Advertisement

One Analyst Just Shaved Their Rossari Biotech Limited (NSE:ROSSARI) Forecasts Dramatically

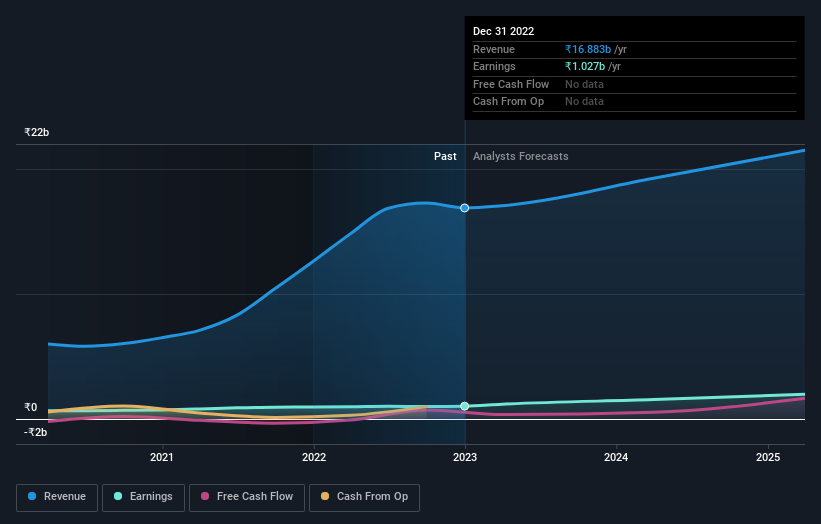

The analyst covering Rossari Biotech Limited (NSE:ROSSARI) delivered a dose of negativity to shareholders today, by making a substantial revision to their statutory forecasts for next year. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business.

Following the downgrade, the current consensus from Rossari Biotech's one analyst is for revenues of ₹19b in 2024 which - if met - would reflect a solid 14% increase on its sales over the past 12 months. Statutory earnings per share are presumed to surge 52% to ₹28.20. Previously, the analyst had been modelling revenues of ₹23b and earnings per share (EPS) of ₹39.12 in 2024. Indeed, we can see that the analyst is a lot more bearish about Rossari Biotech's prospects, administering a measurable cut to revenue estimates and slashing their EPS estimates to boot.

View our latest analysis for Rossari Biotech

The consensus price target fell 7.1% to ₹986, with the weaker earnings outlook clearly leading analyst valuation estimates. There's another way to think about price targets though, and that's to look at the range of price targets put forward by analysts, because a wide range of estimates could suggest a diverse view on possible outcomes for the business. There are some variant perceptions on Rossari Biotech, with the most bullish analyst valuing it at ₹1,252 and the most bearish at ₹720 per share. This shows there is still some diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. It's pretty clear that there is an expectation that Rossari Biotech's revenue growth will slow down substantially, with revenues to the end of 2024 expected to display 11% growth on an annualised basis. This is compared to a historical growth rate of 34% over the past five years. Compare this to the 296 other companies in this industry with analyst coverage, which are forecast to grow their revenue at 12% per year. So it's pretty clear that, while Rossari Biotech's revenue growth is expected to slow, it's expected to grow roughly in line with the industry.

The Bottom Line

The most important thing to take away is that the analyst cut their earnings per share estimates, expecting a clear decline in business conditions. Lamentably, they also downgraded their sales forecasts, but the business is still expected to grow at roughly the same rate as the market itself. Given the scope of the downgrades, it would not be a surprise to see the market become more wary of the business.

Even so, the longer term trajectory of the business is much more important for the value creation of shareholders. We have analyst estimates for Rossari Biotech going out as far as 2025, and you can see them free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ROSSARI

Rossari Biotech

Engages in manufacturing and selling specialty chemicals in India and internationally.

Flawless balance sheet with reasonable growth potential.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor