Advertisement

Kansai Nerolac Paints Limited (NSE:KANSAINER) Looks Inexpensive But Perhaps Not Attractive Enough

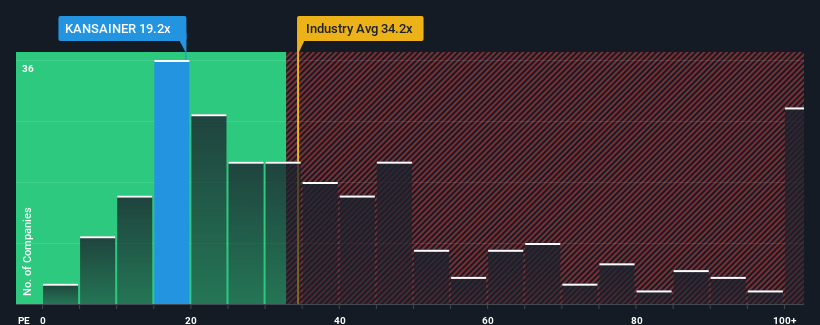

Kansai Nerolac Paints Limited's (NSE:KANSAINER) price-to-earnings (or "P/E") ratio of 19.2x might make it look like a buy right now compared to the market in India, where around half of the companies have P/E ratios above 35x and even P/E's above 67x are quite common. However, the P/E might be low for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, Kansai Nerolac Paints has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If not, then existing shareholders have reason to be quite optimistic about the future direction of the share price.

See our latest analysis for Kansai Nerolac Paints

Does Growth Match The Low P/E?

The only time you'd be truly comfortable seeing a P/E as low as Kansai Nerolac Paints' is when the company's growth is on track to lag the market.

Retrospectively, the last year delivered an exceptional 150% gain to the company's bottom line. Pleasingly, EPS has also lifted 124% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Shifting to the future, estimates from the six analysts covering the company suggest earnings growth is heading into negative territory, declining 8.9% per annum over the next three years. That's not great when the rest of the market is expected to grow by 21% per year.

With this information, we are not surprised that Kansai Nerolac Paints is trading at a P/E lower than the market. However, shrinking earnings are unlikely to lead to a stable P/E over the longer term. There's potential for the P/E to fall to even lower levels if the company doesn't improve its profitability.

What We Can Learn From Kansai Nerolac Paints' P/E?

While the price-to-earnings ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of earnings expectations.

We've established that Kansai Nerolac Paints maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. It's hard to see the share price rising strongly in the near future under these circumstances.

There are also other vital risk factors to consider and we've discovered 3 warning signs for Kansai Nerolac Paints (1 is a bit concerning!) that you should be aware of before investing here.

You might be able to find a better investment than Kansai Nerolac Paints. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if Kansai Nerolac Paints might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:KANSAINER

Kansai Nerolac Paints

Manufactures and supplies paints and varnishes, enamels, and lacquers in India.

Flawless balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Scaling up in building materials with smart M&A and growing profitability

Fair Value US$2.77|30.0% undervalued

CM

Community Contributor

Hims: The Platform Powering Personalised Healthcare

Fair Value US$114.01|51.9% undervalued

BL

Community Contributor

Undervalued lottery company with strong fundamentals

Fair Value AU$15.00|34.5% undervalued

RO

Community Contributor

Proximus, transferring money from the impatient to the patient investor

Fair Value €16.62|55.1% undervalued

AX

Community Contributor