- India

- /

- Healthcare Services

- /

- NSEI:SHALBY

Shalby (NSE:SHALBY) Will Be Hoping To Turn Its Returns On Capital Around

If we want to find a potential multi-bagger, often there are underlying trends that can provide clues. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. However, after briefly looking over the numbers, we don't think Shalby (NSE:SHALBY) has the makings of a multi-bagger going forward, but let's have a look at why that may be.

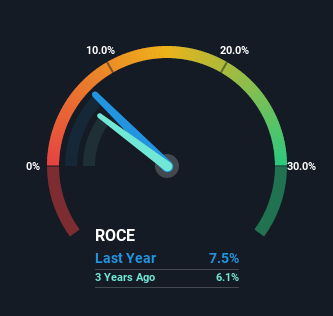

Understanding Return On Capital Employed (ROCE)

Just to clarify if you're unsure, ROCE is a metric for evaluating how much pre-tax income (in percentage terms) a company earns on the capital invested in its business. The formula for this calculation on Shalby is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.075 = ₹762m ÷ (₹12b - ₹1.7b) (Based on the trailing twelve months to June 2022).

Therefore, Shalby has an ROCE of 7.5%. Ultimately, that's a low return and it under-performs the Healthcare industry average of 15%.

View our latest analysis for Shalby

In the above chart we have measured Shalby's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for Shalby.

So How Is Shalby's ROCE Trending?

On the surface, the trend of ROCE at Shalby doesn't inspire confidence. To be more specific, ROCE has fallen from 10% over the last five years. However, given capital employed and revenue have both increased it appears that the business is currently pursuing growth, at the consequence of short term returns. And if the increased capital generates additional returns, the business, and thus shareholders, will benefit in the long run.

What We Can Learn From Shalby's ROCE

In summary, despite lower returns in the short term, we're encouraged to see that Shalby is reinvesting for growth and has higher sales as a result. And the stock has followed suit returning a meaningful 69% to shareholders over the last three years. So should these growth trends continue, we'd be optimistic on the stock going forward.

If you want to continue researching Shalby, you might be interested to know about the 2 warning signs that our analysis has discovered.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you're looking to trade Shalby, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:SHALBY

Shalby

Engages in the operation of multi-specialty hospitals primarily in India, the United States, Japan, Indonesia, Oman, the United Arab Emirates, Bangladesh, Nepal, and internationally.

Reasonable growth potential with adequate balance sheet.

Market Insights

Community Narratives