- India

- /

- Oil and Gas

- /

- NSEI:OIL

There's No Escaping Oil India Limited's (NSE:OIL) Muted Earnings Despite A 25% Share Price Rise

Oil India Limited (NSE:OIL) shares have continued their recent momentum with a 25% gain in the last month alone. Looking back a bit further, it's encouraging to see the stock is up 95% in the last year.

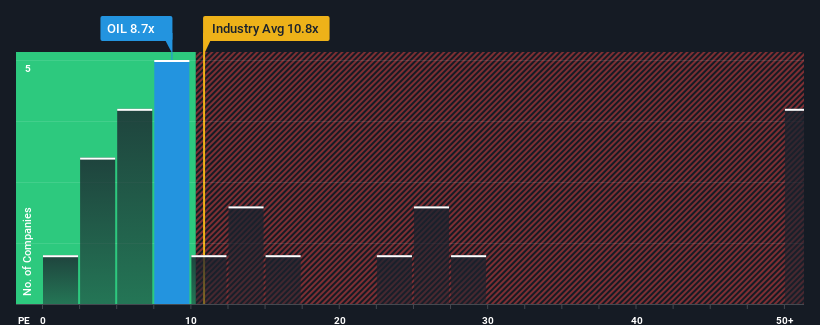

Although its price has surged higher, Oil India's price-to-earnings (or "P/E") ratio of 8.7x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 33x and even P/E's above 60x are quite common. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's so limited.

Oil India hasn't been tracking well recently as its declining earnings compare poorly to other companies, which have seen some growth on average. It seems that many are expecting the dour earnings performance to persist, which has repressed the P/E. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

View our latest analysis for Oil India

Does Growth Match The Low P/E?

Oil India's P/E ratio would be typical for a company that's expected to deliver very poor growth or even falling earnings, and importantly, perform much worse than the market.

Retrospectively, the last year delivered a frustrating 28% decrease to the company's bottom line. However, a few very strong years before that means that it was still able to grow EPS by an impressive 116% in total over the last three years. So we can start by confirming that the company has generally done a very good job of growing earnings over that time, even though it had some hiccups along the way.

Looking ahead now, EPS is anticipated to climb by 2.4% each year during the coming three years according to the nine analysts following the company. With the market predicted to deliver 20% growth each year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that Oil India's P/E sits below the majority of other companies. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Oil India's P/E?

Oil India's recent share price jump still sees its P/E sitting firmly flat on the ground. Typically, we'd caution against reading too much into price-to-earnings ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

We've established that Oil India maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Plus, you should also learn about these 2 warning signs we've spotted with Oil India.

If P/E ratios interest you, you may wish to see this free collection of other companies with strong earnings growth and low P/E ratios.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:OIL

Oil India

Engages in the exploration, development, and production of crude oil and natural gas in India.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Community Narratives