Advertisement

- India

- /

- Hospitality

- /

- NSEI:RBA

Restaurant Brands Asia Limited's (NSE:RBA) Revenues Are Not Doing Enough For Some Investors

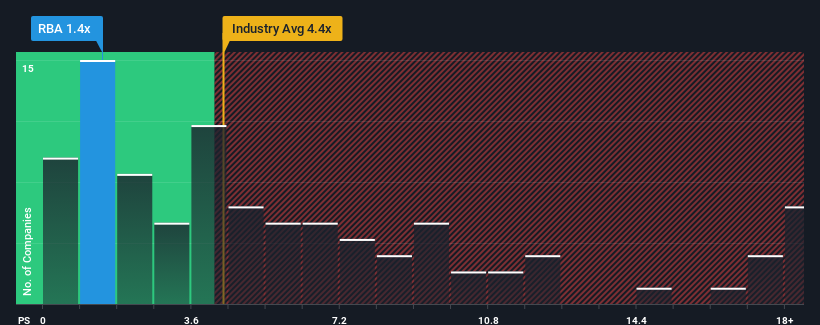

With a price-to-sales (or "P/S") ratio of 1.4x Restaurant Brands Asia Limited (NSE:RBA) may be sending very bullish signals at the moment, given that almost half of all the Hospitality companies in India have P/S ratios greater than 4.4x and even P/S higher than 9x are not unusual. Nonetheless, we'd need to dig a little deeper to determine if there is a rational basis for the highly reduced P/S.

View our latest analysis for Restaurant Brands Asia

What Does Restaurant Brands Asia's Recent Performance Look Like?

Recent times haven't been great for Restaurant Brands Asia as its revenue has been rising slower than most other companies. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If this is the case, then existing shareholders will probably struggle to get excited about the future direction of the share price.

Keen to find out how analysts think Restaurant Brands Asia's future stacks up against the industry? In that case, our free report is a great place to start .Is There Any Revenue Growth Forecasted For Restaurant Brands Asia?

There's an inherent assumption that a company should far underperform the industry for P/S ratios like Restaurant Brands Asia's to be considered reasonable.

If we review the last year of revenue growth, the company posted a worthy increase of 6.9%. The latest three year period has also seen an excellent 189% overall rise in revenue, aided somewhat by its short-term performance. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Shifting to the future, estimates from the five analysts covering the company suggest revenue should grow by 17% per annum over the next three years. Meanwhile, the rest of the industry is forecast to expand by 33% per year, which is noticeably more attractive.

With this information, we can see why Restaurant Brands Asia is trading at a P/S lower than the industry. Apparently many shareholders weren't comfortable holding on while the company is potentially eyeing a less prosperous future.

What We Can Learn From Restaurant Brands Asia's P/S?

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

As we suspected, our examination of Restaurant Brands Asia's analyst forecasts revealed that its inferior revenue outlook is contributing to its low P/S. At this stage investors feel the potential for an improvement in revenue isn't great enough to justify a higher P/S ratio. The company will need a change of fortune to justify the P/S rising higher in the future.

Before you take the next step, you should know about the 1 warning sign for Restaurant Brands Asia that we have uncovered.

If these risks are making you reconsider your opinion on Restaurant Brands Asia, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:RBA

Fair value with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.9% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.9% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|64.1% undervalued

ME

Community Contributor