Advertisement

- India

- /

- Basic Materials

- /

- NSEI:AMBUJACEM

We Think That There Are Issues Underlying Ambuja Cements' (NSE:AMBUJACEM) Earnings

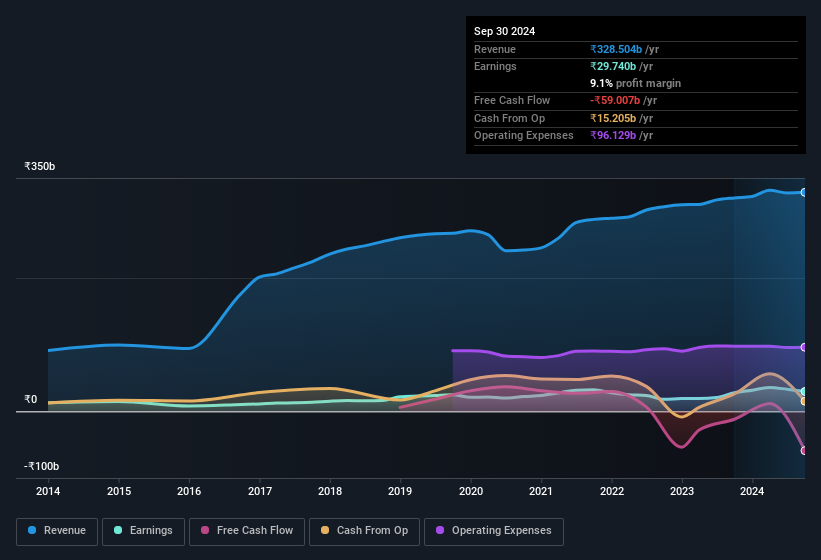

Ambuja Cements Limited's (NSE:AMBUJACEM) stock was strong after they recently reported robust earnings. However, our analysis suggests that shareholders may be missing some factors that indicate the earnings result was not as good as it looked.

Check out our latest analysis for Ambuja Cements

Examining Cashflow Against Ambuja Cements' Earnings

As finance nerds would already know, the accrual ratio from cashflow is a key measure for assessing how well a company's free cash flow (FCF) matches its profit. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. This ratio tells us how much of a company's profit is not backed by free cashflow.

Therefore, it's actually considered a good thing when a company has a negative accrual ratio, but a bad thing if its accrual ratio is positive. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to September 2024, Ambuja Cements recorded an accrual ratio of 0.23. Unfortunately, that means its free cash flow fell significantly short of its reported profits. Even though it reported a profit of ₹29.7b, a look at free cash flow indicates it actually burnt through ₹59b in the last year. We also note that Ambuja Cements' free cash flow was actually negative last year as well, so we could understand if shareholders were bothered by its outflow of ₹59b. Unfortunately for shareholders, the company has also been issuing new shares, diluting their share of future earnings.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. Ambuja Cements expanded the number of shares on issue by 24% over the last year. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. Check out Ambuja Cements' historical EPS growth by clicking on this link.

How Is Dilution Impacting Ambuja Cements' Earnings Per Share (EPS)?

Ambuja Cements' net profit dropped by 7.7% per year over the last three years. On the bright side, in the last twelve months it grew profit by 7.1%. But earnings per share are actually down 3.8%, over that same period. This is a great example of why it's rather imprudent to rely only on net income as a growth measure. Therefore, one can observe that the dilution is having a fairly profound effect on shareholder returns.

If Ambuja Cements' EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

Our Take On Ambuja Cements' Profit Performance

As it turns out, Ambuja Cements couldn't match its profit with cashflow and its dilution means that shareholders own less of the company than the did before (unless they bought more shares). Considering all this we'd argue Ambuja Cements' profits probably give an overly generous impression of its sustainable level of profitability. If you'd like to know more about Ambuja Cements as a business, it's important to be aware of any risks it's facing. To help with this, we've discovered 3 warning signs (1 can't be ignored!) that you ought to be aware of before buying any shares in Ambuja Cements.

Our examination of Ambuja Cements has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks with significant insider holdings to be useful.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:AMBUJACEM

Ambuja Cements

Manufactures, markets, and sells cement and related products to individual homebuilders, developers, infrastructure projects, masons and contractors, professionals, and architects and engineers in India.

Solid track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets