Shareholders May Not Be So Generous With Uttam Sugar Mills Limited's (NSE:UTTAMSUGAR) CEO Compensation And Here's Why

Performance at Uttam Sugar Mills Limited (NSE:UTTAMSUGAR) has been reasonably good and CEO Raj Adlakha has done a decent job of steering the company in the right direction. This is something shareholders will keep in mind as they cast their votes on company resolutions such as executive remuneration in the upcoming AGM on 17 September 2021. However, some shareholders may still be hesitant of being overly generous with CEO compensation.

See our latest analysis for Uttam Sugar Mills

Comparing Uttam Sugar Mills Limited's CEO Compensation With the industry

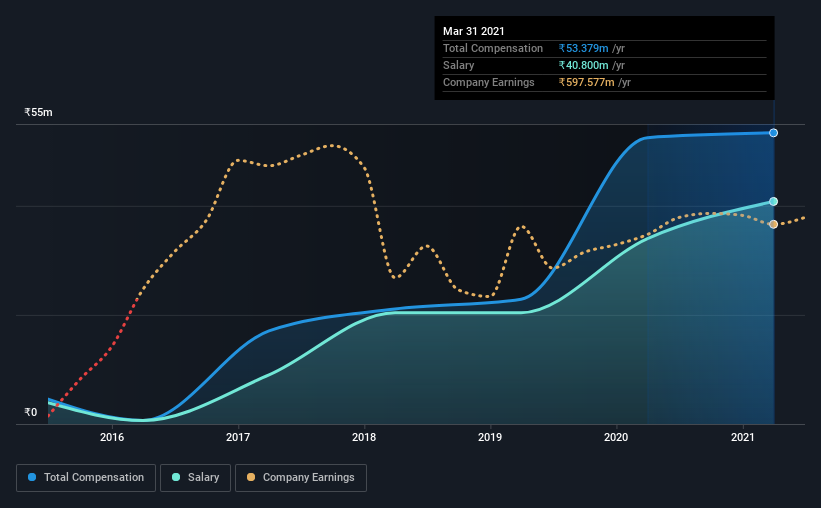

Our data indicates that Uttam Sugar Mills Limited has a market capitalization of ₹7.2b, and total annual CEO compensation was reported as ₹53m for the year to March 2021. That's mostly flat as compared to the prior year's compensation. In particular, the salary of ₹40.8m, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the industry with market capitalizations below ₹15b, reported a median total CEO compensation of ₹3.0m. Hence, we can conclude that Raj Adlakha is remunerated higher than the industry median. What's more, Raj Adlakha holds ₹306m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2021 | 2020 | Proportion (2021) |

| Salary | ₹41m | ₹34m | 76% |

| Other | ₹13m | ₹19m | 24% |

| Total Compensation | ₹53m | ₹53m | 100% |

Speaking on an industry level, all of total compensation represents salary, while non-salary remuneration is completely ignored. In Uttam Sugar Mills' case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

A Look at Uttam Sugar Mills Limited's Growth Numbers

Uttam Sugar Mills Limited has seen its earnings per share (EPS) increase by 15% a year over the past three years. In the last year, its revenue is up 9.8%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. It's nice to see revenue heading northwards, as this is consistent with healthy business conditions. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Uttam Sugar Mills Limited Been A Good Investment?

Boasting a total shareholder return of 70% over three years, Uttam Sugar Mills Limited has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

To Conclude...

Given that the company's overall performance has been reasonable, the CEO remuneration policy might not be shareholders' central point of focus in the upcoming AGM. Still, not all shareholders might be in favor of a pay raise to the CEO, seeing that they are already being paid higher than the industry.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. We identified 4 warning signs for Uttam Sugar Mills (2 are concerning!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading Uttam Sugar Mills or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NSEI:UTTAMSUGAR

Uttam Sugar Mills

Manufactures and sells sugar products under the Uttam brand in India and internationally.

Good value with adequate balance sheet.

Market Insights

Community Narratives