Nahar Poly Films' (NSE:NAHARPOLY) five-year earnings growth trails the incredible shareholder returns

Nahar Poly Films Limited (NSE:NAHARPOLY) shareholders might be concerned after seeing the share price drop 19% in the last quarter. But that doesn't change the fact that the returns over the last half decade have been spectacular. In fact, during that period, the share price climbed 637%. Impressive! So we don't think the recent decline in the share price means its story is a sad one. The most important thing for savvy investors to consider is whether the underlying business can justify the share price gain. Unfortunately not all shareholders will have held it for five years, so spare a thought for those caught in the 59% decline over the last three years: that's a long time to wait for profits. We love happy stories like this one. The company should be really proud of that performance!

The past week has proven to be lucrative for Nahar Poly Films investors, so let's see if fundamentals drove the company's five-year performance.

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Over half a decade, Nahar Poly Films managed to grow its earnings per share at 0.2% a year. This EPS growth is lower than the 49% average annual increase in the share price. So it's fair to assume the market has a higher opinion of the business than it did five years ago. That's not necessarily surprising considering the five-year track record of earnings growth.

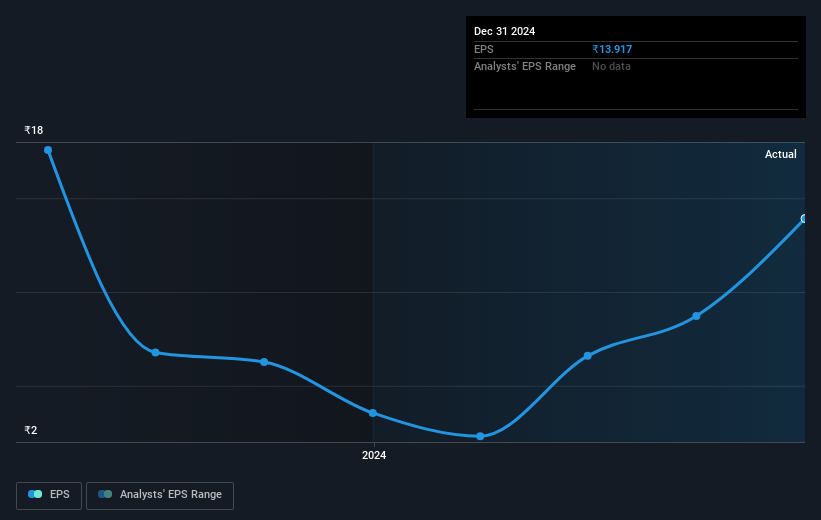

The image below shows how EPS has tracked over time (if you click on the image you can see greater detail).

This free interactive report on Nahar Poly Films' earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

What About Dividends?

As well as measuring the share price return, investors should also consider the total shareholder return (TSR). Whereas the share price return only reflects the change in the share price, the TSR includes the value of dividends (assuming they were reinvested) and the benefit of any discounted capital raising or spin-off. So for companies that pay a generous dividend, the TSR is often a lot higher than the share price return. We note that for Nahar Poly Films the TSR over the last 5 years was 666%, which is better than the share price return mentioned above. The dividends paid by the company have thusly boosted the total shareholder return.

A Different Perspective

It's good to see that Nahar Poly Films has rewarded shareholders with a total shareholder return of 8.5% in the last twelve months. And that does include the dividend. Having said that, the five-year TSR of 50% a year, is even better. Potential buyers might understandably feel they've missed the opportunity, but it's always possible business is still firing on all cylinders. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. For instance, we've identified 3 warning signs for Nahar Poly Films (1 shouldn't be ignored) that you should be aware of.

But note: Nahar Poly Films may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Indian exchanges.

If you're looking to trade Nahar Poly Films, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if Nahar Poly Films might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NAHARPOLY

Nahar Poly Films

Manufactures and sells bi-axially oriented polypropylene films in India and internationally.

Excellent balance sheet and good value.

Market Insights

Community Narratives