking our list of top dividend stocks with a greater than 2% yield and an upcoming dividend.

If you’re looking to trade UltraTech Cement, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:ULTRACEMCO

UltraTech Cement

Primarily engages in the manufacture and sale of clinker, cement, and related products in India.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

WhiteCap Is Positioned To Profit Regardless Of Trump's Policy

Fair Value CA$22.60|61.7% undervalued

ST

Equity Analyst and Writer

Microsoft's Evolution Will Drive Revenue to New Heights Fueled by AI

Fair Value US$360.00|28.9% overvalued

BR

Community Contributor

A CASE FOR USD$2.50 (CAD$3.44) BY 2028 (A 5-10 BAGGER)

Fair Value CA$3.44|88.1% undervalued

AG

Community Contributor