Advertisement

- India

- /

- Basic Materials

- /

- NSEI:HEIDELBERG

HeidelbergCement India (NSE:HEIDELBERG) Is Increasing Its Dividend To ₹8.00

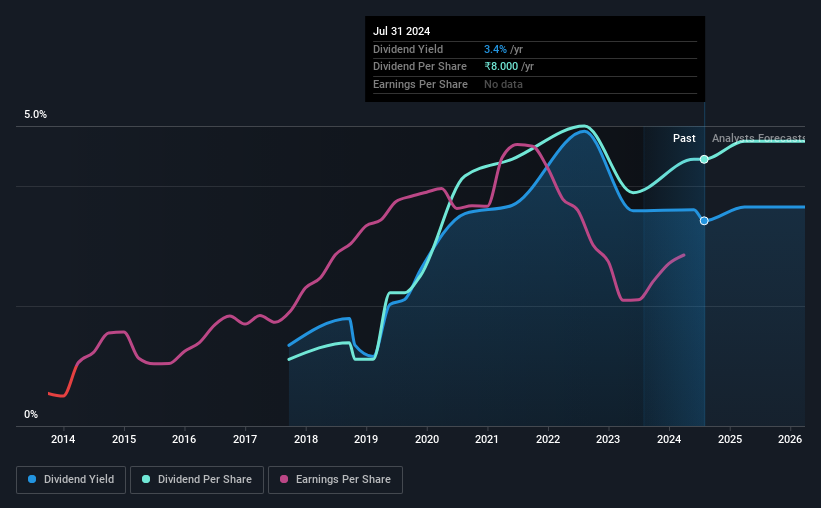

The board of HeidelbergCement India Limited (NSE:HEIDELBERG) has announced that it will be paying its dividend of ₹8.00 on the 25th of October, an increased payment from last year's comparable dividend. This will take the annual payment to 3.4% of the stock price, which is above what most companies in the industry pay.

See our latest analysis for HeidelbergCement India

HeidelbergCement India's Earnings Easily Cover The Distributions

While it is great to have a strong dividend yield, we should also consider whether the payment is sustainable. Based on the last payment, HeidelbergCement India's profits didn't cover the dividend, but the company was generating enough cash instead. Healthy cash flows are always a positive sign, especially when they quite easily cover the dividend.

Looking forward, earnings per share is forecast to rise by 90.8% over the next year. Assuming the dividend continues along the course it has been charting recently, our estimates show the payout ratio being 66% which brings it into quite a comfortable range.

HeidelbergCement India's Dividend Has Lacked Consistency

Looking back, HeidelbergCement India's dividend hasn't been particularly consistent. This suggests that the dividend might not be the most reliable. Since 2017, the dividend has gone from ₹2.00 total annually to ₹8.00. This works out to be a compound annual growth rate (CAGR) of approximately 22% a year over that time. Despite the rapid growth in the dividend over the past number of years, we have seen the payments go down the past as well, so that makes us cautious.

Dividend Growth Is Doubtful

With a relatively unstable dividend, it's even more important to see if earnings per share is growing. In the last five years, HeidelbergCement India's earnings per share has shrunk at approximately 5.3% per annum. If earnings continue declining, the company may have to make the difficult choice of reducing the dividend or even stopping it completely - the opposite of dividend growth. Earnings are predicted to grow over the next year, but we would remain cautious until a track record of earnings growth is established.

The Dividend Could Prove To Be Unreliable

In summary, while it's always good to see the dividend being raised, we don't think HeidelbergCement India's payments are rock solid. The payments haven't been particularly stable and we don't see huge growth potential, but with the dividend well covered by cash flows it could prove to be reliable over the short term. We don't think HeidelbergCement India is a great stock to add to your portfolio if income is your focus.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. For instance, we've picked out 1 warning sign for HeidelbergCement India that investors should take into consideration. Is HeidelbergCement India not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if HeidelbergCement India might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:HEIDELBERG

HeidelbergCement India

Engages in the manufacture and sale of cement in India.

Flawless balance sheet with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor