Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:SURANI

We Think Surani Steel Tubes (NSE:SURANI) Has A Fair Chunk Of Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We can see that Surani Steel Tubes Limited (NSE:SURANI) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Surani Steel Tubes

What Is Surani Steel Tubes's Net Debt?

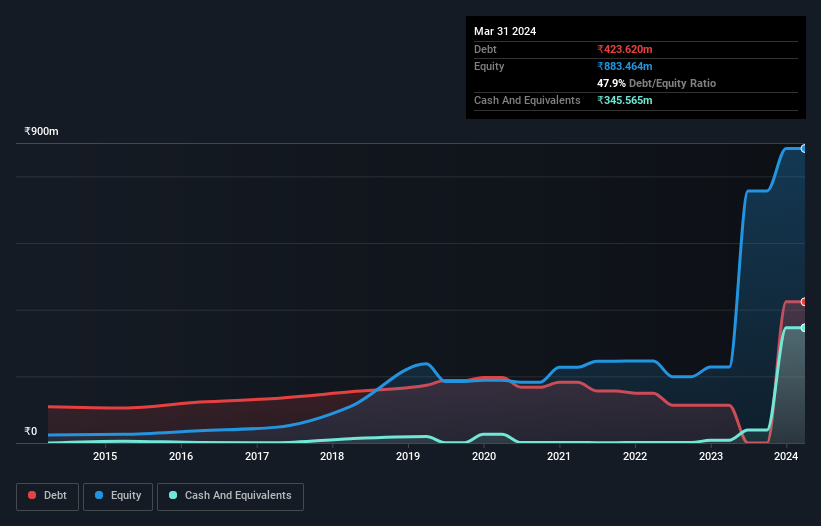

As you can see below, at the end of March 2024, Surani Steel Tubes had ₹423.6m of debt, up from ₹113.3m a year ago. Click the image for more detail. On the flip side, it has ₹345.6m in cash leading to net debt of about ₹78.1m.

A Look At Surani Steel Tubes' Liabilities

Zooming in on the latest balance sheet data, we can see that Surani Steel Tubes had liabilities of ₹453.3m due within 12 months and liabilities of ₹5.41m due beyond that. Offsetting this, it had ₹345.6m in cash and ₹113.1m in receivables that were due within 12 months. So these liquid assets roughly match the total liabilities.

Having regard to Surani Steel Tubes' size, it seems that its liquid assets are well balanced with its total liabilities. So it's very unlikely that the ₹2.87b company is short on cash, but still worth keeping an eye on the balance sheet. There's no doubt that we learn most about debt from the balance sheet. But it is Surani Steel Tubes's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Over 12 months, Surani Steel Tubes reported revenue of ₹1.6b, which is a gain of 26%, although it did not report any earnings before interest and tax. With any luck the company will be able to grow its way to profitability.

Caveat Emptor

While we can certainly appreciate Surani Steel Tubes's revenue growth, its earnings before interest and tax (EBIT) loss is not ideal. To be specific the EBIT loss came in at ₹799k. Looking on the brighter side, the business has adequate liquid assets, which give it time to grow and develop before its debt becomes a near-term issue. But we'd want to see some positive free cashflow before spending much time on trying to understand the stock. This one is a bit too risky for our liking. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. For example Surani Steel Tubes has 2 warning signs (and 1 which can't be ignored) we think you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:SURANI

Surani Steel Tubes

Engages in the manufacture and supply of ERW mild steel (MS) pipes and steel tubes in India.

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|26.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.8% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor