Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:TATASTEEL

If EPS Growth Is Important To You, Tata Steel (NSE:TATASTEEL) Presents An Opportunity

For beginners, it can seem like a good idea (and an exciting prospect) to buy a company that tells a good story to investors, even if it currently lacks a track record of revenue and profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' While a well funded company may sustain losses for years, it will need to generate a profit eventually, or else investors will move on and the company will wither away.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Tata Steel (NSE:TATASTEEL). Even if this company is fairly valued by the market, investors would agree that generating consistent profits will continue to provide Tata Steel with the means to add long-term value to shareholders.

See our latest analysis for Tata Steel

How Quickly Is Tata Steel Increasing Earnings Per Share?

If a company can keep growing earnings per share (EPS) long enough, its share price should eventually follow. That makes EPS growth an attractive quality for any company. Tata Steel's shareholders have have plenty to be happy about as their annual EPS growth for the last 3 years was 55%. Growth that fast may well be fleeting, but it should be more than enough to pique the interest of the wary stock pickers.

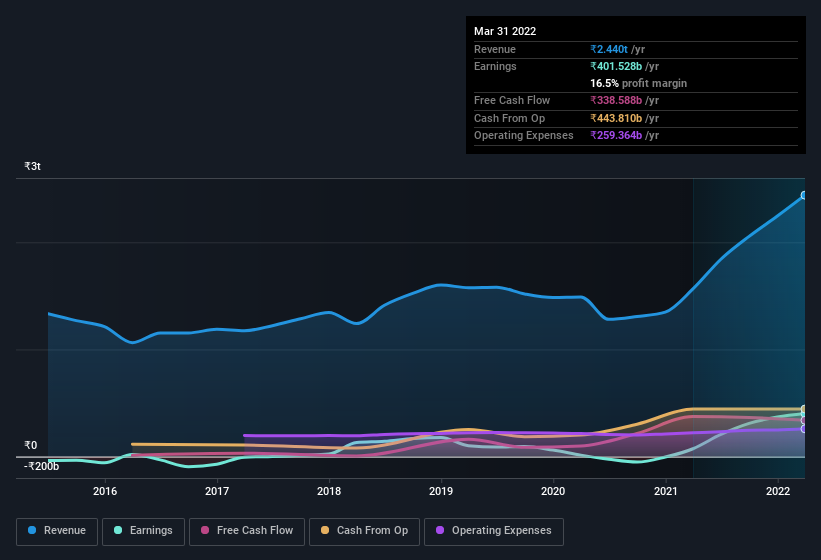

Top-line growth is a great indicator that growth is sustainable, and combined with a high earnings before interest and taxation (EBIT) margin, it's a great way for a company to maintain a competitive advantage in the market. Tata Steel shareholders can take confidence from the fact that EBIT margins are up from 12% to 23%, and revenue is growing. Ticking those two boxes is a good sign of growth, in our book.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

In investing, as in life, the future matters more than the past. So why not check out this free interactive visualization of Tata Steel's forecast profits?

Are Tata Steel Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, insiders are sometimes wrong, and we don't know the exact thinking behind their acquisitions.

While some insiders did sell some of their holdings in Tata Steel, one lone insider trumped that with significant stock purchases. Specifically the Additional Non-Executive Independent Director, Farida Khambata, spent ₹22m, paying about ₹1,098 per share. That certainly piques our interest.

Should You Add Tata Steel To Your Watchlist?

Tata Steel's earnings have taken off in quite an impressive fashion. Growth investors should find it difficult to look past that strong EPS move. And indeed, it could be a sign that the business is at an inflection point. If this these factors intrigue you, then an addition of Tata Steel to your watchlist won't go amiss. It is worth noting though that we have found 3 warning signs for Tata Steel (1 is a bit concerning!) that you need to take into consideration.

Keen growth investors love to see insider buying. Thankfully, Tata Steel isn't the only one. You can see a a free list of them here.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

Valuation is complex, but we're here to simplify it.

Discover if Tata Steel might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:TATASTEEL

Tata Steel

Engages in the manufacture and distribution of steel products in India and internationally.

Moderate growth potential second-rate dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Nike's Direct-to-Consumer Focus Will Drive Future Growth

Fair Value US$87.90|22.7% undervalued

UN

Community Contributor

Novo Nordisk will dominate GLP-1 market with Ozempic and Wegovy growth

Fair Value US$89.59|14.2% undervalued

BE

Community Contributor

Rheinmetall could get 20-25% of EU-NATO 3%-GDP defence spending

Fair Value €7.57k|82.8% undervalued

NO

Community Contributor