In the wake of a historic U.S. election, global markets have shown robust performance, with major indices like the S&P 500 and Nasdaq Composite reaching record highs amid expectations of favorable economic policies. This optimistic climate highlights the potential for growth stocks, particularly those with high insider ownership, as they often reflect strong confidence in a company's future prospects from those who know it best.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Medley (TSE:4480) | 34% | 30.4% |

| Pharma Mar (BME:PHM) | 11.8% | 56.4% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| Adveritas (ASX:AV1) | 21.2% | 144.2% |

| Plenti Group (ASX:PLT) | 12.8% | 107.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Brightstar Resources (ASX:BTR) | 14.8% | 84.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Let's explore several standout options from the results in the screener.

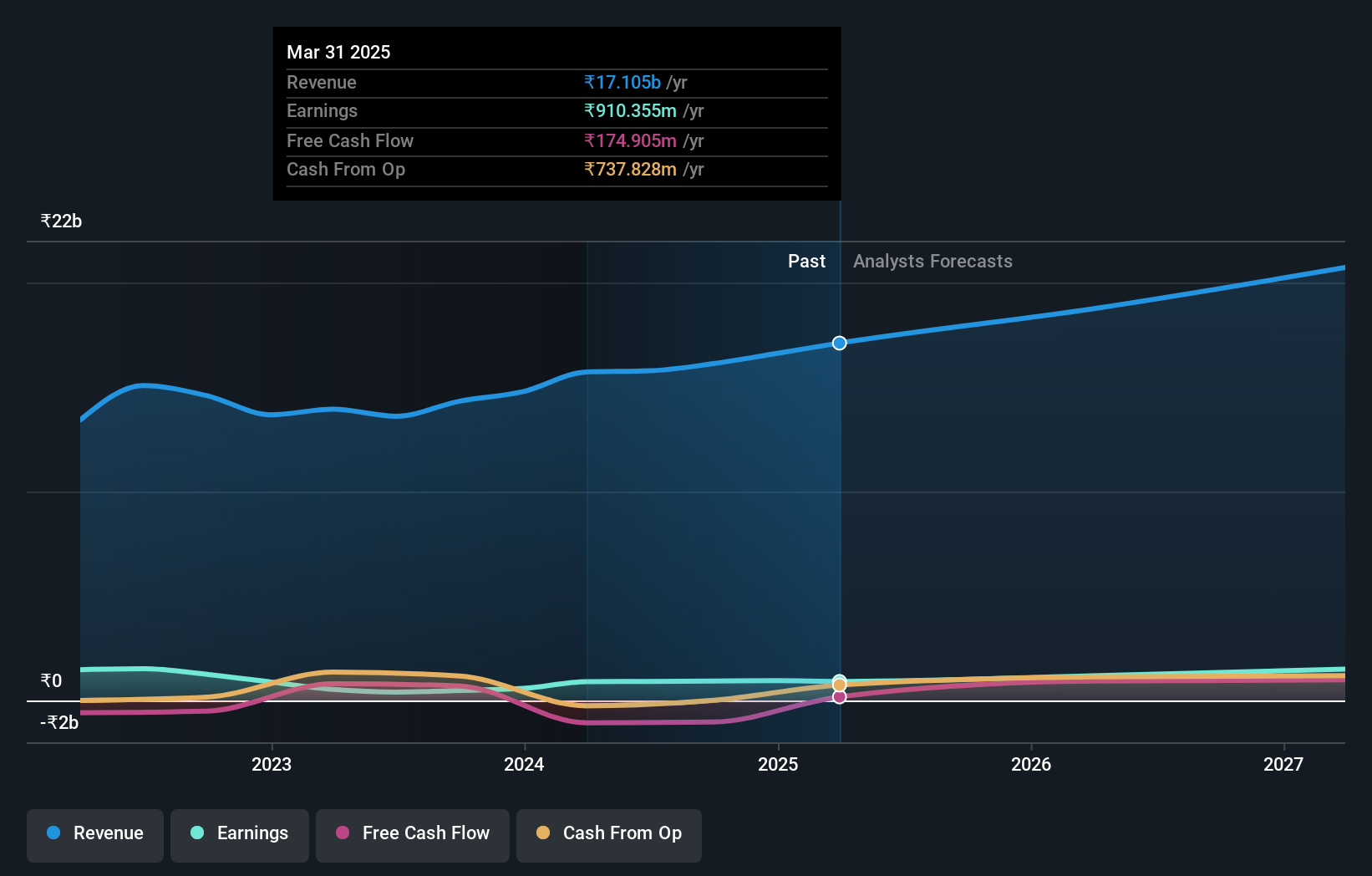

Dollar Industries (NSEI:DOLLAR)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dollar Industries Limited manufactures and sells hosiery products, including knitted innerwear, casual wear, and thermal wear in India and internationally, with a market cap of ₹31 billion.

Operations: The company's revenue primarily comes from garments, hosiery goods, rainwear products, and related services, totaling ₹15.78 billion.

Insider Ownership: 14.2%

Revenue Growth Forecast: 12.5% p.a.

Dollar Industries demonstrates promising growth potential with forecasted earnings growth of 30.6% annually, outpacing the Indian market's 18%. The company's revenue is expected to grow at 12.5% per year, faster than the market average but below significant thresholds. Recent earnings showed improvement with net income rising to INR 153.03 million from INR 145.26 million a year ago. However, its dividend yield of 0.56% is not well covered by free cash flows, and debt coverage by operating cash flow remains inadequate.

- Dive into the specifics of Dollar Industries here with our thorough growth forecast report.

- Our valuation report here indicates Dollar Industries may be overvalued.

Entero Healthcare Solutions (NSEI:ENTERO)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Entero Healthcare Solutions Limited is involved in the trading of pharmaceutical and surgical products to various healthcare providers in India, with a market cap of ₹65.40 billion.

Operations: The company's revenue is primarily derived from trading pharmaceutical and surgical products, amounting to ₹41.32 billion.

Insider Ownership: 15.8%

Revenue Growth Forecast: 30.9% p.a.

Entero Healthcare Solutions exhibits strong growth potential, with earnings forecasted to grow 53.25% annually, significantly outpacing the Indian market's average of 18%. Recent financial results show a substantial increase in net income to INR 200.8 million from INR 62.4 million year-over-year. Revenue is projected to grow at an impressive rate of 30.9% per year, surpassing market expectations. Although insider buying has been modest recently, the company's growth trajectory remains robust despite low return on equity forecasts at 12.4%.

- Get an in-depth perspective on Entero Healthcare Solutions' performance by reading our analyst estimates report here.

- According our valuation report, there's an indication that Entero Healthcare Solutions' share price might be on the expensive side.

Amata Corporation (SET:AMATA)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Amata Corporation Public Company Limited, with a market cap of THB34.50 billion, develops industrial estates in Thailand and internationally through its subsidiaries.

Operations: The company's revenue segments include Rental at THB949 million, Utility Services at THB5.14 billion, and Industrial Estate Development at THB5.42 billion.

Insider Ownership: 28.0%

Revenue Growth Forecast: 12.8% p.a.

Amata Corporation's revenue is expected to grow at 12.8% annually, outpacing the Thai market average of 6.4%, with earnings projected to rise significantly by 21.1% per year over the next three years. Despite a reduction in profit margins from last year's figures, recent earnings reports show increased sales and revenue compared to the previous year. The company has not seen substantial insider trading activity recently but maintains a high level of debt while negotiating significant loan agreements totaling THB 560 million.

- Unlock comprehensive insights into our analysis of Amata Corporation stock in this growth report.

- The valuation report we've compiled suggests that Amata Corporation's current price could be inflated.

Seize The Opportunity

- Embark on your investment journey to our 1529 Fast Growing Companies With High Insider Ownership selection here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Simply Wall St is your key to unlocking global market trends, a free user-friendly app for forward-thinking investors.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

If you're looking to trade Dollar Industries, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NSEI:DOLLAR

Dollar Industries

Manufactures and sells hosiery products in knitted inner wears, casual wears, and thermal wears in India and internationally.

Solid track record with reasonable growth potential.

Similar Companies

Market Insights

Community Narratives