- India

- /

- Hospitality

- /

- NSEI:INDHOTEL

These 4 Measures Indicate That Indian Hotels (NSE:INDHOTEL) Is Using Debt Safely

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that The Indian Hotels Company Limited (NSE:INDHOTEL) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Indian Hotels

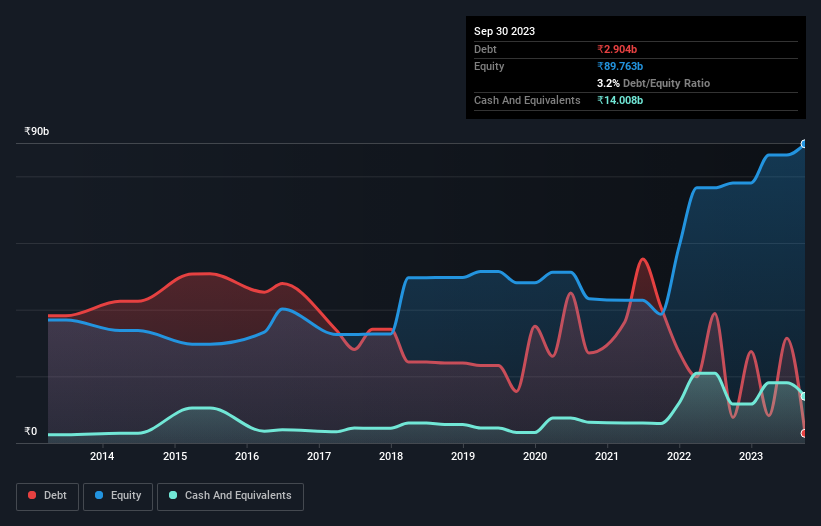

What Is Indian Hotels's Net Debt?

As you can see below, Indian Hotels had ₹2.90b of debt at September 2023, down from ₹7.69b a year prior. But it also has ₹14.0b in cash to offset that, meaning it has ₹11.1b net cash.

How Healthy Is Indian Hotels' Balance Sheet?

We can see from the most recent balance sheet that Indian Hotels had liabilities of ₹18.7b falling due within a year, and liabilities of ₹27.1b due beyond that. On the other hand, it had cash of ₹14.0b and ₹4.91b worth of receivables due within a year. So its liabilities total ₹26.9b more than the combination of its cash and short-term receivables.

Given Indian Hotels has a market capitalization of ₹597.3b, it's hard to believe these liabilities pose much threat. But there are sufficient liabilities that we would certainly recommend shareholders continue to monitor the balance sheet, going forward. Despite its noteworthy liabilities, Indian Hotels boasts net cash, so it's fair to say it does not have a heavy debt load!

Better yet, Indian Hotels grew its EBIT by 107% last year, which is an impressive improvement. If maintained that growth will make the debt even more manageable in the years ahead. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Indian Hotels can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. While Indian Hotels has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, Indian Hotels recorded free cash flow worth a fulsome 82% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Summing Up

We could understand if investors are concerned about Indian Hotels's liabilities, but we can be reassured by the fact it has has net cash of ₹11.1b. The cherry on top was that in converted 82% of that EBIT to free cash flow, bringing in ₹10b. So is Indian Hotels's debt a risk? It doesn't seem so to us. Over time, share prices tend to follow earnings per share, so if you're interested in Indian Hotels, you may well want to click here to check an interactive graph of its earnings per share history.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NSEI:INDHOTEL

Indian Hotels

Owns, operates, and manages hotels, palaces, and resorts in India and internationally.

Flawless balance sheet with solid track record.