Radico Khaitan Limited's (NSE:RADICO) CEO Compensation Is Looking A Bit Stretched At The Moment

Performance at Radico Khaitan Limited (NSE:RADICO) has been reasonably good and CEO Lalit Khaitan has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 29 September 2022. However, some shareholders may still want to keep CEO compensation within reason.

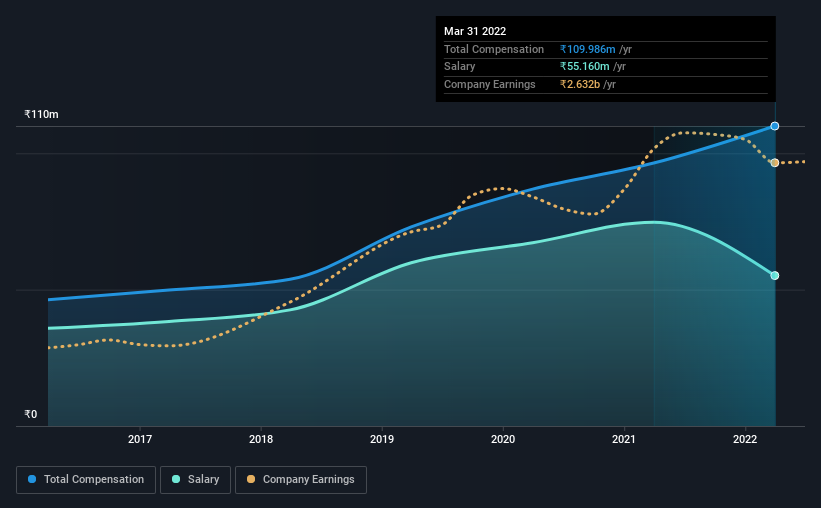

View our latest analysis for Radico Khaitan

How Does Total Compensation For Lalit Khaitan Compare With Other Companies In The Industry?

Our data indicates that Radico Khaitan Limited has a market capitalization of ₹147b, and total annual CEO compensation was reported as ₹110m for the year to March 2022. We note that's an increase of 14% above last year. Notably, the salary which is ₹55.2m, represents a considerable chunk of the total compensation being paid.

In comparison with other companies in the industry with market capitalizations ranging from ₹80b to ₹256b, the reported median CEO total compensation was ₹16m. This suggests that Lalit Khaitan is paid more than the median for the industry. Moreover, Lalit Khaitan also holds ₹303m worth of Radico Khaitan stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

| Component | 2022 | 2021 | Proportion (2022) |

| Salary | ₹55m | ₹75m | 50% |

| Other | ₹55m | ₹22m | 50% |

| Total Compensation | ₹110m | ₹96m | 100% |

Talking in terms of the industry, salary represented approximately 97% of total compensation out of all the companies we analyzed, while other remuneration made up 3% of the pie. It's interesting to note that Radico Khaitan allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

A Look at Radico Khaitan Limited's Growth Numbers

Radico Khaitan Limited's earnings per share (EPS) grew 9.5% per year over the last three years. It achieved revenue growth of 16% over the last year.

This revenue growth could really point to a brighter future. And, while modest, the EPS growth is noticeable. So while performance isn't amazing, we think it really does seem quite respectable. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Radico Khaitan Limited Been A Good Investment?

Most shareholders would probably be pleased with Radico Khaitan Limited for providing a total return of 245% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Seeing that the company has put up a decent performance, only a few shareholders, if any at all, might have questions about the CEO pay in the upcoming AGM. However, any decision to raise CEO pay might be met with some objections from the shareholders given that the CEO is already paid higher than the industry average.

CEO compensation is one thing, but it is also interesting to check if the CEO is buying or selling Radico Khaitan (free visualization of insider trades).

Important note: Radico Khaitan is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RADICO

Radico Khaitan

Engages in the manufacture and trading of Indian made foreign liquor (IMFL) and country liquor in India and internationally.

Excellent balance sheet with reasonable growth potential and pays a dividend.

Similar Companies

Market Insights

Community Narratives