What Do The Returns On Capital At Camlin Fine Sciences (NSE:CAMLINFINE) Tell Us?

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. Typically, we'll want to notice a trend of growing return on capital employed (ROCE) and alongside that, an expanding base of capital employed. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. However, after briefly looking over the numbers, we don't think Camlin Fine Sciences (NSE:CAMLINFINE) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

What is Return On Capital Employed (ROCE)?

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. To calculate this metric for Camlin Fine Sciences, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

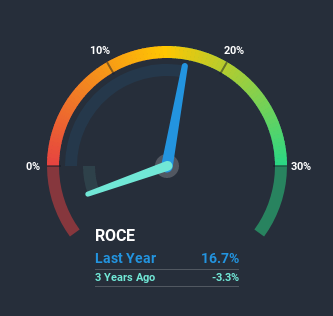

0.17 = ₹1.1b ÷ (₹12b - ₹5.5b) (Based on the trailing twelve months to June 2020).

Thus, Camlin Fine Sciences has an ROCE of 17%. On its own, that's a standard return, however it's much better than the 13% generated by the Chemicals industry.

View our latest analysis for Camlin Fine Sciences

Above you can see how the current ROCE for Camlin Fine Sciences compares to its prior returns on capital, but there's only so much you can tell from the past. If you'd like, you can check out the forecasts from the analysts covering Camlin Fine Sciences here for free.

What The Trend Of ROCE Can Tell Us

On the surface, the trend of ROCE at Camlin Fine Sciences doesn't inspire confidence. To be more specific, ROCE has fallen from 51% over the last five years. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. If these investments prove successful, this can bode very well for long term stock performance.

On a side note, Camlin Fine Sciences has done well to pay down its current liabilities to 44% of total assets. So we could link some of this to the decrease in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE. Keep in mind 44% is still pretty high, so those risks are still somewhat prevalent.The Bottom Line

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for Camlin Fine Sciences. These trends don't appear to have influenced returns though, because the total return from the stock has been mostly flat over the last five years. As a result, we'd recommend researching this stock further to uncover what other fundamentals of the business can show us.

Since virtually every company faces some risks, it's worth knowing what they are, and we've spotted 3 warning signs for Camlin Fine Sciences (of which 2 are concerning!) that you should know about.

For those who like to invest in solid companies, check out this free list of companies with solid balance sheets and high returns on equity.

When trading Camlin Fine Sciences or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:CAMLINFINE

Camlin Fine Sciences

Engages in the research, development, manufacture, and marketing of specialty chemicals, ingredients, and additive blend products in India and internationally.

Good value with mediocre balance sheet.