Here's Why I Think Uttam Sugar Mills (NSE:UTTAMSUGAR) Is An Interesting Stock

Like a puppy chasing its tail, some new investors often chase 'the next big thing', even if that means buying 'story stocks' without revenue, let alone profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.'

If, on the other hand, you like companies that have revenue, and even earn profits, then you may well be interested in Uttam Sugar Mills (NSE:UTTAMSUGAR). Even if the shares are fully valued today, most capitalists would recognize its profits as the demonstration of steady value generation. In comparison, loss making companies act like a sponge for capital - but unlike such a sponge they do not always produce something when squeezed.

See our latest analysis for Uttam Sugar Mills

How Fast Is Uttam Sugar Mills Growing Its Earnings Per Share?

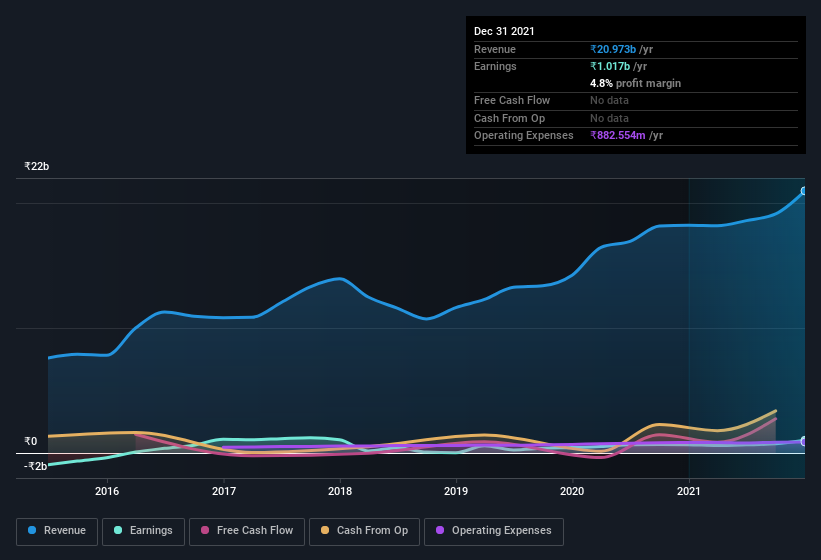

In the last three years Uttam Sugar Mills's earnings per share took off like a rocket; fast, and from a low base. So the actual rate of growth doesn't tell us much. Thus, it makes sense to focus on more recent growth rates, instead. Like a falcon taking flight, Uttam Sugar Mills's EPS soared from ₹17.52 to ₹26.66, over the last year. That's a commendable gain of 52%.

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. Uttam Sugar Mills maintained stable EBIT margins over the last year, all while growing revenue 15% to ₹21b. That's progress.

In the chart below, you can see how the company has grown earnings, and revenue, over time. Click on the chart to see the exact numbers.

Since Uttam Sugar Mills is no giant, with a market capitalization of ₹10b, so you should definitely check its cash and debt before getting too excited about its prospects.

Are Uttam Sugar Mills Insiders Aligned With All Shareholders?

I like company leaders to have some skin in the game, so to speak, because it increases alignment of incentives between the people running the business, and its true owners. So it is good to see that Uttam Sugar Mills insiders have a significant amount of capital invested in the stock. Indeed, they hold ₹2.3b worth of its stock. That shows significant buy-in, and may indicate conviction in the business strategy. Those holdings account for over 22% of the company; visible skin in the game.

Is Uttam Sugar Mills Worth Keeping An Eye On?

You can't deny that Uttam Sugar Mills has grown its earnings per share at a very impressive rate. That's attractive. I think that EPS growth is something to boast of, and it doesn't surprise me that insiders are holding on to a considerable chunk of shares. So this is very likely the kind of business that I like to spend time researching, with a view to discerning its true value. We don't want to rain on the parade too much, but we did also find 4 warning signs for Uttam Sugar Mills (1 makes us a bit uncomfortable!) that you need to be mindful of.

Although Uttam Sugar Mills certainly looks good to me, I would like it more if insiders were buying up shares. If you like to see insider buying, too, then this free list of growing companies that insiders are buying, could be exactly what you're looking for.

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

If you're looking to trade Uttam Sugar Mills, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:UTTAMSUGAR

Uttam Sugar Mills

Manufactures and sells sugar products under the Uttam brand in India and internationally.

Adequate balance sheet and fair value.

Market Insights

Community Narratives