Advertisement

Nakoda Group of Industries (NSE:NGILPP1) Is Making Moderate Use Of Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. Importantly, Nakoda Group of Industries Limited (NSE:NGILPP1) does carry debt. But the real question is whether this debt is making the company risky.

What Risk Does Debt Bring?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Nakoda Group of Industries

What Is Nakoda Group of Industries's Debt?

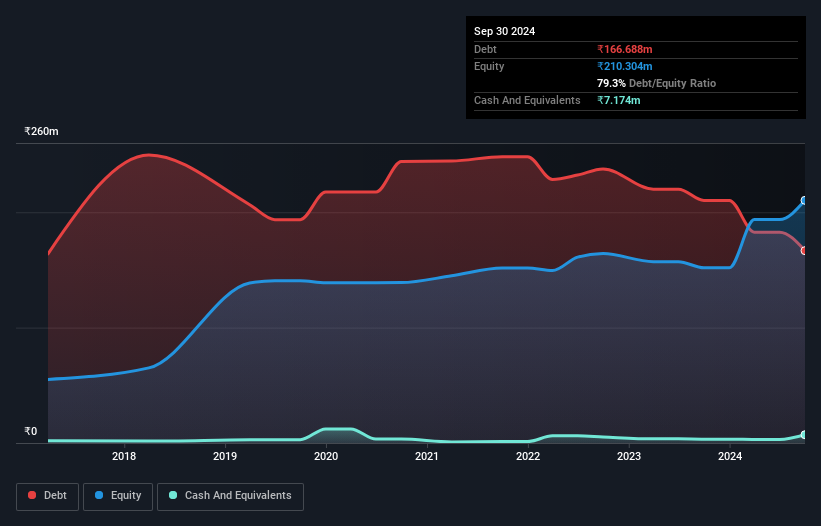

You can click the graphic below for the historical numbers, but it shows that Nakoda Group of Industries had ₹166.7m of debt in September 2024, down from ₹210.2m, one year before. However, it does have ₹7.17m in cash offsetting this, leading to net debt of about ₹159.5m.

How Healthy Is Nakoda Group of Industries' Balance Sheet?

We can see from the most recent balance sheet that Nakoda Group of Industries had liabilities of ₹148.7m falling due within a year, and liabilities of ₹40.8m due beyond that. Offsetting this, it had ₹7.17m in cash and ₹49.3m in receivables that were due within 12 months. So its liabilities total ₹133.1m more than the combination of its cash and short-term receivables.

Since publicly traded Nakoda Group of Industries shares are worth a total of ₹788.1m, it seems unlikely that this level of liabilities would be a major threat. Having said that, it's clear that we should continue to monitor its balance sheet, lest it change for the worse. There's no doubt that we learn most about debt from the balance sheet. But it is Nakoda Group of Industries's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

In the last year Nakoda Group of Industries had a loss before interest and tax, and actually shrunk its revenue by 17%, to ₹432m. That's not what we would hope to see.

Caveat Emptor

While Nakoda Group of Industries's falling revenue is about as heartwarming as a wet blanket, arguably its earnings before interest and tax (EBIT) loss is even less appealing. To be specific the EBIT loss came in at ₹22m. Considering that alongside the liabilities mentioned above does not give us much confidence that company should be using so much debt. So we think its balance sheet is a little strained, though not beyond repair. However, it doesn't help that it burned through ₹45m of cash over the last year. So suffice it to say we consider the stock very risky. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. To that end, you should be aware of the 5 warning signs we've spotted with Nakoda Group of Industries .

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

Valuation is complex, but we're here to simplify it.

Discover if Nakoda Group of Industries might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:NGILPP1

Nakoda Group of Industries

Engages in the manufacture and trading of tutty fruity and other agriculture commodities in India.

Slight with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|3.1% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|11.6% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|39.4% undervalued

TR

Community Contributor