- India

- /

- Basic Materials

- /

- NSEI:RHIM

We Think Orient Refractories (NSE:ORIENTREF) Can Manage Its Debt With Ease

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We can see that Orient Refractories Limited (NSE:ORIENTREF) does use debt in its business. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Orient Refractories

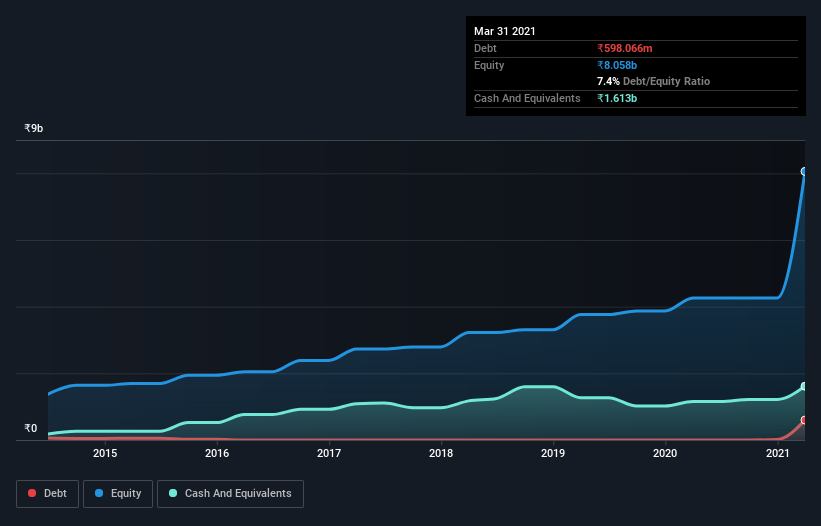

What Is Orient Refractories's Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2021 Orient Refractories had ₹598.1m of debt, an increase on none, over one year. However, it does have ₹1.61b in cash offsetting this, leading to net cash of ₹1.02b.

How Healthy Is Orient Refractories' Balance Sheet?

We can see from the most recent balance sheet that Orient Refractories had liabilities of ₹3.91b falling due within a year, and liabilities of ₹626.8m due beyond that. Offsetting these obligations, it had cash of ₹1.61b as well as receivables valued at ₹3.89b due within 12 months. So it actually has ₹964.6m more liquid assets than total liabilities.

This state of affairs indicates that Orient Refractories' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the ₹51.4b company is short on cash, but still worth keeping an eye on the balance sheet. Succinctly put, Orient Refractories boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that Orient Refractories has boosted its EBIT by 61%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Orient Refractories can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Orient Refractories may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last three years, Orient Refractories's free cash flow amounted to 33% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Summing up

While we empathize with investors who find debt concerning, you should keep in mind that Orient Refractories has net cash of ₹1.02b, as well as more liquid assets than liabilities. And it impressed us with its EBIT growth of 61% over the last year. So we don't think Orient Refractories's use of debt is risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Orient Refractories that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

If you decide to trade Orient Refractories, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:RHIM

RHI Magnesita India

Engages in the manufacture and trading of in refractories, monolithics, bricks, and ceramic paper in India and internationally.

Excellent balance sheet average dividend payer.

Market Insights

Community Narratives