Advertisement

- India

- /

- Metals and Mining

- /

- NSEI:KIRLOSIND

Kirloskar Industries (NSE:KIRLOSIND) Shareholders Will Want The ROCE Trajectory To Continue

If you're looking for a multi-bagger, there's a few things to keep an eye out for. Amongst other things, we'll want to see two things; firstly, a growing return on capital employed (ROCE) and secondly, an expansion in the company's amount of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So on that note, Kirloskar Industries (NSE:KIRLOSIND) looks quite promising in regards to its trends of return on capital.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. The formula for this calculation on Kirloskar Industries is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.16 = ₹4.1b ÷ (₹32b - ₹6.6b) (Based on the trailing twelve months to March 2021).

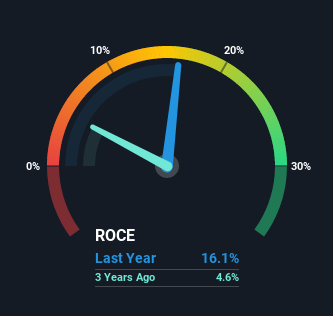

So, Kirloskar Industries has an ROCE of 16%. In absolute terms, that's a satisfactory return, but compared to the Metals and Mining industry average of 12% it's much better.

View our latest analysis for Kirloskar Industries

Historical performance is a great place to start when researching a stock so above you can see the gauge for Kirloskar Industries' ROCE against it's prior returns. If you want to delve into the historical earnings, revenue and cash flow of Kirloskar Industries, check out these free graphs here.

So How Is Kirloskar Industries' ROCE Trending?

Kirloskar Industries is displaying some positive trends. Over the last five years, returns on capital employed have risen substantially to 16%. The amount of capital employed has increased too, by 121%. The increasing returns on a growing amount of capital is common amongst multi-baggers and that's why we're impressed.

Our Take On Kirloskar Industries' ROCE

A company that is growing its returns on capital and can consistently reinvest in itself is a highly sought after trait, and that's what Kirloskar Industries has. And with the stock having performed exceptionally well over the last five years, these patterns are being accounted for by investors. In light of that, we think it's worth looking further into this stock because if Kirloskar Industries can keep these trends up, it could have a bright future ahead.

Kirloskar Industries does have some risks though, and we've spotted 1 warning sign for Kirloskar Industries that you might be interested in.

While Kirloskar Industries may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

When trading Kirloskar Industries or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Kirloskar Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:KIRLOSIND

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

America Wants Homegrown Drones — Draganfly Is Ready to Deliver

Fair Value US$9.21|33.8% undervalued

JO

Community Contributor

Cheesecake Factory offers an enticing opportunity for long-term growth by leveraging new concepts

Fair Value US$73.83|26.3% undervalued

ZW

Community Contributor

Coca-Cola’s Intrinsic Value Set to Rise with Fed Rate Cut

Fair Value US$67.50|1.2% undervalued

AL

Community Contributor

Fully Permitted Gold Mine with 50 Baggers Potential

Fair Value CA$41.00|98.6% undervalued

RO

Community Contributor