Advertisement

Laxmi Organic Industries Limited (NSE:LXCHEM) Just Released Its Yearly Earnings: Here's What Analysts Think

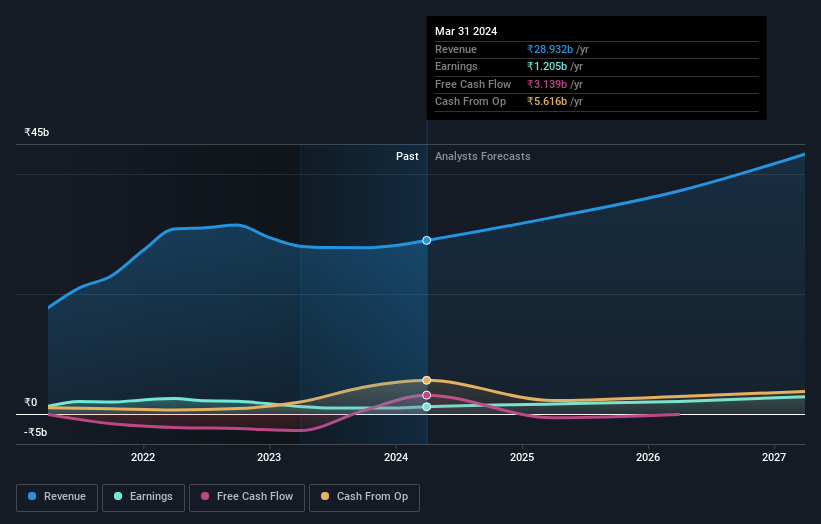

Last week saw the newest full-year earnings release from Laxmi Organic Industries Limited (NSE:LXCHEM), an important milestone in the company's journey to build a stronger business. Results overall were respectable, with statutory earnings of ₹4.43 per share roughly in line with what the analysts had forecast. Revenues of ₹29b came in 3.1% ahead of analyst predictions. Following the result, the analysts have updated their earnings model, and it would be good to know whether they think there's been a strong change in the company's prospects, or if it's business as usual. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

Check out our latest analysis for Laxmi Organic Industries

Taking into account the latest results, the most recent consensus for Laxmi Organic Industries from four analysts is for revenues of ₹32.8b in 2025. If met, it would imply a meaningful 13% increase on its revenue over the past 12 months. Statutory earnings per share are predicted to surge 40% to ₹6.15. Yet prior to the latest earnings, the analysts had been anticipated revenues of ₹32.2b and earnings per share (EPS) of ₹6.25 in 2025. The consensus analysts don't seem to have seen anything in these results that would have changed their view on the business, given there's been no major change to their estimates.

The analysts reconfirmed their price target of ₹247, showing that the business is executing well and in line with expectations. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. The most optimistic Laxmi Organic Industries analyst has a price target of ₹272 per share, while the most pessimistic values it at ₹206. Even so, with a relatively close grouping of estimates, it looks like the analysts are quite confident in their valuations, suggesting Laxmi Organic Industries is an easy business to forecast or the the analysts are all using similar assumptions.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 13% growth on an annualised basis. That is in line with its 13% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 12% annually. So although Laxmi Organic Industries is expected to maintain its revenue growth rate, it's only growing at about the rate of the wider industry.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Happily, there were no real changes to revenue forecasts, with the business still expected to grow in line with the overall industry. There was no real change to the consensus price target, suggesting that the intrinsic value of the business has not undergone any major changes with the latest estimates.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Laxmi Organic Industries going out to 2027, and you can see them free on our platform here..

Don't forget that there may still be risks. For instance, we've identified 1 warning sign for Laxmi Organic Industries that you should be aware of.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:LXCHEM

Laxmi Organic Industries

Manufactures and trades acetyl intermediates and specialty chemicals in India and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.3% undervalued

9 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

27 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Pagaya Technologies ·

The "Rate Cut" Supercycle Winner – Profitable & Accelerating

Fair Value:US$170.685.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Archer Aviation ·

The Industrialist of the Skies – Scaling with "Automotive DNA

Fair Value:US$16.3254.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

110 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

943 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

145 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative