- India

- /

- Hospitality

- /

- NSEI:AHLWEST

Here's Why Asian Hotels (West) (NSE:AHLWEST) Has A Meaningful Debt Burden

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk'. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Asian Hotels (West) Limited (NSE:AHLWEST) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Asian Hotels (West)

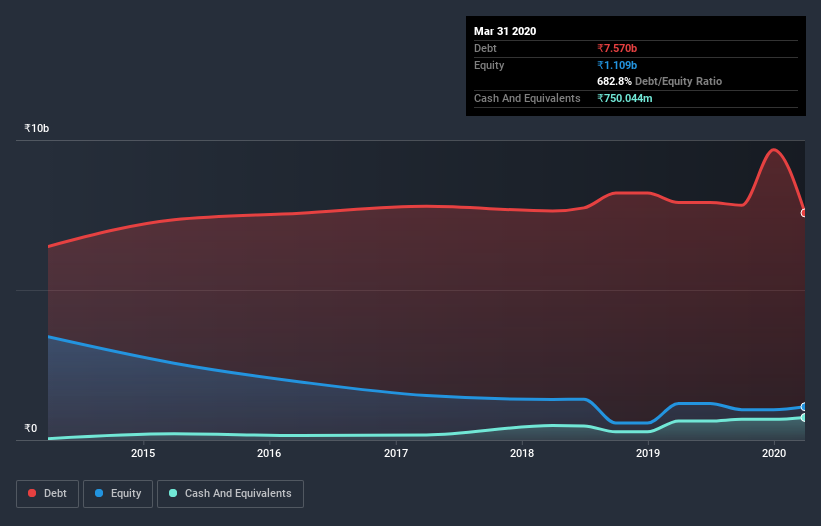

What Is Asian Hotels (West)'s Debt?

The image below, which you can click on for greater detail, shows that Asian Hotels (West) had debt of ₹7.57b at the end of March 2020, a reduction from ₹7.91b over a year. However, because it has a cash reserve of ₹750.0m, its net debt is less, at about ₹6.82b.

How Healthy Is Asian Hotels (West)'s Balance Sheet?

We can see from the most recent balance sheet that Asian Hotels (West) had liabilities of ₹1.13b falling due within a year, and liabilities of ₹9.49b due beyond that. Offsetting these obligations, it had cash of ₹750.0m as well as receivables valued at ₹142.5m due within 12 months. So its liabilities total ₹9.7b more than the combination of its cash and short-term receivables.

This deficit casts a shadow over the ₹2.92b company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. After all, Asian Hotels (West) would likely require a major re-capitalisation if it had to pay its creditors today.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

While we wouldn't worry about Asian Hotels (West)'s net debt to EBITDA ratio of 4.2, we think its super-low interest cover of 1.1 times is a sign of high leverage. So shareholders should probably be aware that interest expenses appear to have really impacted the business lately. Another concern for investors might be that Asian Hotels (West)'s EBIT fell 13% in the last year. If things keep going like that, handling the debt will about as easy as bundling an angry house cat into its travel box. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Asian Hotels (West) can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So the logical step is to look at the proportion of that EBIT that is matched by actual free cash flow. Happily for any shareholders, Asian Hotels (West) actually produced more free cash flow than EBIT over the last three years. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

On the face of it, Asian Hotels (West)'s interest cover left us tentative about the stock, and its level of total liabilities was no more enticing than the one empty restaurant on the busiest night of the year. But at least it's pretty decent at converting EBIT to free cash flow; that's encouraging. Overall, it seems to us that Asian Hotels (West)'s balance sheet is really quite a risk to the business. For this reason we're pretty cautious about the stock, and we think shareholders should keep a close eye on its liquidity. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. Be aware that Asian Hotels (West) is showing 3 warning signs in our investment analysis , and 1 of those is a bit unpleasant...

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

If you’re looking to trade Asian Hotels (West), open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NSEI:AHLWEST

Asian Hotels (West)

Asian Hotels (West) Limited, together with its subsidiaries, engages in the hotel business in India.

Weak fundamentals or lack of information.

Market Insights

Community Narratives