- India

- /

- Metals and Mining

- /

- NSEI:SANDUMA

Optimistic Investors Push The Sandur Manganese & Iron Ores Limited (NSE:SANDUMA) Shares Up 26% But Growth Is Lacking

Despite an already strong run, The Sandur Manganese & Iron Ores Limited (NSE:SANDUMA) shares have been powering on, with a gain of 26% in the last thirty days. While recent buyers may be laughing, long-term holders might not be as pleased since the recent gain only brings the stock back to where it started a year ago.

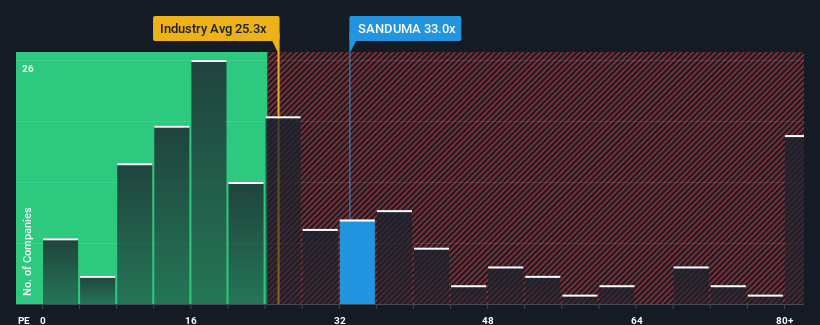

In spite of the firm bounce in price, it's still not a stretch to say that Sandur Manganese & Iron Ores' price-to-earnings (or "P/E") ratio of 33x right now seems quite "middle-of-the-road" compared to the market in India, where the median P/E ratio is around 32x. Although, it's not wise to simply ignore the P/E without explanation as investors may be disregarding a distinct opportunity or a costly mistake.

As an illustration, earnings have deteriorated at Sandur Manganese & Iron Ores over the last year, which is not ideal at all. It might be that many expect the company to put the disappointing earnings performance behind them over the coming period, which has kept the P/E from falling. If you like the company, you'd at least be hoping this is the case so that you could potentially pick up some stock while it's not quite in favour.

View our latest analysis for Sandur Manganese & Iron Ores

How Is Sandur Manganese & Iron Ores' Growth Trending?

There's an inherent assumption that a company should be matching the market for P/E ratios like Sandur Manganese & Iron Ores' to be considered reasonable.

If we review the last year of earnings, dishearteningly the company's profits fell to the tune of 54%. As a result, earnings from three years ago have also fallen 27% overall. Accordingly, shareholders would have felt downbeat about the medium-term rates of earnings growth.

In contrast to the company, the rest of the market is expected to grow by 25% over the next year, which really puts the company's recent medium-term earnings decline into perspective.

With this information, we find it concerning that Sandur Manganese & Iron Ores is trading at a fairly similar P/E to the market. Apparently many investors in the company are way less bearish than recent times would indicate and aren't willing to let go of their stock right now. Only the boldest would assume these prices are sustainable as a continuation of recent earnings trends is likely to weigh on the share price eventually.

What We Can Learn From Sandur Manganese & Iron Ores' P/E?

Sandur Manganese & Iron Ores appears to be back in favour with a solid price jump getting its P/E back in line with most other companies. While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

Our examination of Sandur Manganese & Iron Ores revealed its shrinking earnings over the medium-term aren't impacting its P/E as much as we would have predicted, given the market is set to grow. Right now we are uncomfortable with the P/E as this earnings performance is unlikely to support a more positive sentiment for long. Unless the recent medium-term conditions improve, it's challenging to accept these prices as being reasonable.

Before you take the next step, you should know about the 1 warning sign for Sandur Manganese & Iron Ores that we have uncovered.

Of course, you might also be able to find a better stock than Sandur Manganese & Iron Ores. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SANDUMA

Sandur Manganese & Iron Ores

Together with its subsidiary, engages in the mining of manganese and iron ores in Deogiri village of Ballari District, Karnataka.

Outstanding track record with flawless balance sheet.

Market Insights

Community Narratives