Advertisement

- India

- /

- Diversified Financial

- /

- NSEI:RECLTD

Improved Earnings Required Before REC Limited (NSE:RECLTD) Stock's 26% Jump Looks Justified

REC Limited (NSE:RECLTD) shares have had a really impressive month, gaining 26% after a shaky period beforehand. The last 30 days were the cherry on top of the stock's 315% gain in the last year, which is nothing short of spectacular.

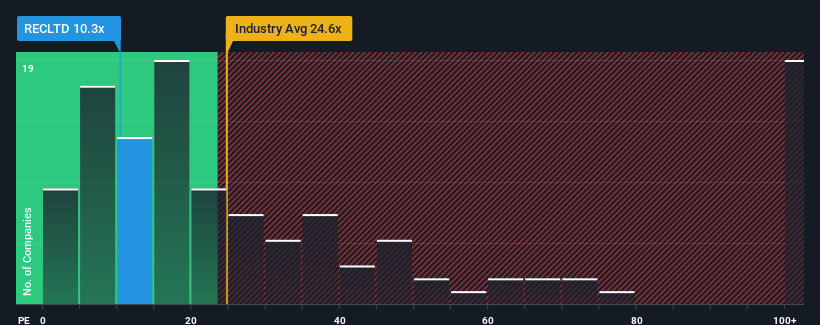

Although its price has surged higher, REC's price-to-earnings (or "P/E") ratio of 10.3x might still make it look like a strong buy right now compared to the market in India, where around half of the companies have P/E ratios above 32x and even P/E's above 61x are quite common. However, the P/E might be quite low for a reason and it requires further investigation to determine if it's justified.

With earnings growth that's superior to most other companies of late, REC has been doing relatively well. It might be that many expect the strong earnings performance to degrade substantially, which has repressed the P/E. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

Check out our latest analysis for REC

What Are Growth Metrics Telling Us About The Low P/E?

In order to justify its P/E ratio, REC would need to produce anemic growth that's substantially trailing the market.

Retrospectively, the last year delivered an exceptional 27% gain to the company's bottom line. Pleasingly, EPS has also lifted 68% in aggregate from three years ago, thanks to the last 12 months of growth. So we can start by confirming that the company has done a great job of growing earnings over that time.

Looking ahead now, EPS is anticipated to climb by 11% per year during the coming three years according to the five analysts following the company. With the market predicted to deliver 21% growth per year, the company is positioned for a weaker earnings result.

In light of this, it's understandable that REC's P/E sits below the majority of other companies. It seems most investors are expecting to see limited future growth and are only willing to pay a reduced amount for the stock.

What We Can Learn From REC's P/E?

Shares in REC are going to need a lot more upward momentum to get the company's P/E out of its slump. Generally, our preference is to limit the use of the price-to-earnings ratio to establishing what the market thinks about the overall health of a company.

We've established that REC maintains its low P/E on the weakness of its forecast growth being lower than the wider market, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Having said that, be aware REC is showing 2 warning signs in our investment analysis, and 1 of those is a bit concerning.

Of course, you might also be able to find a better stock than REC. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RECLTD

REC

Engages in the provision of financing services for power generation, transmission, and distribution projects in India.

Very undervalued average dividend payer.

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor