- India

- /

- Metals and Mining

- /

- NSEI:ASHAPURMIN

Further Upside For Ashapura Minechem Limited (NSE:ASHAPURMIN) Shares Could Introduce Price Risks After 41% Bounce

The Ashapura Minechem Limited (NSE:ASHAPURMIN) share price has done very well over the last month, posting an excellent gain of 41%. This latest share price bounce rounds out a remarkable 420% gain over the last twelve months.

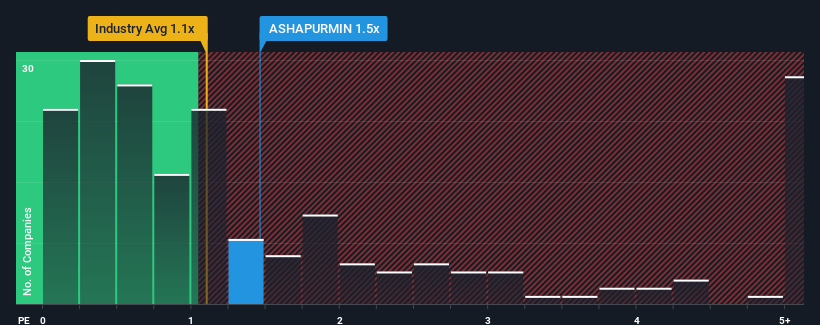

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Ashapura Minechem's P/S ratio of 1.5x, since the median price-to-sales (or "P/S") ratio for the Metals and Mining industry in India is also close to 1.1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

See our latest analysis for Ashapura Minechem

What Does Ashapura Minechem's P/S Mean For Shareholders?

Ashapura Minechem certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to taper off, which has kept the P/S from rising. Those who are bullish on Ashapura Minechem will be hoping that this isn't the case, so that they can pick up the stock at a lower valuation.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Ashapura Minechem's earnings, revenue and cash flow.Do Revenue Forecasts Match The P/S Ratio?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Ashapura Minechem's to be considered reasonable.

Retrospectively, the last year delivered an exceptional 143% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

This is in contrast to the rest of the industry, which is expected to grow by 6.2% over the next year, materially lower than the company's recent medium-term annualised growth rates.

In light of this, it's curious that Ashapura Minechem's P/S sits in line with the majority of other companies. It may be that most investors are not convinced the company can maintain its recent growth rates.

The Final Word

Ashapura Minechem appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

We've established that Ashapura Minechem currently trades on a lower than expected P/S since its recent three-year growth is higher than the wider industry forecast. There could be some unobserved threats to revenue preventing the P/S ratio from matching this positive performance. While recent revenue trends over the past medium-term suggest that the risk of a price decline is low, investors appear to see the likelihood of revenue fluctuations in the future.

It is also worth noting that we have found 2 warning signs for Ashapura Minechem that you need to take into consideration.

If these risks are making you reconsider your opinion on Ashapura Minechem, explore our interactive list of high quality stocks to get an idea of what else is out there.

If you're looking to trade Ashapura Minechem, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:ASHAPURMIN

Ashapura Minechem

Ashapura Minechem Limited is involved in the mining, manufacturing, and trading of various minerals and its derivative products in India and internationally.

Adequate balance sheet low.

Similar Companies

Market Insights

Community Narratives