Advertisement

- India

- /

- Basic Materials

- /

- NSEI:KCP

The KCP Limited's (NSE:KCP) CEO Compensation Looks Acceptable To Us And Here's Why

Key Insights

- KCP's Annual General Meeting to take place on 11th of August

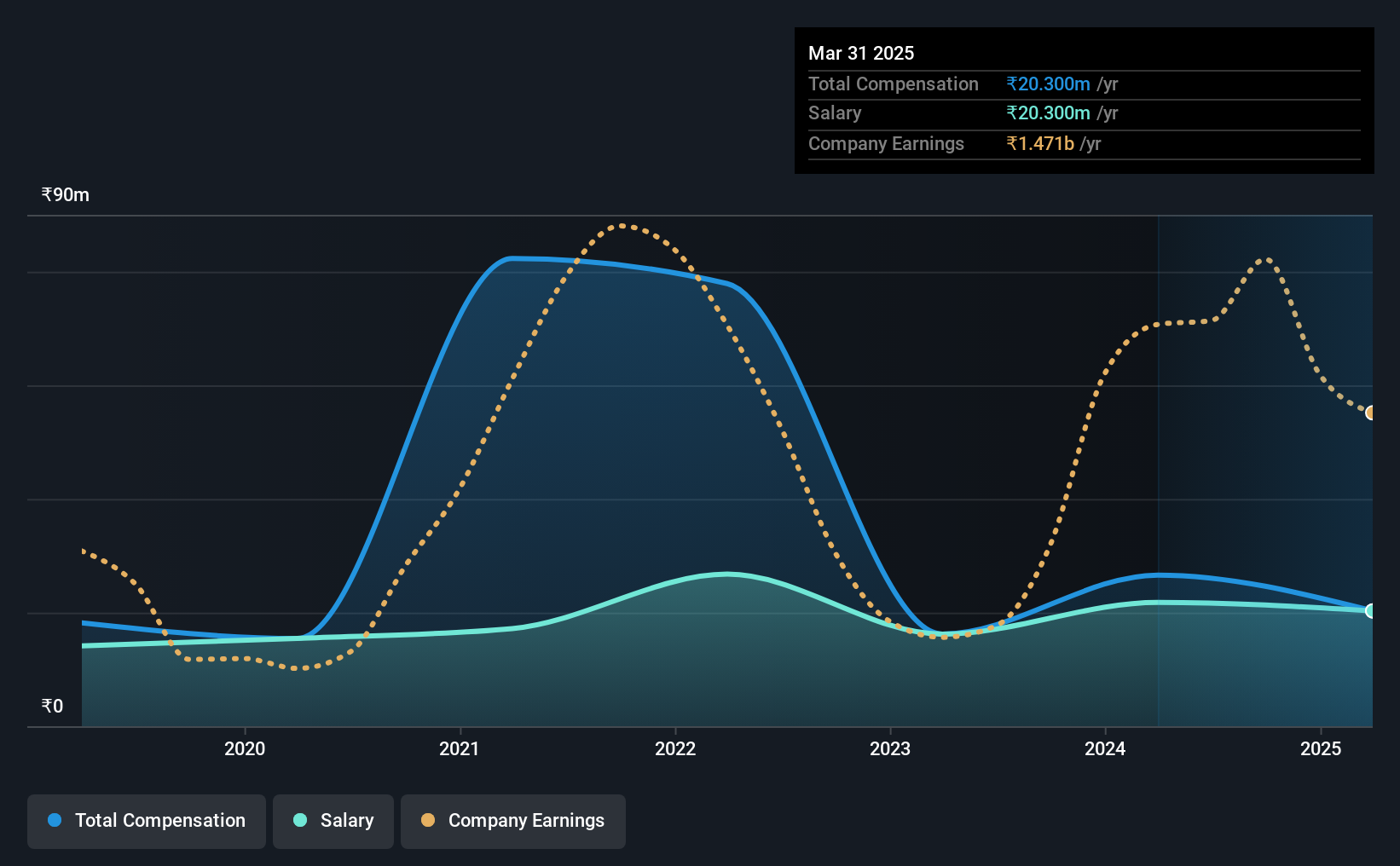

- Total pay for CEO Velagapudi Lakshmana Dutt includes ₹20.3m salary

- The total compensation is 49% less than the average for the industry

- KCP's EPS declined by 7.9% over the past three years while total shareholder return over the past three years was 86%

The performance at The KCP Limited (NSE:KCP) has been rather lacklustre of late and shareholders may be wondering what CEO Velagapudi Lakshmana Dutt is planning to do about this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 11th of August. Voting on executive pay could be a powerful way to influence management, as studies have shown that the right compensation incentives impact company performance. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

Check out our latest analysis for KCP

How Does Total Compensation For Velagapudi Lakshmana Dutt Compare With Other Companies In The Industry?

Our data indicates that The KCP Limited has a market capitalization of ₹26b, and total annual CEO compensation was reported as ₹20m for the year to March 2025. That's a notable decrease of 24% on last year. Notably, the salary of ₹20m is the entirety of the CEO compensation.

For comparison, other companies in the Indian Basic Materials industry with market capitalizations ranging between ₹8.7b and ₹35b had a median total CEO compensation of ₹40m. This suggests that Velagapudi Lakshmana Dutt is paid below the industry median. What's more, Velagapudi Lakshmana Dutt holds ₹2.4b worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2025 | 2024 | Proportion (2025) |

| Salary | ₹20m | ₹22m | 100% |

| Other | - | ₹4.8m | - |

| Total Compensation | ₹20m | ₹27m | 100% |

Speaking on an industry level, nearly 87% of total compensation represents salary, while the remainder of 13% is other remuneration. On a company level, KCP prefers to reward its CEO through a salary, opting not to pay Velagapudi Lakshmana Dutt through non-salary benefits. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

The KCP Limited's Growth

Over the last three years, The KCP Limited has shrunk its earnings per share by 7.9% per year. It saw its revenue drop 11% over the last year.

Few shareholders would be pleased to read that EPS have declined. This is compounded by the fact revenue is actually down on last year. These factors suggest that the business performance wouldn't really justify a high pay packet for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has The KCP Limited Been A Good Investment?

Most shareholders would probably be pleased with The KCP Limited for providing a total return of 86% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

KCP pays CEO compensation exclusively through a salary, with non-salary compensation completely ignored. While the return to shareholders does look promising, it's hard to ignore the lack of earnings growth and this makes us wonder if these strong returns can continue. These concerns could be addressed to the board and shareholders should revisit their investment thesis to see if it still makes sense.

So you may want to check if insiders are buying KCP shares with their own money (free access).

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if KCP might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:KCP

KCP

Engages in cement, heavy engineering, power generation, and hospitality businesses in India.

Flawless balance sheet with acceptable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.7% undervalued

TR

Community Contributor